Should You Take a Fresh Look at Trade Desk After Its 12% Price Rebound?

Trade Desk, Inc. Class A TTD | 22.05 | +0.32% |

If you are wondering what to do with Trade Desk stock, you are definitely not alone. After all, the past year has been a roller coaster for investors, with the price sliding an eye-opening 57.7% over twelve months and tumbling even more sharply on a year-to-date basis. Yet, despite this gloomy long-term trend, the past month brought a surprising 12.4% rebound. Is this the start of a turnaround, or just another blip in a volatile period?

Much of this recent bounce can be linked to broader optimism in advertising technology stocks. Investors seem to be weighing fresh opportunities as marketers shift budgets and look for better digital ad targeting. This shift has given Trade Desk renewed attention. Still, the underlying numbers show risk perception remains high and the price is below where it traded five years ago.

When it comes to valuation, Trade Desk is getting noticed by those seeking discounts. The company is considered undervalued in 2 out of 6 valuation checks, giving it a value score of 2. That means there may be room for upside, but also some reasons for caution.

So, what exactly goes into these valuation checks, and how much should you trust them? Let us take a closer look at how analysts break down stock value and then dig into the numbers beneath the surface. Stick around to discover an even more insightful way to make sense of Trade Desk’s valuation by the end of this article.

Trade Desk scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

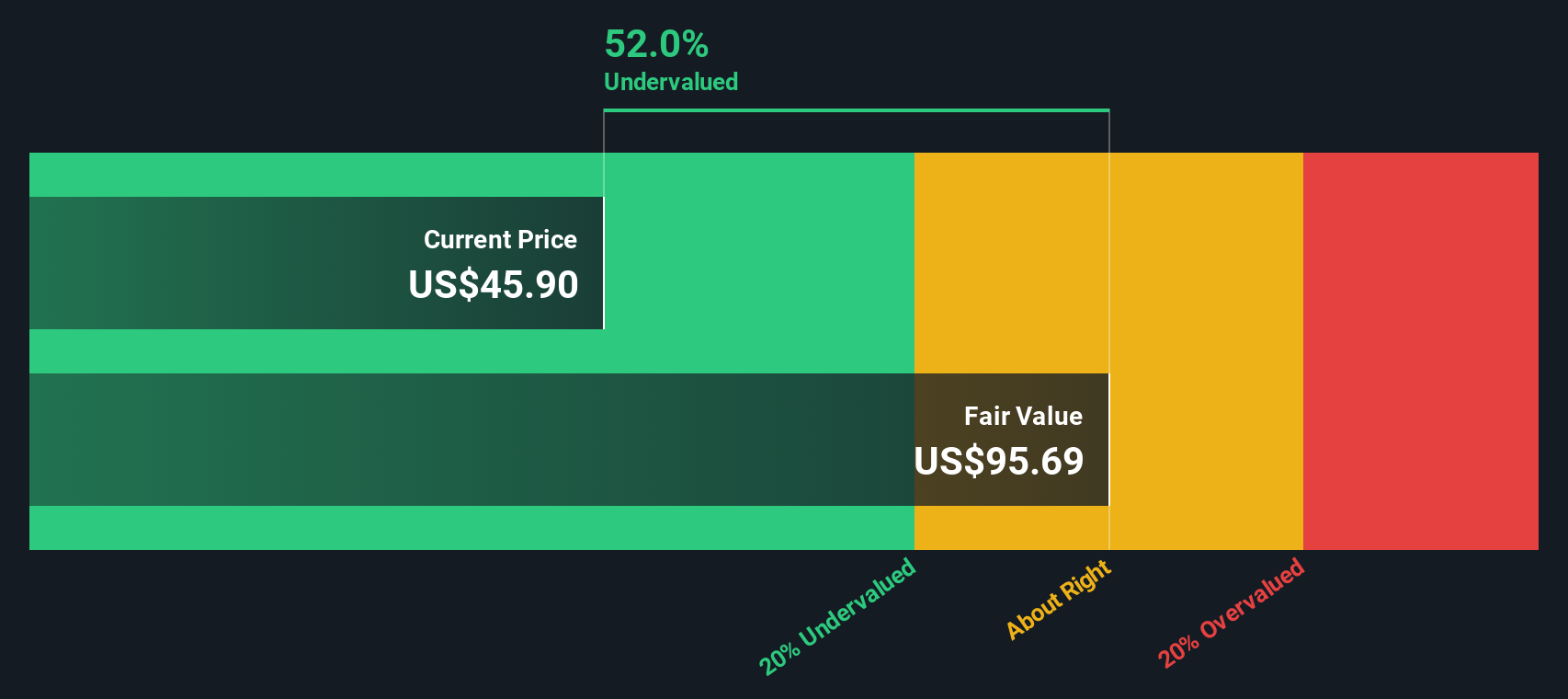

Approach 1: Trade Desk Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model estimates a company’s intrinsic value by projecting its future cash flows and then discounting these amounts back to their present value. This approach helps investors assess whether a stock is trading above or below what those future cash flows are really worth in today’s terms.

