Should Questions Over GDDY’s Discount Disclosures Reshape Views On Its AI And SaaS Margin Story?

GoDaddy, Inc. Class A GDDY | 0.00 |

- Kaplan Fox & Kilsheimer LLP has begun investigating GoDaddy Inc. for potential securities law violations tied to its past disclosure of fourth-quarter promotional pricing on dotcom domains and the resulting impact on reported revenue and bookings.

- This probe raises questions about how clearly GoDaddy communicated the effects of its discounting strategy, potentially adding a governance and transparency dimension to how investors assess the business.

- We’ll now examine how concerns over GoDaddy’s promotional pricing disclosures may influence its existing investment narrative built around AI, SaaS, and margin expansion.

Uncover the next big thing with 20 elite penny stocks that balance risk and reward.

GoDaddy Investment Narrative Recap

To own GoDaddy, you generally need to believe its AI, SaaS and ecosystem strategy can support durable earnings while margin expansion remains on track. The Kaplan Fox investigation around promotional pricing touches on transparency rather than core demand, so it may not alter the main near term catalyst around AI driven monetization, but it could add to the key risk that aggressive pricing and experimentation introduce more volatility into reported revenue and investor confidence.

The most relevant recent update here is GoDaddy’s ongoing share repurchase program of up to US$3,000,000,000 through 2027, alongside recent earnings that showed continued profitability. Together, they underpin a narrative focused on earnings quality and margin improvement, which now sits next to fresh questions on disclosure practices and governance. How this balance evolves could shape how investors weigh AI and SaaS execution against potential legal, compliance and reporting risks.

Yet beneath the AI story, there is a separate set of legal, pricing, and customer concentration risks investors should be aware of...

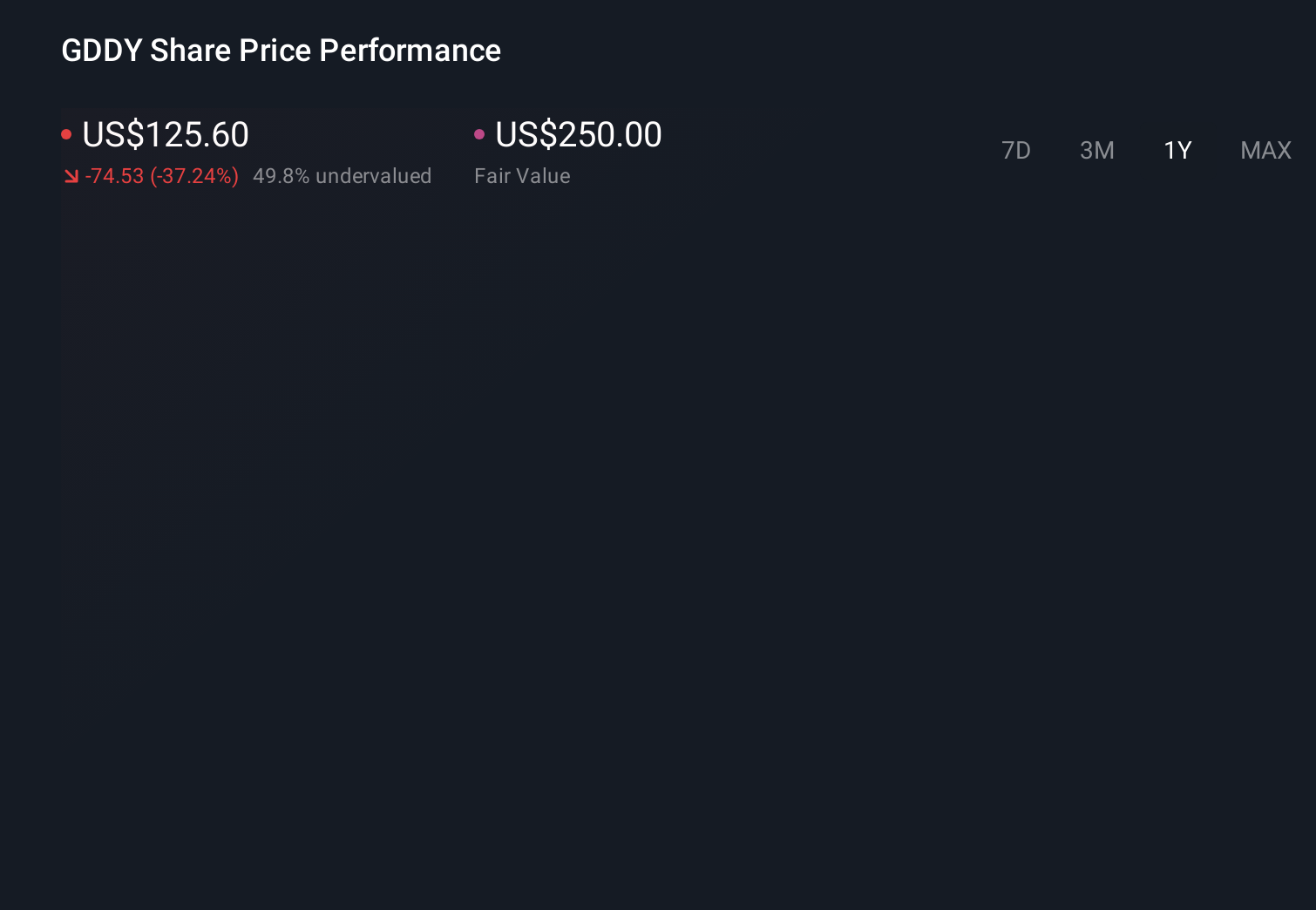

GoDaddy's narrative projects $5.9 billion revenue and $1.3 billion earnings by 2029. This requires 5.7% yearly revenue growth and a roughly $429.9 million earnings increase from $870.1 million today.

Uncover how GoDaddy's forecasts yield a $114.29 fair value, a 25% upside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts already saw more risk here, expecting only about US$5,900,000,000 in revenue and US$1,300,000,000 in earnings by 2029, and the current legal scrutiny around promotional pricing could give that more cautious view additional weight or push it even further.

Explore 6 other fair value estimates on GoDaddy - why the stock might be worth 9% less than the current price!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your GoDaddy research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

- Our free GoDaddy research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate GoDaddy's overall financial health at a glance.

Want Some Alternatives?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- Find 44 companies with promising cash flow potential yet trading below their fair value.

- The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Explore 26 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.