SLB Wins Major Middle East Deals While Trading Below Estimated Fair Value

SLB Limited SLB | 49.44 | -1.18% |

- SLB (NYSE:SLB) has secured a $1.5b, five year contract from Kuwait Oil Company to develop the Mutriba field, involving high pressure, high temperature reservoirs and environmental considerations.

- The company also won new five year contracts in Oman for wellhead and artificial lift technologies, expanding its role across key production infrastructure.

- Together, these awards point to growing demand for end to end service models in complex international energy projects.

For investors watching NYSE:SLB, these contract wins come with the stock at $50.32 and a 25.2% return year to date, alongside a 24.1% return over the past year. The company is increasingly tied to large, technically demanding projects in the Middle East, where long term contracts can support more predictable activity and equipment deployment.

The Kuwait and Oman deals also highlight how major operators are leaning on a smaller set of service providers to handle everything from subsurface work to production support. If this pattern continues across other regions, investors will likely pay close attention to how SLB converts these awards into execution quality, cash flow and future tender momentum.

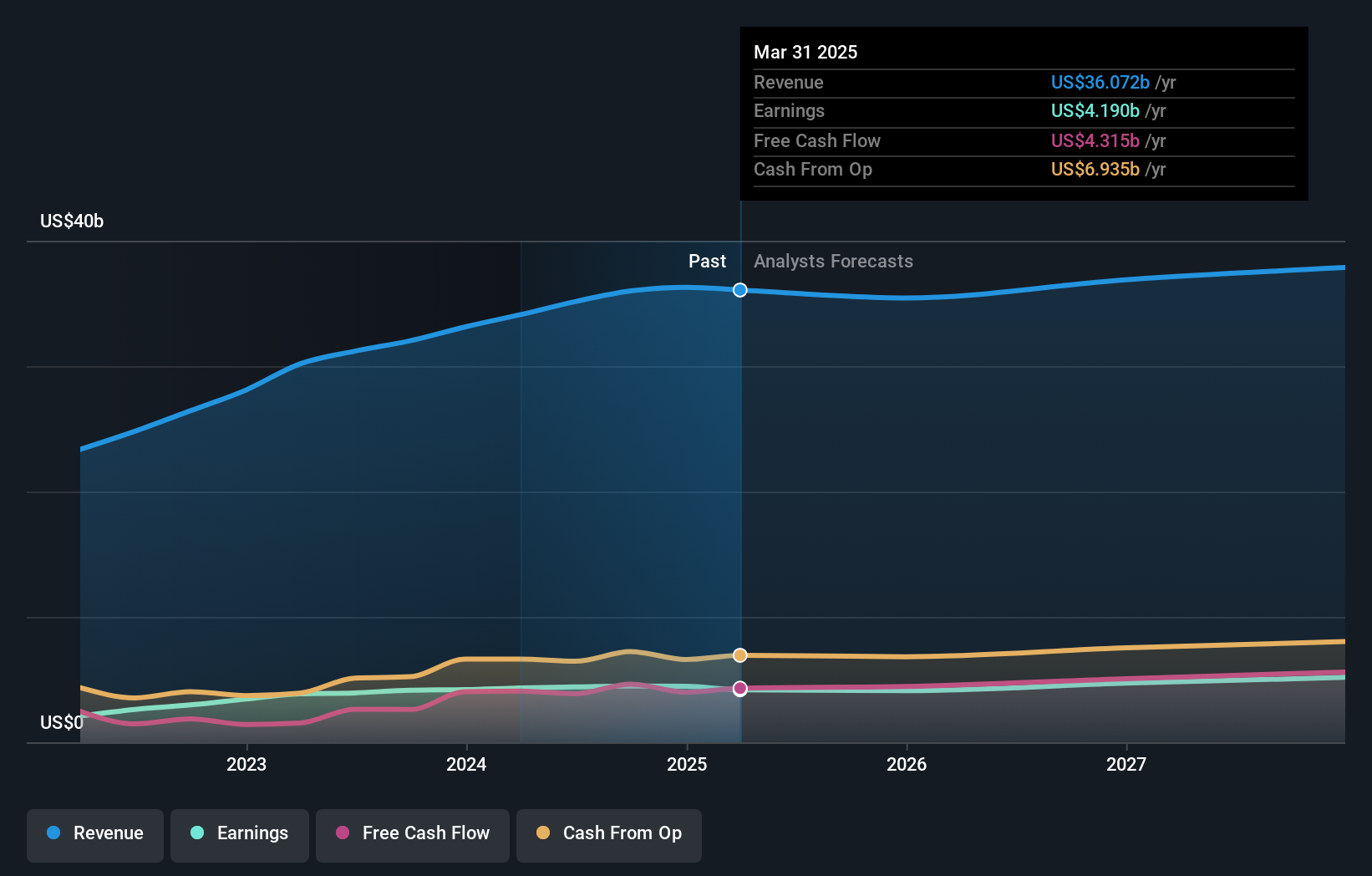

Stay updated on the most important news stories for SLB by adding it to your watchlist or portfolio. Alternatively, explore our Community to discover new perspectives on SLB.

Quick Assessment

- ⚖️ Price vs Analyst Target: At US$50.32 versus a consensus target of US$54.08, the price is about 7% below analyst expectations.

- ✅ Simply Wall St Valuation: SLB is flagged as trading 38.6% below estimated fair value, which is a sizable valuation gap.

- ✅ Recent Momentum: The 30 day return of roughly 11.3% suggests buyers have been in control recently.

There is only one way to know the right time to buy, sell or hold SLB. Head to Simply Wall St's company report for the latest analysis of SLB's Fair Value.

Key Considerations

- 📊 The Kuwait and Oman awards extend SLB's role in high pressure, high temperature and production support work, which could support longer visibility on activity and equipment usage.

- 📊 Keep an eye on how these contracts feed into revenue, margins and cash flow, especially with SLB trading at a P/E of about 22.3 versus an Energy Services average of roughly 24.7.

- ⚠️ One identified risk is an unstable dividend track record, so income focused investors may want to watch payout consistency alongside project execution.

Dig Deeper

For the full picture including more risks and rewards, check out the complete SLB analysis. Alternatively, you can visit the community page for SLB to see how other investors believe this latest news will impact the company's narrative.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.