Somnigroup International (SGI) Valuation Check After Rebrand And Mattress Firm Integration Progress

Somnigroup International Inc. SGI | 72.90 | -0.96% |

Somnigroup International (SGI), formerly Tempur Sealy International, has attracted fresh attention after its rebrand in February 2025, prompting investors to reassess the bedding company’s recent share performance and underlying fundamentals.

At a share price of $92.68, Somnigroup’s recent trading has cooled slightly, with a 2.1% one day and 1.4% seven day share price pullback. This comes even as its 90 day share price return of 12.4% and one year total shareholder return of 55.6% point to momentum built over a longer stretch.

If this rebrand has you rethinking the sleep sector, it can also be a good moment to broaden your watchlist and check out fast growing stocks with high insider ownership.

With the stock at $92.68, sitting about 10% below the average analyst price target and trading on strong 1 year and multi year returns, should you view Somnigroup as undervalued at its current level, or is the market already fully reflecting expectations for future growth?

Most Popular Narrative: 9.4% Undervalued

Somnigroup’s most followed valuation narrative puts fair value at $102.29 per share, which sits above the recent $92.68 close and frames the current pullback in a different light.

The integration of Mattress Firm is already generating meaningful sales and cost synergies, with $100 million in annual net cost synergies projected and sales synergies ahead of schedule; these operational improvements are set to expand EBITDA and enhance net margins moving into 2026 and beyond.

Curious what kind of revenue trajectory and margin rebuild would need to support that higher value, and how long earnings would have to compound to get there? The full narrative sets out a detailed earnings bridge and a future earnings multiple that is usually reserved for faster growing consumer names. If you want to see exactly which assumptions do the heavy lifting in that $102.29 fair value, the next step is to read it in full.

Result: Fair Value of $102.29 (UNDERVALUED)

However, this hinges on mattress demand holding up and Mattress Firm’s integration staying on track, since weaker consumer spending or execution hiccups could quickly challenge that bullish setup.

Another View: Rich P/E Puts Pressure On The Story

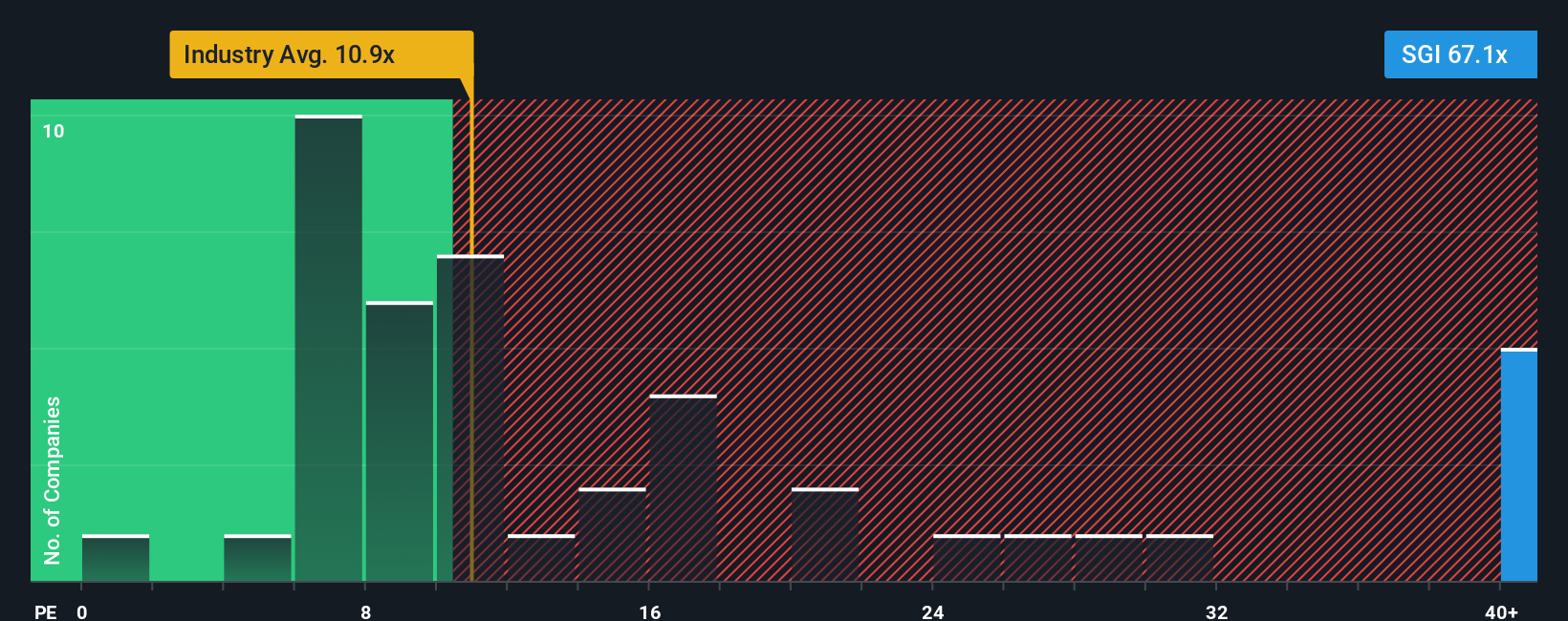

That $102.29 fair value suggests upside, but the current P/E of 61.7x tells a different story. It is far higher than both the US Consumer Durables average of 11.3x and peers at 14.4x, and also well above a fair ratio of 27.6x, which points to meaningful valuation risk if expectations fade.

Build Your Own Somnigroup International Narrative

If you do not see the story the same way, or just prefer to test the numbers yourself, you can build a tailored view in minutes with Do it your way.

A great starting point for your Somnigroup International research is our analysis highlighting 1 key reward and 3 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Before you move on, you may want to scan a few focused stock lists built from the same data engine to spot opportunities you might otherwise miss.

- Spot companies the market may be overlooking by checking out these 871 undervalued stocks based on cash flows, which stand out on cash flow based metrics.

- Catch early movers at the smaller end of the market by reviewing these 3523 penny stocks with strong financials with stronger balance sheets and fundamentals.

- Position yourself ahead of major tech shifts by scanning these 23 quantum computing stocks that are shaping advances in computing and related applications.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.