Simpson Manufacturing (SSD) After The Housing Bill Passed And Why Valuation Still Looks Tight

Simpson Manufacturing Co., Inc. SSD | 0.00 |

Simpson Manufacturing (SSD) drew investor attention after Congress passed the bipartisan 21st Century ROAD to Housing Act, a housing supply bill targeting regulatory hurdles, builder volumes, and investor-owned homes in favor of new residential construction.

Against this backdrop, Simpson Manufacturing’s share price has gained momentum, with a 30 day share price return of 10.71% and a 90 day share price return of 25.66%. The 1 year total shareholder return of 34.63% points to solid longer term participation.

If the housing bill has you looking beyond a single construction supplier, it could be a good time to broaden your search with the 35 power grid technology and infrastructure stocks

With Simpson Manufacturing now trading near its recent highs and sitting only modestly below analysts’ price targets, the key question is whether the current valuation leaves much upside or if the market is already pricing in future growth.

Most Popular Narrative: 3.6% Undervalued

With Simpson Manufacturing last closing at $210.06 against a narrative fair value of $217.80, the current pricing sits only slightly below that central estimate while still reflecting a premium construction supplier with global reach.

The accelerating adoption of off-site, modular, and mass timber construction solutions is creating significant demand for high-performance, engineered fasteners and connectors, an area where Simpson continues to see double-digit OEM volume growth and increasing traction with new digital and software solutions. This is likely to support above-market revenue growth.

Want to see what sits behind that growth story? The narrative leans on steady top line expansion, rising margins, and a richer earnings multiple than the broader building sector. Curious which specific assumptions tie those pieces together into a fair value that edges above today’s share price?

Result: Fair Value of $217.80 (UNDERVALUED)

However, the Simpson Manufacturing story could be knocked off course if housing starts stay weak for longer, or if higher steel input costs squeeze margins more than expected.

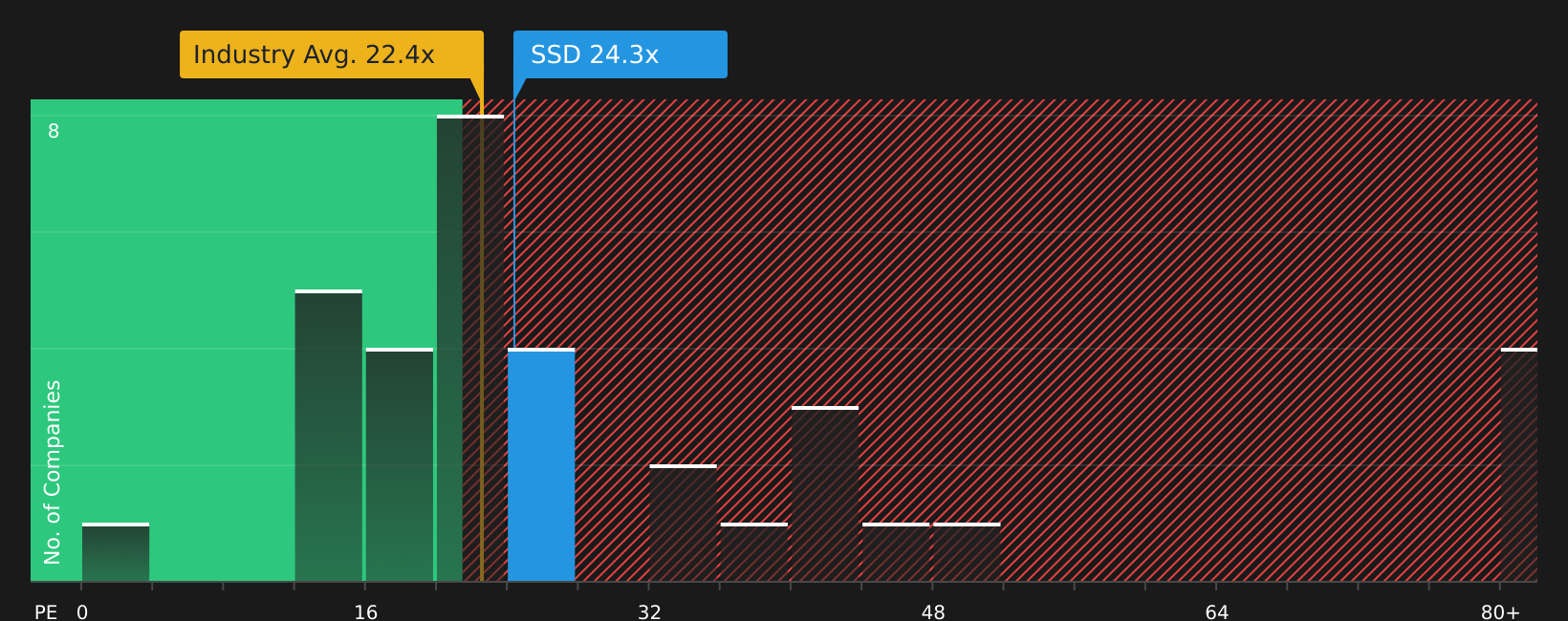

Another View: Simpson Manufacturing Through the P/E Lens

While the narrative fair value frames Simpson Manufacturing as modestly undervalued, the P/E snapshot tells a tighter story. The stock trades at 24.3x earnings, higher than the US Building industry at 22.4x and above a fair ratio of 22.9x. This points to less room for error if growth underdelivers.

For a closer look at how this earnings multiple stacks up against peers and that fair ratio, take a moment with the See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

With sentiment around Simpson Manufacturing skewing positive, this is a moment to move quickly, test the assumptions against the numbers, and build your own view using the 2 key rewards

Looking for more investment ideas beyond Simpson Manufacturing?

If you only focus on Simpson Manufacturing, you might miss other compelling setups across sectors, position sizes, and risk profiles that could better match your goals.

- Target potential high growth opportunities early by scanning through 21 elite penny stocks with strong financials that already show stronger financial foundations than many peers.

- Zero in on quality at a sensible price by using the 44 high quality undervalued stocks to spot stocks where fundamentals and valuation appear more closely aligned.

- Prioritize resilience and capital preservation with the 71 resilient stocks with low risk scores to find companies that may better suit a steadier, lower volatility approach.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.