Should Zscaler’s AI-Driven Zero Trust Expansion Amid Index Exit Require Action From ZS Investors?

Zscaler, Inc. ZS | 0.00 |

- Zscaler recently expanded its Zero Trust SASE platform with new AI- and agent-focused capabilities and announced integrations with Oasis Security, Radiant Logic, and Gigamon to strengthen identity governance and observability across complex hybrid environments.

- These moves deepen Zscaler’s role at the center of zero trust and AI security architectures, even as the company faces index removal, leadership turnover, and legal scrutiny that raise questions about its execution and governance.

- Against this backdrop of advanced AI security launches and index removal, we’ll examine how these developments reshape Zscaler’s investment narrative.

Explore 29 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

Zscaler Investment Narrative Recap

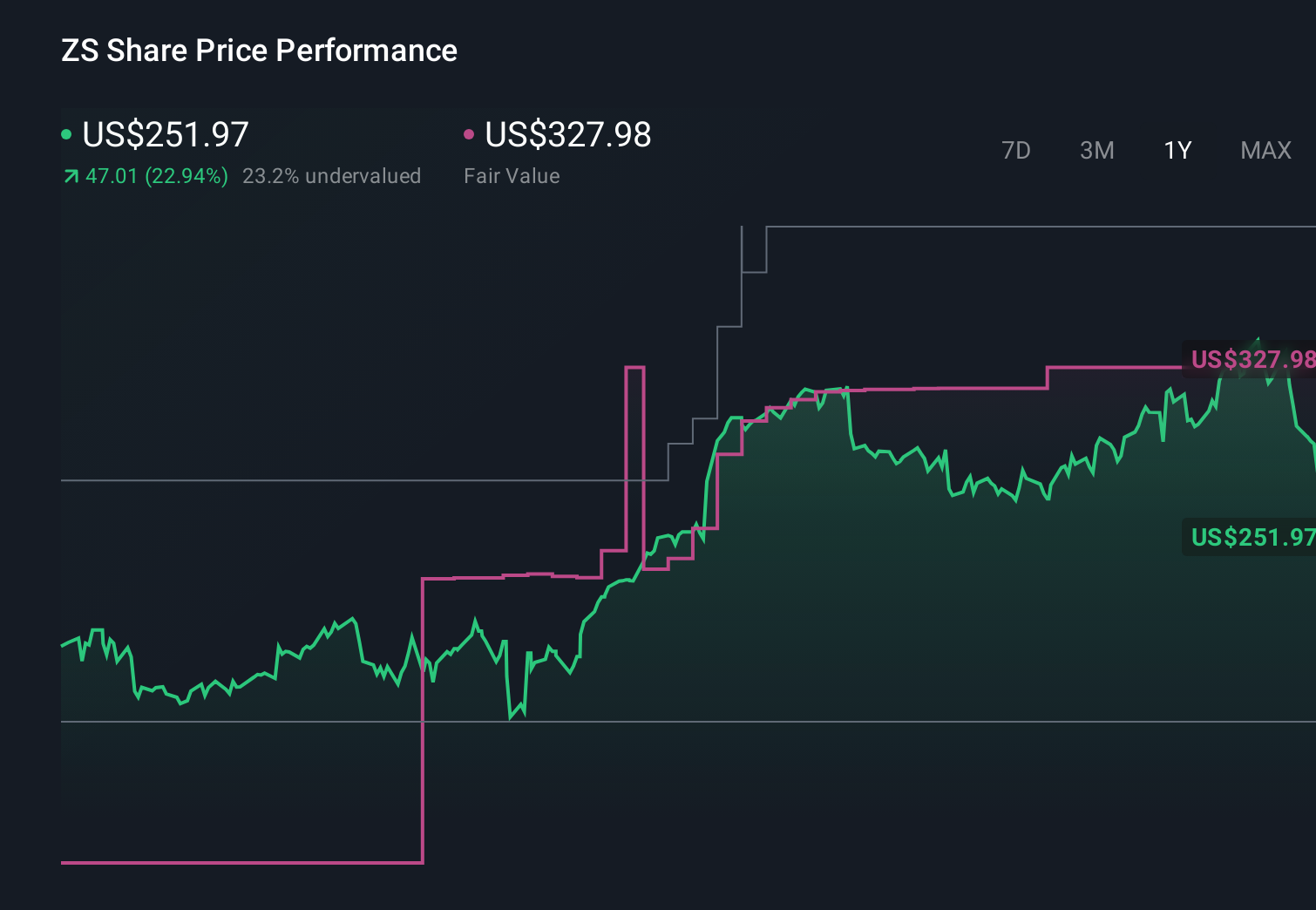

To own Zscaler, you need to believe zero trust and AI-centric security will keep pulling enterprises away from legacy firewalls and VPNs, and that Zscaler can convert that shift into durable, high-margin subscription revenue despite ongoing losses. Near term, the key catalyst is whether AI and Zero Trust SASE wins can re-anchor sentiment after the 31% post-guidance drop, while the biggest risk now is execution and governance scrutiny following index removal, insider selling, leadership churn, and multiple securities investigations.

Among the latest announcements, the Gigamon integration stands out for investors because it reinforces Zscaler Private Access with richer telemetry and visibility across hybrid environments, directly supporting the zero trust adoption and AI security catalysts. By pairing identity-aware access with deep application metadata, the partnership makes Zscaler’s platform more embedded in customers’ incident response and policy validation workflows, which could strengthen retention and cross-sell if enterprises keep consolidating around fewer cloud security vendors.

Yet investors should also be aware that, even as Zscaler deepens its AI security story, ongoing legal and governance overhangs could still weigh on...

Zscaler's narrative projects $5.2 billion revenue and $152.9 million earnings by 2029. This requires 19.9% yearly revenue growth and a $220.5 million earnings increase from -$67.6 million today.

Uncover how Zscaler's forecasts yield a $227.67 fair value, a 76% upside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts were already more cautious, assuming about US$4.9 billion of revenue and US$576.9 million of earnings by 2029, and they worry that aggressive AI security investment without clear efficiency gains could pressure margins far more than the recent product and partnership news implies.

Explore 5 other fair value estimates on Zscaler - why the stock might be worth just $193.05!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Zscaler research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Zscaler research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Zscaler's overall financial health at a glance.

Contemplating Other Strategies?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- We've uncovered the 8 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Find 43 companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.