Should You Rethink Lattice Semiconductor After a 6% Weekly Drop Amid Industry Shifts?

Lattice Semiconductor Corporation LSCC | 95.54 95.47 | +3.00% -0.07% Post |

If you’re weighing what to do with your shares of Lattice Semiconductor or thinking about starting a position, you’re definitely not alone. After all, this stock has taken investors on a notable journey lately. Over just the past seven days, it slid by 6.2%, and it’s down 10.5% over the last month. Looking at the longer-term view, its performance is surprisingly robust, with a year-to-date gain of 19.6% and an impressive 101.4% rise over the last five years. These big moves can make for some tough decisions, especially when every dip and rally sparks fresh speculation about what’s driving the action.

One reason for the recent choppiness has been a wave of news highlighting shifting industry trends and rising demand in its core markets. Lattice’s focus on low-power programmable chips has become more relevant as broader sectors such as networking and industrial automation look for efficiency and new solutions. Even with the company’s innovations and growing relevance getting attention, investors haven’t always agreed on how much growth is already reflected in the stock price. This uncertainty is why valuation takes center stage.

Here’s something to consider: according to six fundamental valuation checks, Lattice Semiconductor isn’t currently undervalued in any category, scoring a 0 out of 6 on our value score. That doesn’t necessarily make it unattractive, but it does raise the question of how to value a business that’s performing well and is already recognized for doing so by the market. Let’s break down the different approaches to stock valuation for Lattice and provide a perspective that goes beyond the usual models to give you a clearer picture.

Lattice Semiconductor scores just 0/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

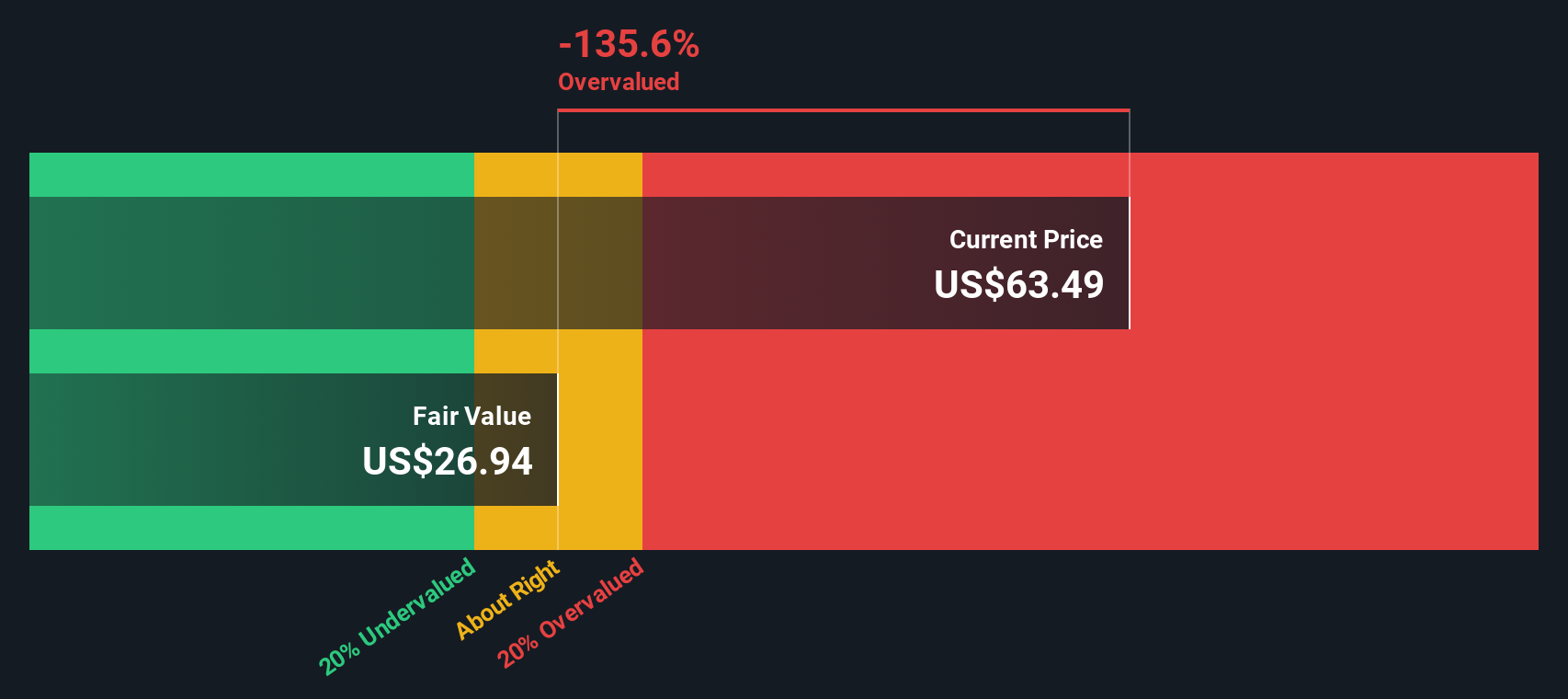

Approach 1: Lattice Semiconductor Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model estimates a company’s intrinsic value by projecting its future free cash flows and discounting them back to today’s value. This approach helps investors gauge what a business might be worth based on its cash-generating ability rather than just its current earnings or assets.

