Should VinFast’s Indian Showroom Surge and Delivery Jump Require Action From VinFast Auto (VFS) Investors?

VinFast Auto Ltd. VFS | 0.00 |

- VinFast Auto, through its Indian subsidiary, recently opened its 50th domestic showroom in Bengaluru via PPS Motors LLP, while also reporting a 61% quarter-on-quarter increase in global vehicle deliveries to 58,577 units and very large growth in e-scooter and e-bike shipments.

- Together, this rapid showroom rollout in India and higher global deliveries highlight how VinFast is pushing to scale both its international footprint and multi-category electric mobility offering.

- Next, we’ll examine how VinFast’s accelerating Indian showroom expansion may influence its existing investment narrative around global EV growth.

Uncover the next big thing with 23 elite penny stocks that balance risk and reward.

VinFast Auto Investment Narrative Recap

To own VinFast today, you need to believe it can turn rapid volume growth and global expansion into a sustainable, profitable EV and e-mobility platform. The jump in quarterly deliveries and the 50th Indian showroom support the short term catalyst of scaling international volumes, but they do little to reduce the immediate risks around heavy cash burn, liquidity pressure and the need for ongoing external funding, which still hang over the equity story.

Among recent developments, VinFast’s target for 2026 global EV deliveries of 300,000 units and at least 2.5 times two wheeler volumes stands out in relation to this India news. The strong Q1 growth in e scooters and e bikes, alongside a fast growing Indian showroom network, slots directly into that higher volume ambition, but it also raises the execution and capital intensity hurdles that have to be cleared before any improvement in margins or cash generation can show through.

Yet behind the showroom count and delivery surge, there is a financing and dilution risk investors should be aware of if cash burn does not ease...

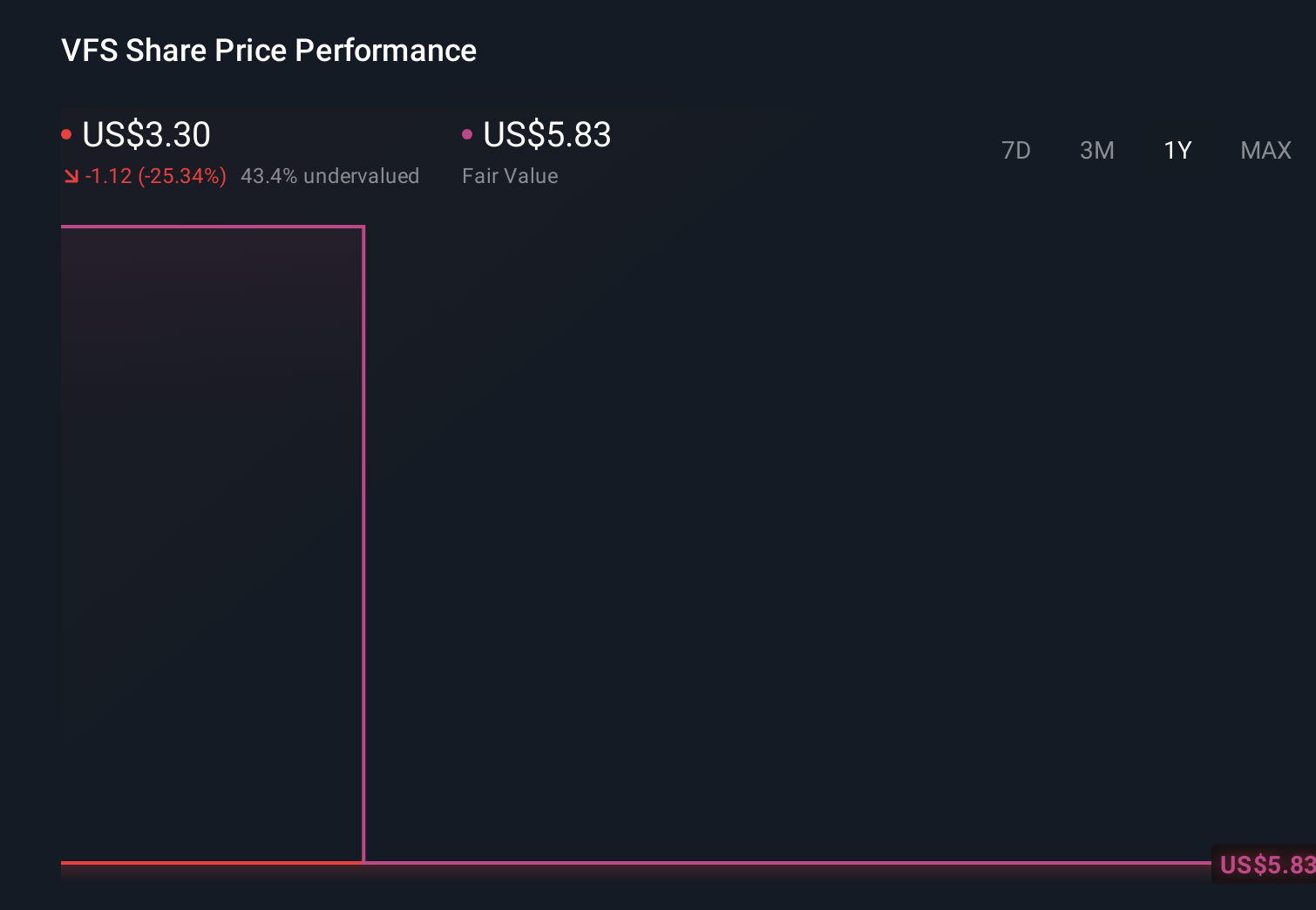

VinFast Auto’s narrative projects ₫239006.9 billion in revenue and ₫5494.0 billion in earnings by 2029. This requires 38.3% yearly revenue growth and an earnings increase of about ₫1.03e+05 billion from -₫97041.9 billion today.

Uncover how VinFast Auto's forecasts yield a $6.30 fair value, a 49% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts saw VinFast’s revenue growing about 41% a year and earnings swinging toward ₫9,301.1 billion, while also treating India expansion as a key execution risk, so this latest delivery and showroom news could either reinforce or challenge that far more bullish story.

Explore 5 other fair value estimates on VinFast Auto - why the stock might be a potential multi-bagger!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your VinFast Auto research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

- Our free VinFast Auto research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate VinFast Auto's overall financial health at a glance.

Curious About Other Options?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- Find 51 companies with promising cash flow potential yet trading below their fair value.

- Outshine the giants: these 17 early-stage AI stocks could fund your retirement.

- AI is about to change healthcare. These 33 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.