Southwest’s Wine-Friendly Santa Rosa Push Might Change The Case For Investing In Southwest Airlines (LUV)

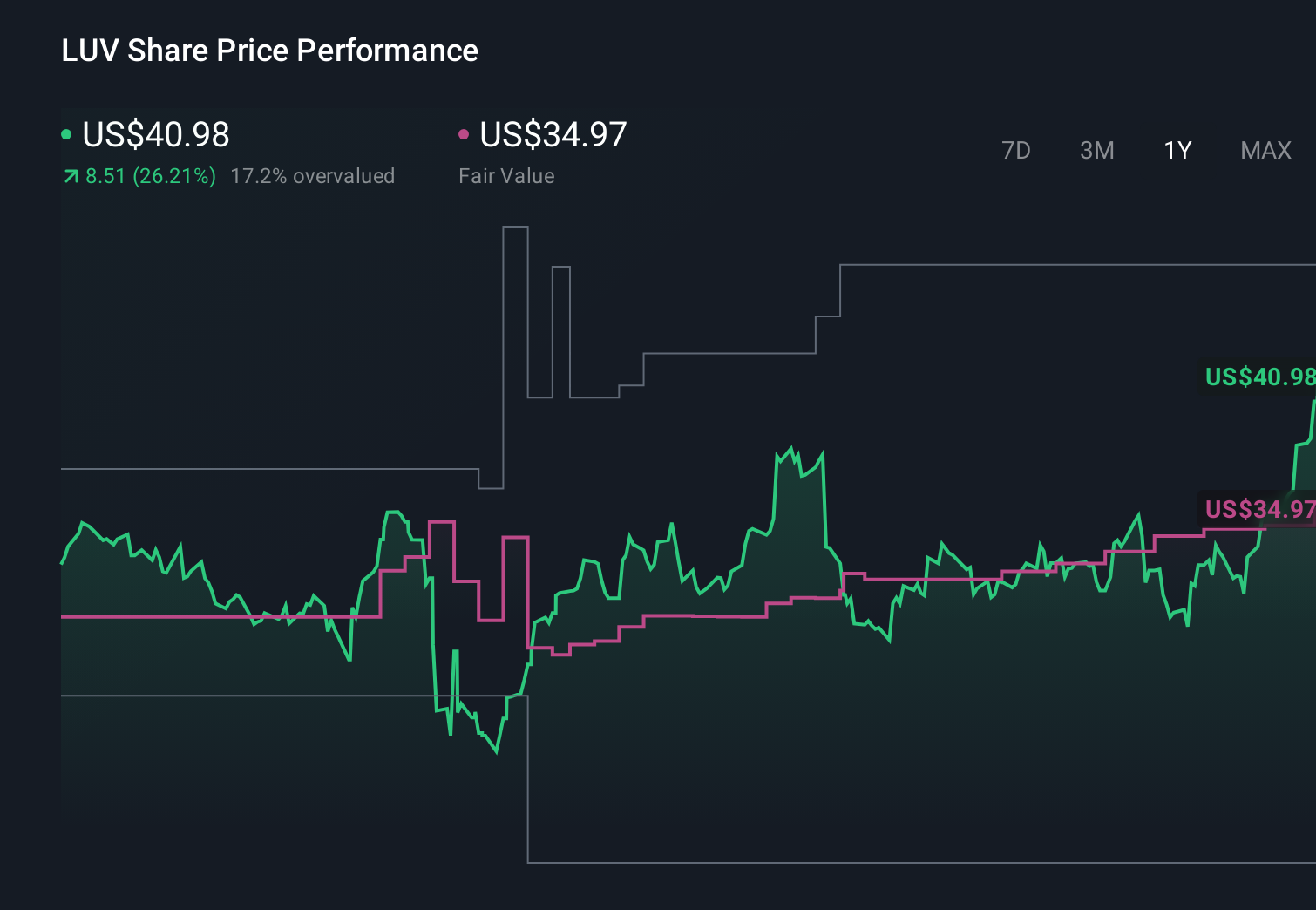

Southwest Airlines Co. LUV | 39.56 | -1.62% |

- Southwest Airlines recently began service at Santa Rosa’s Charles M. Schulz Sonoma County Airport, adding nonstop flights to San Diego, Las Vegas, Denver, and Burbank, while also continuing broader network expansion to destinations such as St. Thomas, St. Maarten, Knoxville, and Anchorage.

- The carrier also introduced its Sip and Ship program, letting customers check one case of wine for free from select West Coast airports, underscoring a focus on differentiated perks amid rising fuel costs and operational pressures.

- We’ll now examine how Southwest’s wine-friendly Santa Rosa expansion fits into its broader investment narrative amid sharply higher jet fuel costs.

Find 61 companies with promising cash flow potential yet trading below their fair value.

Southwest Airlines Investment Narrative Recap

To own Southwest today, you need to believe its shift toward higher-yield products and a wider network can offset margin pressure from sharply higher jet fuel costs and rising labor expenses. The Santa Rosa launch and wine-friendly “Sip and Ship” perk support Southwest’s brand and ancillary revenue efforts, but they are not a material offset to the near term fuel shock, which remains the key catalyst and the most immediate risk to earnings.

The Santa Rosa expansion lands alongside Southwest’s broader push to refresh its product, including the rollout of assigned and premium seating tiers in 2025. That fare revamp is far more central to the near term investment story than a single new station, because it is designed to lift revenue per seat and help fund higher operating costs. Santa Rosa’s added leisure demand may complement those initiatives, but investors will still be watching fuel and pricing power first.

Yet, even as Southwest leans into new fees and wine friendly routes, investors should be aware that jet fuel volatility and the end of hedging could...

Southwest Airlines' narrative projects $34.6 billion revenue and $2.4 billion earnings by 2029.

Uncover how Southwest Airlines' forecasts yield a $44.82 fair value, a 18% upside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts were already cautious, assuming earnings of about US$1.5 billion by 2028 and a 7.2x PE. Compared with concerns about fuel exposure and capacity risk, that more pessimistic view highlights how sharply opinions can differ, and why fresh developments like Santa Rosa and Sip and Ship could eventually shift both the bull and bear cases.

Explore 4 other fair value estimates on Southwest Airlines - why the stock might be worth just $44.82!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Southwest Airlines research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Southwest Airlines research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Southwest Airlines' overall financial health at a glance.

Seeking Other Investments?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- Outshine the giants: these 20 early-stage AI stocks could fund your retirement.

- The future of work is here. Discover the 34 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- The latest GPUs need a type of rare earth metal called Neodymium and there are only 27 companies in the world exploring or producing it. Find the list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.