Should Wayfair's (W) Profit Rebound and Retail Expansion Change Investor Expectations?

Wayfair W | 0.00 |

- Wayfair Inc. recently reported its second quarter 2025 financial results, showing sales growth to US$3.27 billion and a return to net profitability, with basic earnings per share from continuing operations reaching US$0.11 compared to a loss a year ago.

- An interesting highlight is Wayfair's physical retail expansion, with the announcement of a new large-format store in Denver, marking its growing presence in the Mountain West and underscoring its focus on combining digital and in-person shopping experiences.

- We'll examine how Wayfair's improved profitability and continued retail expansion impact its long-term growth story and industry position.

Find companies with promising cash flow potential yet trading below their fair value.

Wayfair Investment Narrative Recap

The fundamental case for Wayfair centers on its ability to outpace a low-growth home goods market by expanding online and now physical presence, which could help it capture market share and drive profitability. The recent return to net profit and sustained sales growth in Q2 2025 reinforce this narrative, but do not meaningfully change the core short-term catalyst, sustained operating leverage through cost control and customer growth, or the biggest risk: softer home-buying and potential competitive pressure that could limit margin expansion.

The most relevant announcement is Wayfair’s new large-format Denver store, which highlights the company’s push into omnichannel retail. This physical expansion aligns with current catalysts tied to market share gains and customer experience improvements, but adds complexity and fixed costs at a time when the demand outlook for home furnishings remains uncertain.

By contrast, investors should be aware that increased investments in physical stores could expose Wayfair to underperformance risk if retail traffic doesn't meet expectations...

Wayfair's outlook forecasts $13.9 billion in revenue and $130.8 million in earnings by 2028. This scenario assumes annual revenue growth of 4.9% and an earnings increase of $430.8 million from current earnings of -$300 million.

Uncover how Wayfair's forecasts yield a $80.62 fair value, a 8% upside to its current price.

Exploring Other Perspectives

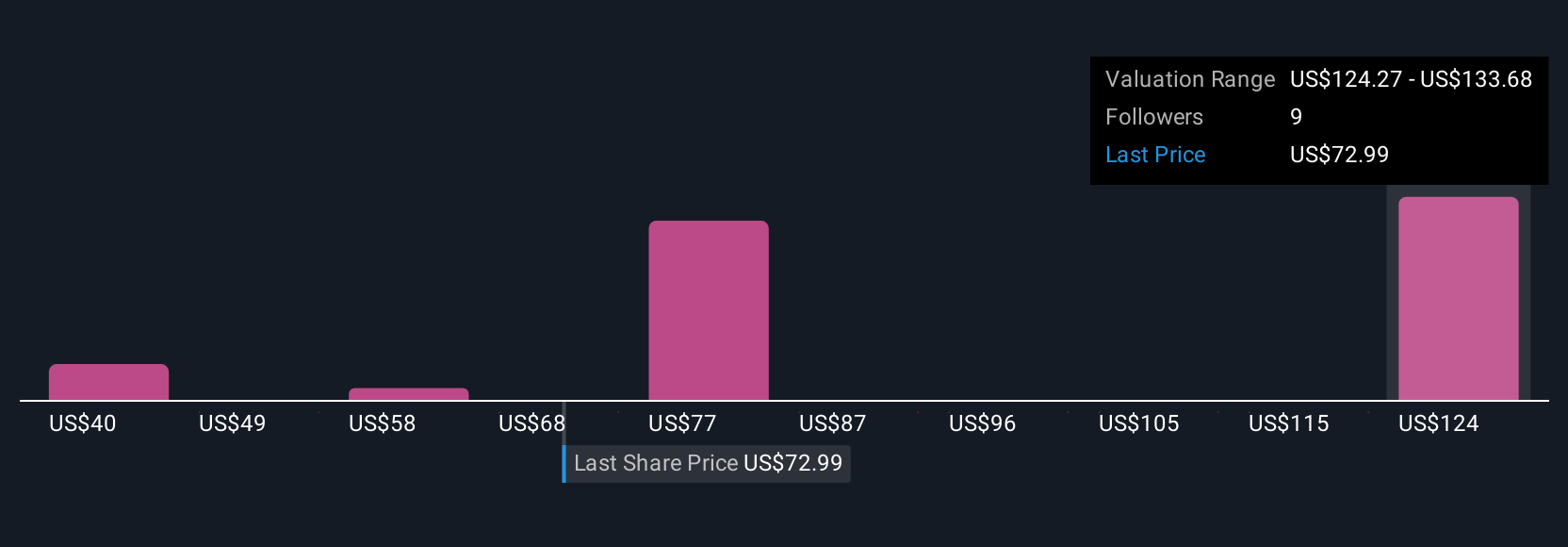

Five Simply Wall St Community members see Wayfair’s fair value spanning US$39.54 to US$133.80, a wide and varied spectrum. With physical retail expansion adding execution complexity, your view on long-term market share gains matters, consider what drives these sharply different outlooks.

Explore 5 other fair value estimates on Wayfair - why the stock might be worth as much as 79% more than the current price!

Build Your Own Wayfair Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Wayfair research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Wayfair research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Wayfair's overall financial health at a glance.

Searching For A Fresh Perspective?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- These 14 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- The end of cancer? These 26 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- We've found 19 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.