For Trade Desk, the latest reported Free Cash Flow sits at $787.5 Million. Analysts forecast steady growth, with annual Free Cash Flow expected to reach $1.57 Billion by 2029. While these forward-looking numbers rely on analyst estimates for the next five years, further out projections are advanced using Simply Wall St’s extrapolation models.

Using this data, the DCF model calculates a fair value of $96.49 per share. This suggests Trade Desk stock is trading at a 48.2% discount compared to its estimated intrinsic worth. According to the DCF model’s long-term outlook for rising cash flows, the current share price falls well below fair value and may represent an opportunity for investors seeking potential upside.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Trade Desk is undervalued by 48.2%. Track this in your watchlist or portfolio, or discover more undervalued stocks.

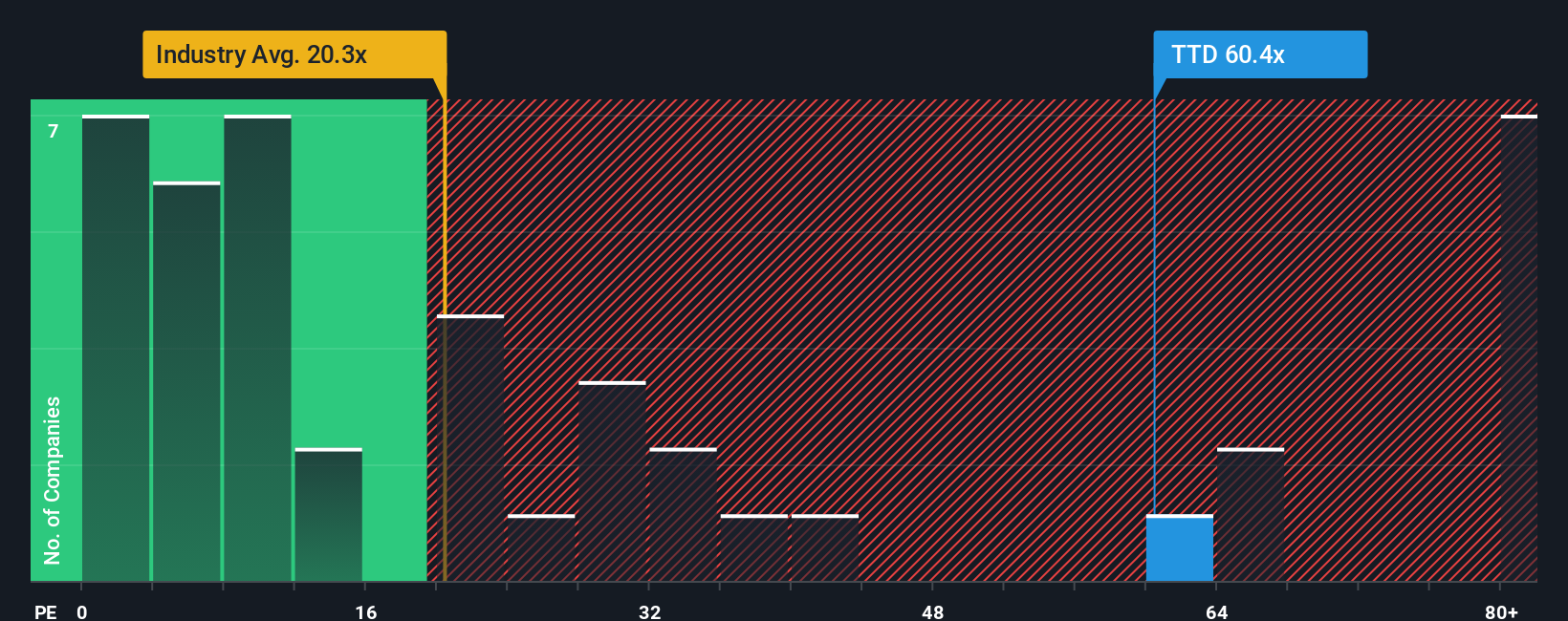

Approach 2: Trade Desk Price vs Earnings

For established, profitable companies like Trade Desk, the Price-to-Earnings (PE) ratio is a widely used and reliable valuation tool. It reflects how much investors are willing to pay for each dollar of the company's annual earnings, making it a clear guide to market sentiment on profitability and growth prospects.

A "normal" or appropriate PE ratio is shaped by how quickly investors expect a company’s earnings to grow and how much uncertainty they are willing to accept. Faster growth and lower risk often justify a higher PE multiple, while slower growth or higher risk typically lead to lower ratios.

