Should Quanta’s Record AI-Fueled Backlog and Buybacks Require Action From Quanta Services (PWR) Investors?

Quanta Services, Inc. PWR | 0.00 |

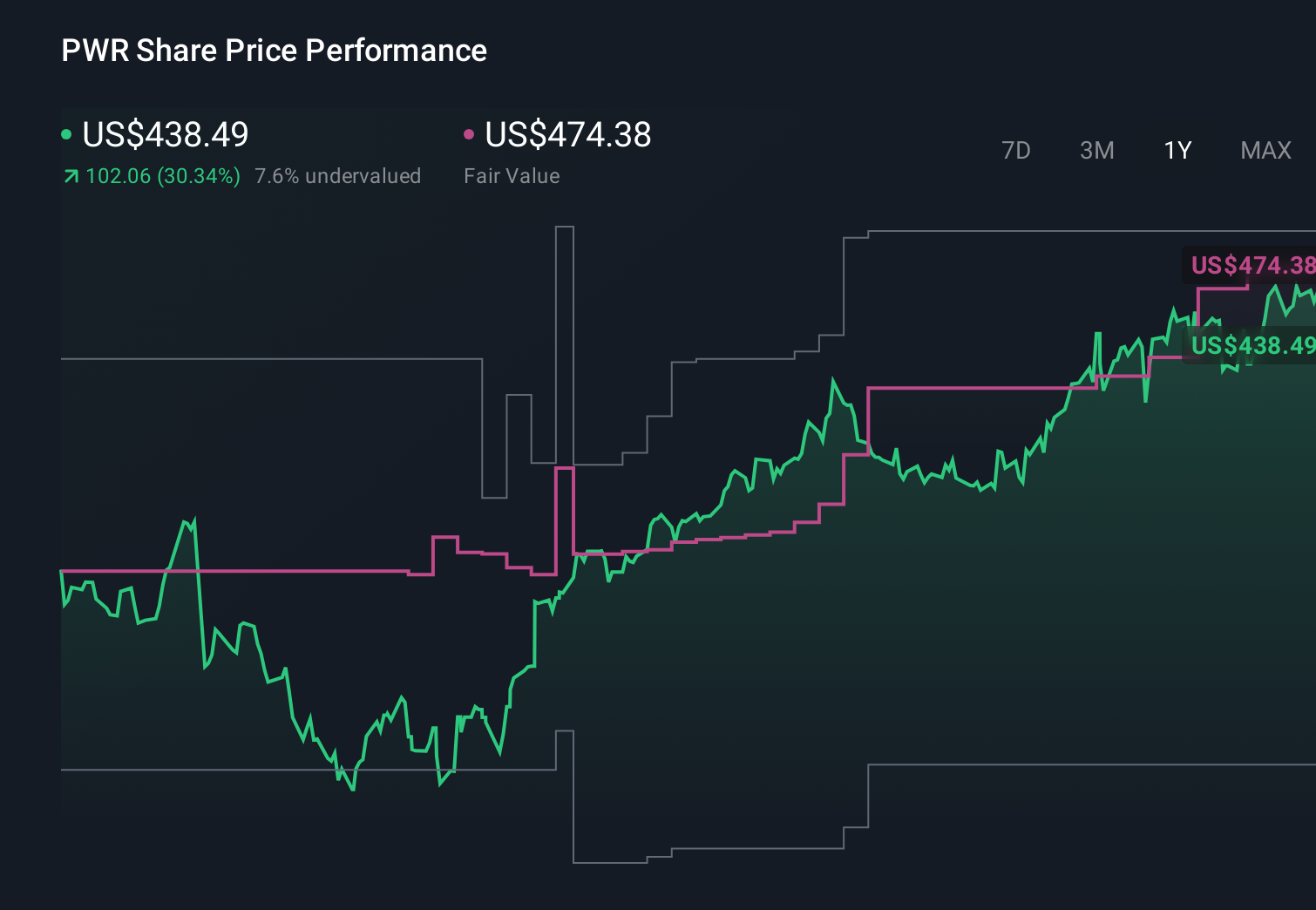

- In recent days, Quanta Services reported quarterly earnings and revenues that exceeded expectations, highlighted a record multibillion-dollar backlog across utility, renewables, and data center projects, and raised its 2026 outlook as AI and electrification-related demand intensified.

- Analysts and investors now see Quanta as increasingly central to enabling large-scale power-grid and data center build-outs, with its expanding role supported by a new US$1.00 billion share repurchase authorization and long-term market projections discussed at its 2026 Investor Day.

- With this backdrop of strong results and record backlog, we’ll examine how Quanta’s AI-driven energy infrastructure momentum influences its investment narrative.

This technology could replace computers: discover 29 stocks that are working to make quantum computing a reality.

Quanta Services Investment Narrative Recap

To own Quanta Services, you need to believe that AI, data centers, and grid modernization will keep driving multi-year infrastructure spending, and that Quanta can convert its record backlog into profitable work. The latest earnings beat and backlog strength appear to reinforce the near term catalyst around AI-driven power-grid build-outs, while the biggest risk remains potential delays or pullbacks in customer capital spending that could slow project starts and backlog conversion.

The new US$1.00 billion share repurchase authorization stands out in light of the recent share price move, because it directly connects to the same theme powering Quanta’s record backlog: confidence in ongoing AI and electrification-related workloads. For investors focused on catalysts, this buyback program adds another lever alongside raised 2026 guidance and strong free cash flow to potentially support the stock if execution on these large, complex projects stays on track.

However, against this strong AI-fueled story, investors should also be aware of risks around regulatory and permitting delays that could...

Quanta Services' narrative projects $46.6 billion revenue and $2.4 billion earnings by 2029. This requires 15.7% yearly revenue growth and about a $1.3 billion earnings increase from $1.1 billion today.

Uncover how Quanta Services' forecasts yield a $761.35 fair value, a 5% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts already expected Quanta’s earnings to climb toward about US$3.3 billion by 2029, yet they also flagged rising automation as a threat to its labor focused model; this shows how you can read the same AI and data center news and still reach very different views on how sustainable today’s growth really is.

Explore 6 other fair value estimates on Quanta Services - why the stock might be worth 42% less than the current price!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Quanta Services research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Quanta Services research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Quanta Services' overall financial health at a glance.

Looking For Alternative Opportunities?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- Find 47 companies with promising cash flow potential yet trading below their fair value.

- We've uncovered the 9 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 14 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.