For Lattice Semiconductor, the current Free Cash Flow stands at $129 million. Analysts expect cash flows to grow over the next several years, reaching $208 million by 2026 and $228.85 million by 2027. Beyond these analyst forecasts, further projections are made using a consistent growth assumption, with expected free cash flow reaching $329 million by 2035. All cash flows are reported in US dollars.

Based on this DCF approach, the estimated intrinsic value per share comes out to $25.46. At present, the stock trades well above this value, implying it is 162.7% overvalued according to DCF analysis. This means that even though Lattice Semiconductor is generating healthy cash flows and is growing, the current share price already more than accounts for this optimism and potentially exceeds it.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Lattice Semiconductor may be overvalued by 162.7%. Find undervalued stocks or create your own screener to find better value opportunities.

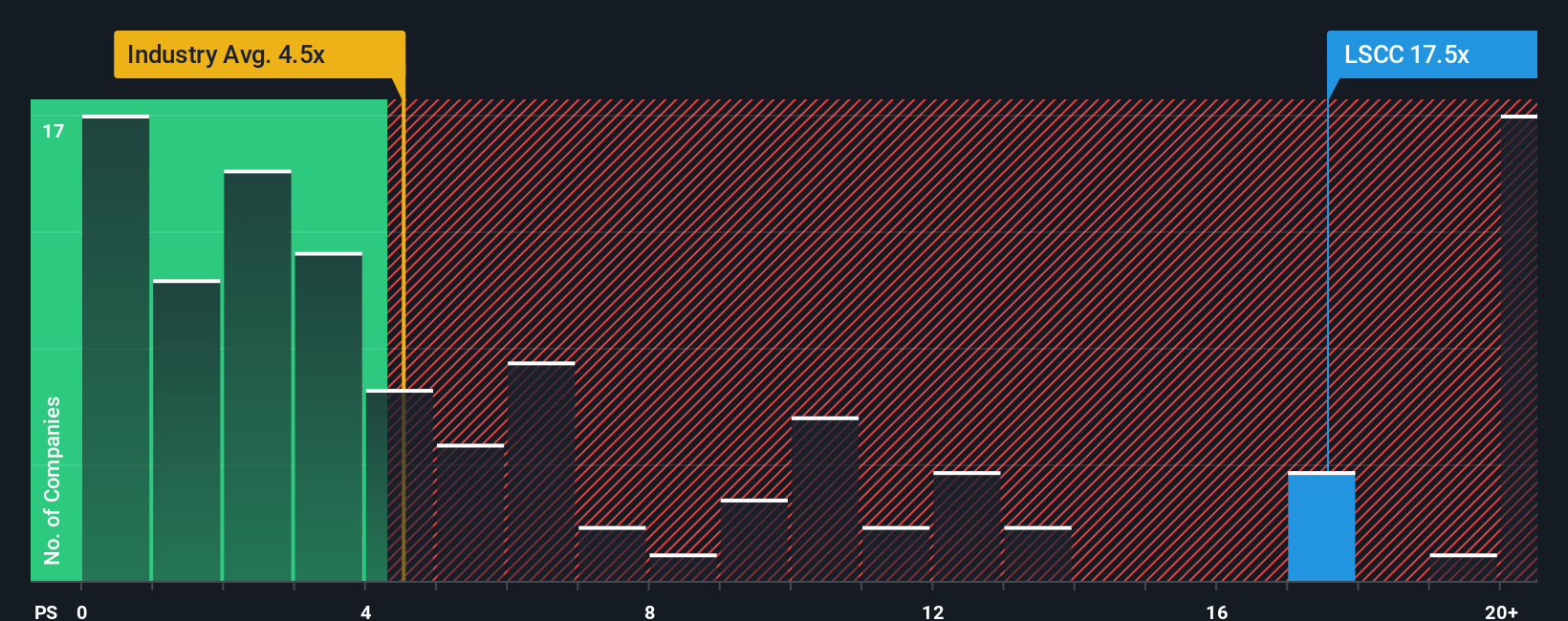

Approach 2: Lattice Semiconductor Price vs Sales

The Price-to-Sales (PS) ratio is a widely used valuation metric for profitable growth companies like Lattice Semiconductor, especially in sectors such as semiconductors where earnings can fluctuate but sales growth remains strong. The PS ratio helps investors see how highly the market is valuing each dollar of the company’s sales, and is often favored when profits are positive yet volatile due to investment cycles or market shifts.

What counts as a "fair" PS ratio varies depending on a company's growth prospects and risk profile. Companies with higher sales growth or lower risks tend to command premium multiples, while stable or lower-growth firms usually trade closer to their industry average. Comparing a company's PS ratio to its peers or the broader industry can provide helpful context, but it's important to account for differences in margins, growth, and business models.

