Should Stronger Same‑Unit Revenue And Reaffirmed Outlook Require Action From Pediatrix Medical Group (MD) Investors?

Pediatrix Medical Group, Inc. MD | 0.00 |

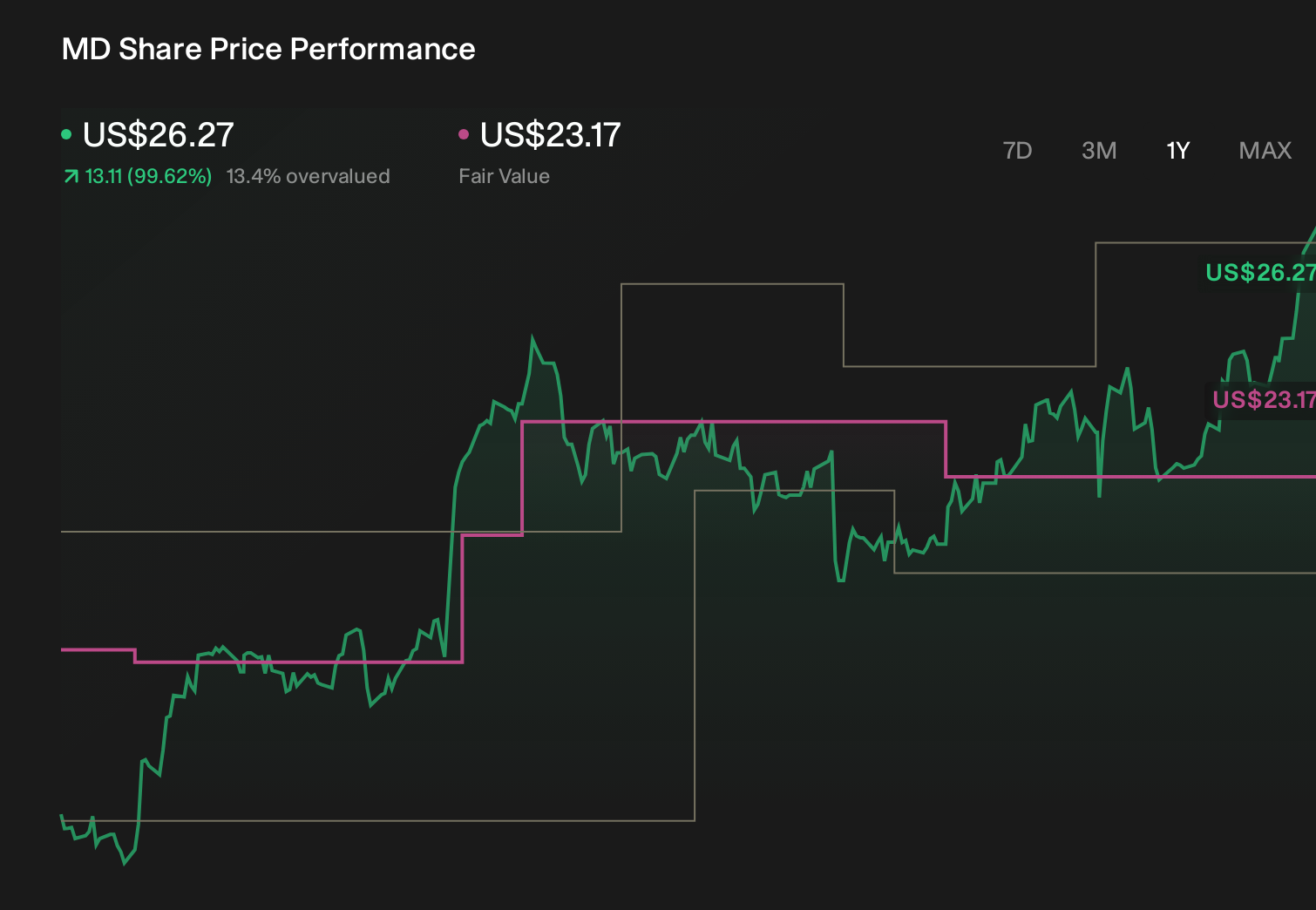

- Pediatrix Medical Group, Inc. has reported past first-quarter 2026 results showing sales of US$476.2 million and net income of US$29.57 million, with diluted earnings per share from continuing operations of US$0.36, all higher than the same period a year earlier.

- The company’s better-than-expected performance, driven by stronger same-unit revenue and improved cash collections, came alongside a reaffirmed full-year adjusted EBITDA outlook that supports management’s operational and financial confidence.

- We’ll now examine how Pediatrix’s outlook reaffirmation and stronger same-unit revenue trends might influence the company’s broader investment narrative.

The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 18 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

Pediatrix Medical Group Investment Narrative Recap

To own Pediatrix, you need to believe in steady demand for neonatal and maternal care, and in management’s ability to convert that demand into reliable cash flow despite reimbursement and labor pressures. The Q1 2026 beat, powered by stronger same unit revenue and better collections, supports the near term catalyst of margin resilience. It does not remove the biggest current risk, which is sustained pressure on hospital fees, payer terms, and reimbursement that could cap pricing power.

The recent acquisition of Tennessee Maternal-Fetal Medicine, with five Greater Nashville locations, ties directly into that same-unit revenue story. By broadening Pediatrix’s footprint in high risk pregnancy care, it increases exposure to hospital based volumes at a time when management is reaffirming its US$280 million to US$300 million adjusted EBITDA outlook. That combination of volume growth and reaffirmed guidance sits at the heart of the bullish catalyst around stable cash flows and continued buybacks.

Yet beneath the better Q1 numbers, investors should still be watching how reimbursement trends and hospital contract negotiations could suddenly shift the picture and...

Pediatrix Medical Group's narrative projects $2.1 billion revenue and $171.4 million earnings by 2029. This requires 2.6% yearly revenue growth and a $6.0 million earnings increase from $165.4 million.

Uncover how Pediatrix Medical Group's forecasts yield a $21.33 fair value, a 5% downside to its current price.

Exploring Other Perspectives

Before this beat, the most pessimistic analysts were assuming roughly flat revenue around US$2.0 billion and earnings of about US$148.9 million by 2028, so if you are relying on stable cash flows and buybacks, this Q1 surprise might eventually soften that cautious view or reinforce it depending on how you weigh reimbursement and labor cost risks.

Explore 6 other fair value estimates on Pediatrix Medical Group - why the stock might be worth less than half the current price!

Decide For Yourself

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Pediatrix Medical Group research is our analysis highlighting 3 key rewards that could impact your investment decision.

- Our free Pediatrix Medical Group research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Pediatrix Medical Group's overall financial health at a glance.

Interested In Other Possibilities?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- We've uncovered the 12 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Capitalize on the AI infrastructure supercycle with our selection of the 38 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- The future of work is here. Discover the 34 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.