Should Willis Towers Watson's New CCS Insurance and Legal Scrutiny Require Action From WTW Investors?

Willis Towers Watson WTW | 0.00 |

- Earlier in May 2026, Willis Towers Watson declared a quarterly dividend of US$0.96 per share and introduced a Carbon Capture and Storage insurance suite spanning CO₂ capture, transport, storage, and related project risks.

- At the same time, the company faced growing legal and regulatory attention, including a lawsuit over alleged broker poaching and a shareholder-focused investigation tied to slower Q1 2026 organic revenue growth and margin pressure.

- Against this backdrop of new CCS insurance offerings and legal scrutiny over weaker Q1 performance, we'll assess how these developments reshape Willis Towers Watson's investment narrative.

Capitalize on the AI infrastructure supercycle with our selection of the 46 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

Willis Towers Watson Investment Narrative Recap

To own Willis Towers Watson you need to believe in its ability to grow fee based risk and advisory businesses while defending margins in a competitive market. The key near term swing factor is whether management can stabilise organic revenue growth after a softer Q1 2026, while the biggest risk is that legal, regulatory and competitive pressures further weigh on profitability. The latest dividend affirmation and product launch do not materially change that near term equation.

The most relevant recent announcement here is the new Carbon Capture and Storage insurance suite, which expands WTW’s specialty capabilities across an emerging project class. For investors focused on catalysts, this product underscores the company’s push into complex risk areas that can differentiate it from large peers, even as it works through questions around slower organic growth and margin pressure highlighted in the recent shareholder investigation.

Yet against these innovations, investors should still be aware of the growing legal and regulatory attention, including...

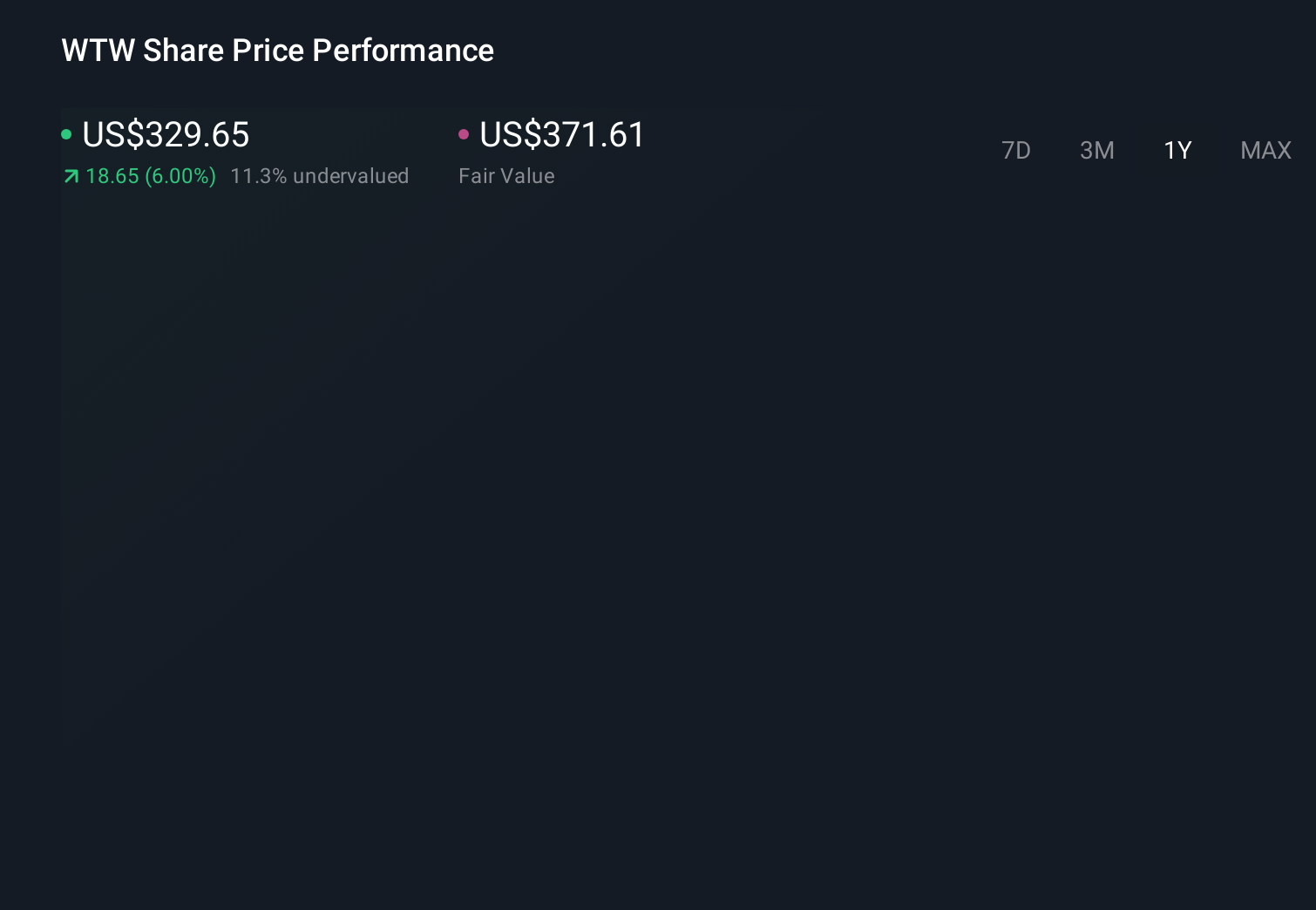

Willis Towers Watson's narrative projects $11.9 billion revenue and $1.8 billion earnings by 2029. This requires 6.9% yearly revenue growth and about a $0.2 billion earnings increase from $1.6 billion today.

Uncover how Willis Towers Watson's forecasts yield a $354.74 fair value, a 38% upside to its current price.

Exploring Other Perspectives

Two fair value estimates from the Simply Wall St Community cluster between US$354.74 and US$446.15, suggesting a wide range of independent views. You should weigh those against the recent concerns around slower organic revenue growth and margin pressure, which could influence how quickly any perceived discount might close.

Explore 2 other fair value estimates on Willis Towers Watson - why the stock might be worth just $354.74!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Willis Towers Watson research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Willis Towers Watson research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Willis Towers Watson's overall financial health at a glance.

Ready For A Different Approach?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- AI is about to change healthcare. These 34 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Uncover the next big thing with 25 elite penny stocks that balance risk and reward.

- Outshine the giants: these 13 early-stage AI stocks could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.