Currently, Lattice Semiconductor’s PS ratio stands at 18.7x. This is almost double both its peer average of 9.4x and the semiconductor industry average of 5.1x. This indicates that the market has high expectations for the company's future. However, Simply Wall St’s "Fair Ratio" offers a deeper perspective by factoring in not just industry averages, but also the company’s profit margins, market cap, growth forecasts, and risks, resulting in a more tailored and holistic assessment than simply lining up numbers across peers.

Lattice’s Fair Ratio, calculated at 8.8x, is significantly lower than its current PS multiple. This suggests that, despite strong momentum and a proven track record, the market price may be stretching well ahead of the company’s fundamentals when all relevant factors are considered.

Result: OVERVALUED

PS ratios tell one story, but what if the real opportunity lies elsewhere? Discover companies where insiders are betting big on explosive growth.

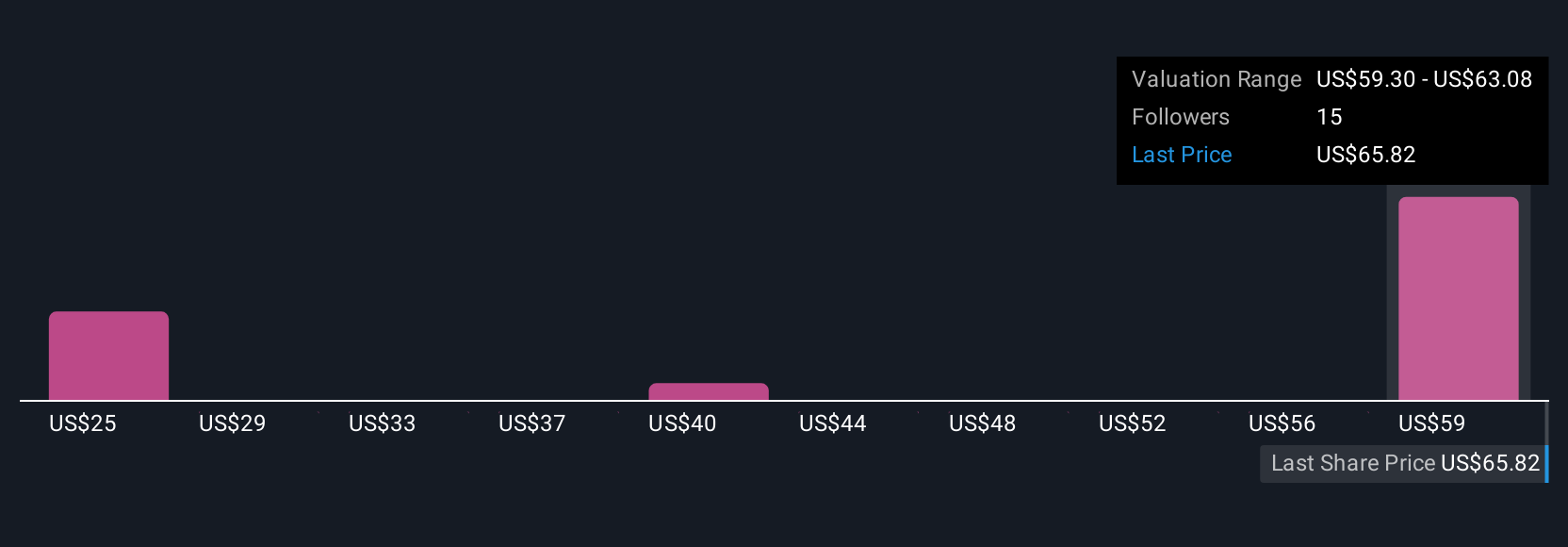

Upgrade Your Decision Making: Choose your Lattice Semiconductor Narrative

Earlier we mentioned that there is an even better way to understand valuation. Let's introduce you to Narratives. A Narrative is more than just a set of numbers; it is your personal, story-driven perspective that connects Lattice Semiconductor’s future prospects to concrete financial forecasts and fair value estimates. By defining your view on how the company will grow, such as assumptions about revenue, margins, or industry catalysts, you turn headlines and trends into a tailored, actionable investment scenario. Narratives bridge the gap between storytelling and valuation by linking your expectations to a calculated fair value. This helps you see clearly when the market price matches or diverges from your outlook.

Narratives are easy to create and compare on Simply Wall St’s Community page, where millions of investors share and update their investment theses in real time as news, earnings, or industry shifts occur. For example, some investors recently projected a bullish fair value of $72.00 per share for Lattice Semiconductor by focusing on accelerating AI and edge computing growth. Others see a more cautious scenario with a fair value of $52.00, emphasizing rising competition and industry risks. Comparing these dynamic Narratives empowers you to decide if now is a buying opportunity, a time to hold, or a signal to take profits, all based on the story you believe is most likely.

Do you think there's more to the story for Lattice Semiconductor? Create your own Narrative to let the Community know!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.