Slower Demand And Modest Returns Might Change The Case For Investing In Ingersoll Rand (IR)

Ingersoll Rand Inc. IR | 0.00 |

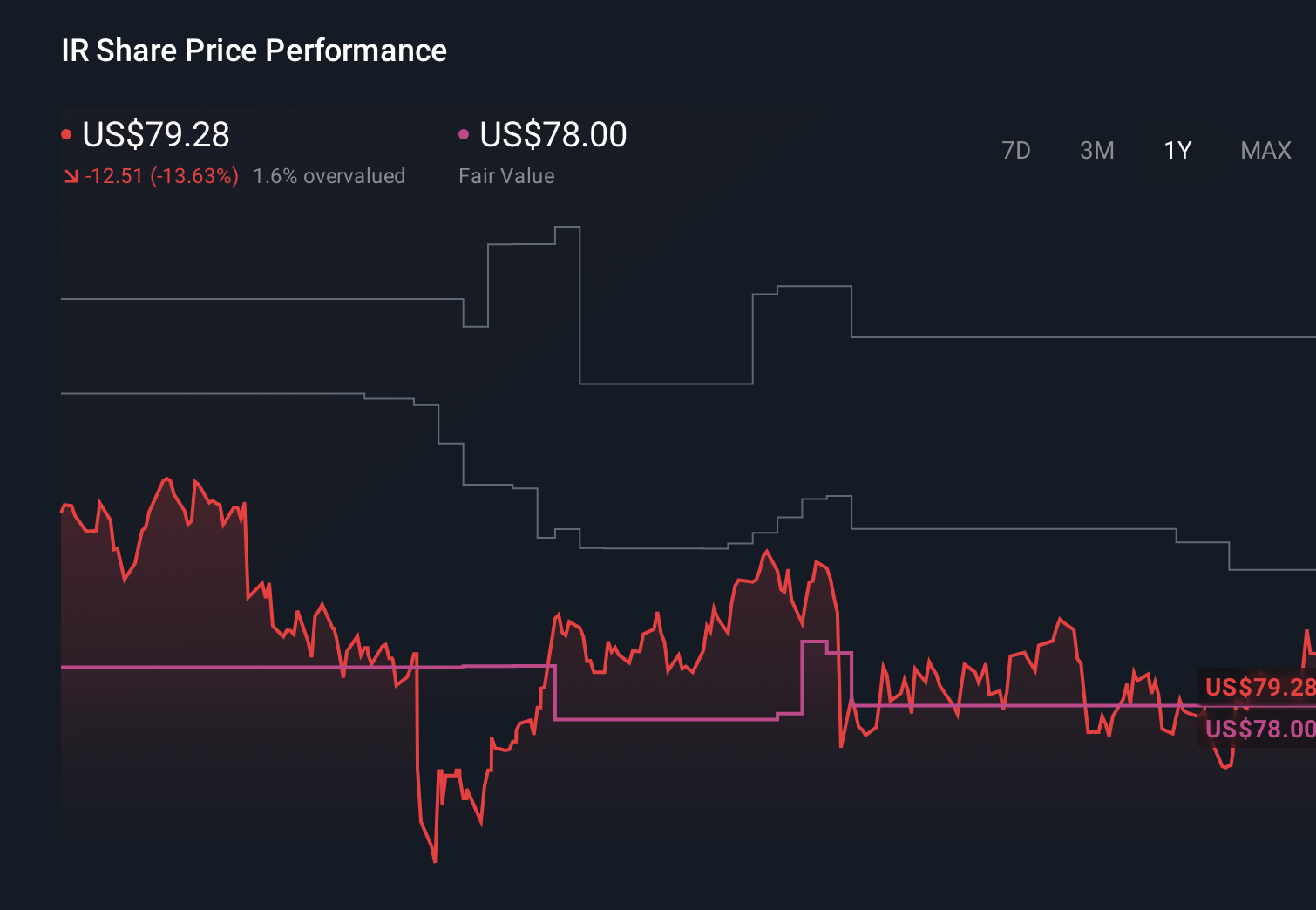

- In the past few days, commentary on Ingersoll Rand has highlighted that its mission-critical flow creation business has delivered organic revenue growth below industry benchmarks over the last two years, with estimated sales growth of 3.1% for the next 12 months pointing to a potential demand slowdown.

- An additional concern is the company’s 6.1% return on capital, which raises questions about how effectively management is converting investments into profitable growth opportunities.

- We’ll now explore how concerns about slower demand and modest returns on capital could influence Ingersoll Rand’s existing investment narrative.

Explore 30 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

Ingersoll Rand Investment Narrative Recap

To own Ingersoll Rand, you need to believe its mission critical flow creation franchise can translate product innovation and aftermarket services into durable earnings, despite current questions over demand and capital efficiency. The recent commentary on slower organic growth and a 6.1% return on capital reinforces near term concerns around muted order trends and capital allocation, but it does not appear to fundamentally alter the main catalyst, which remains execution on higher margin, sustainability focused offerings, or the key risk of prolonged demand softness in core industrial markets.

The recent multiyear partnership with Garrett Motion to co develop next generation oil free air technologies is particularly relevant here, because it speaks directly to the efficiency and sustainability themes that underpin Ingersoll Rand’s product led catalyst. While this collaboration is longer dated, its success could influence how investors weigh slower near term revenue growth against the potential for higher value, energy efficient solutions to support pricing, margins, and incremental returns on capital over time.

Yet beneath the innovation story, there is a risk around weaker organic orders and what that might really mean for future demand trends that investors should be aware of...

Ingersoll Rand's narrative projects $9.0 billion revenue and $1.4 billion earnings by 2029. This requires 4.9% yearly revenue growth and roughly a $0.8 billion earnings increase from $587.0 million.

Uncover how Ingersoll Rand's forecasts yield a $93.20 fair value, a 29% upside to its current price.

Exploring Other Perspectives

Before this news, the most optimistic analysts were assuming around US$8.8 billion in revenue and US$1.5 billion in earnings by 2028, yet the latest signals on slower organic growth and pressured returns on capital show how far opinions can differ and why you may want to compare that upbeat view with the risk that expansion into underpenetrated markets does not deliver as smoothly as hoped.

Explore 3 other fair value estimates on Ingersoll Rand - why the stock might be worth as much as 29% more than the current price!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Ingersoll Rand research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Ingersoll Rand research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Ingersoll Rand's overall financial health at a glance.

Curious About Other Options?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- Capitalize on the AI infrastructure supercycle with our selection of the 48 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- AI is about to change healthcare. These 39 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.