Trade Desk currently trades at a PE ratio of 58.6x. This is substantially higher than both the media industry average of 19.0x and the average among similar peers at 31.4x. However, Simply Wall St’s proprietary Fair Ratio for Trade Desk is 30.6x. The Fair Ratio is a more refined benchmark than peer or industry comparisons alone because it incorporates factors specific to the company, including its earnings growth, profitability, industry context, size, and risk profile. By accounting for these nuances, the Fair Ratio gives a more tailored view of what would constitute a reasonable valuation for Trade Desk.

Comparing Trade Desk’s current PE of 58.6x to its Fair Ratio of 30.6x, the stock appears significantly overvalued based on current earnings. While the company’s robust growth story has driven up its valuation, it is trading well above what would be considered fair by this more holistic approach.

Result: OVERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover companies where insiders are betting big on explosive growth.

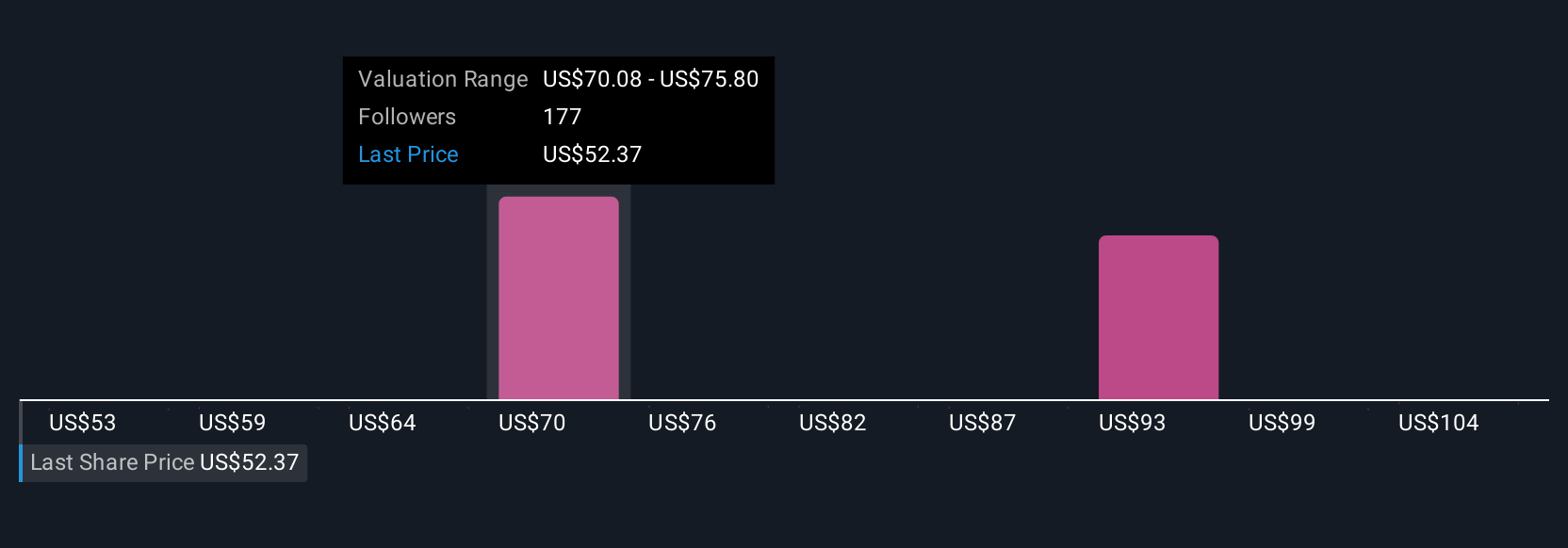

Upgrade Your Decision Making: Choose your Trade Desk Narrative

Earlier, we alluded to a better way to make sense of valuation, so let's introduce you to Narratives. A Narrative is simply your story about a company, informed by your unique perspective on its future opportunities and risks, tied directly to your assumptions about how its revenue, earnings, and profit margins might look in the years ahead.

Rather than only relying on static numbers, Narratives blend your personal investment outlook with a financial forecast, producing a customized fair value for the stock. This approach links what you believe about Trade Desk’s strengths and challenges to actionable data, giving meaning to both the company’s story and its numbers.

Narratives are available and easy to access within Simply Wall St’s Community page, used by millions of investors. They empower you to make buying or selling decisions by comparing your fair value with the current price and are kept up to date automatically when new company news or earnings emerge.

For example, with Trade Desk, one investor’s Narrative may anticipate continued rapid growth from CTV partnerships (projecting a fair value close to $135.00), while another sees increased industry headwinds and prefers a more conservative estimate (valuing the stock around $34.00). Your Narrative ensures your decisions reflect what you believe about the business, making investing both smarter and more personal.

Do you think there's more to the story for Trade Desk? Create your own Narrative to let the Community know!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.