Should Stronger Q1 2026 Results and Portfolio Moves Require Action From International Paper (IP) Investors?

International Paper Company IP | 0.00 |

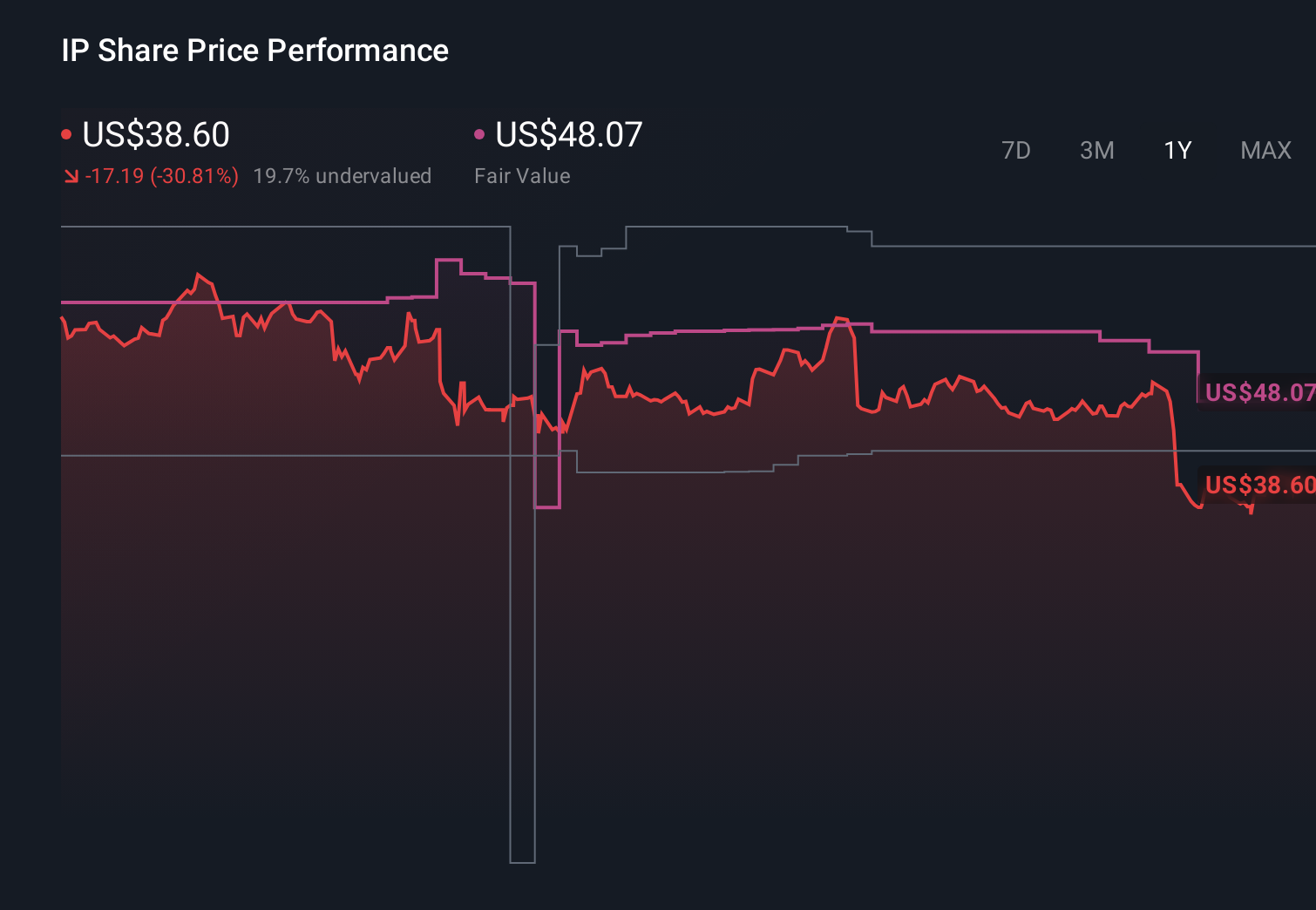

- International Paper Company has already reported first-quarter 2026 results, with sales rising to US$5,971 million from US$5,264 million and net income improving to US$60 million from a net loss of US$105 million a year earlier.

- The quarter also marked progress on its portfolio reshaping, with management highlighting transformation spending, mill reliability efforts, and acquisitions such as North Pacific Paper Company and the Norpak mill as building blocks for its longer-term plan to separate the North America and EMEA businesses.

- With Q1 2026 earnings showing higher sales and improved profitability, we’ll examine how these results influence International Paper’s investment narrative.

AI is about to change healthcare. These 33 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

International Paper Investment Narrative Recap

To own International Paper, you need to believe its multiyear turnaround in packaging can offset past losses and heavy capital needs. The most important short term catalyst remains execution on mill reliability and transformation spending, while the biggest risk is that these initiatives fail to deliver enough cost and margin improvement. Q1 2026’s higher sales and return to profitability help sentiment but do not remove the execution and reliability risks that still hang over the story.

The Q1 2026 update that reaffirmed plans to separate the North America and EMEA businesses within 12 to 15 months is especially relevant here. That split, paired with divestiture proceeds already used to reduce US$660 million of debt, sits at the heart of the current catalyst path, but also increases the complexity and execution risk around closures, cost reductions, and integration of new assets like North Pacific Paper Company.

Yet behind the improving numbers, investors should also be aware that unresolved mill reliability issues could still...

International Paper's narrative projects $26.3 billion revenue and $1.7 billion earnings by 2029.

Uncover how International Paper's forecasts yield a $46.47 fair value, a 46% upside to its current price.

Exploring Other Perspectives

Some of the most cautious analysts were assuming only about 1.7 percent annual revenue growth and roughly US$1.6 billion of earnings by 2029, so compared with the base case and the focus on mill reliability, they paint a much more pessimistic picture that Q1’s progress could still challenge or potentially soften over time.

Explore 3 other fair value estimates on International Paper - why the stock might be worth just $46.47!

Form Your Own Verdict

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your International Paper research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

- Our free International Paper research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate International Paper's overall financial health at a glance.

Curious About Other Options?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- This technology could replace computers: discover 26 stocks that are working to make quantum computing a reality.

- The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Invest in the nuclear renaissance through our list of 91 elite nuclear energy infrastructure plays powering the global AI revolution.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.