Spectrum Brands (SPB) Is Down 6.3% After Strong Q2 Earnings And Acquisition Plans Update

Spectrum Brands Holdings, Inc. SPB | 0.00 |

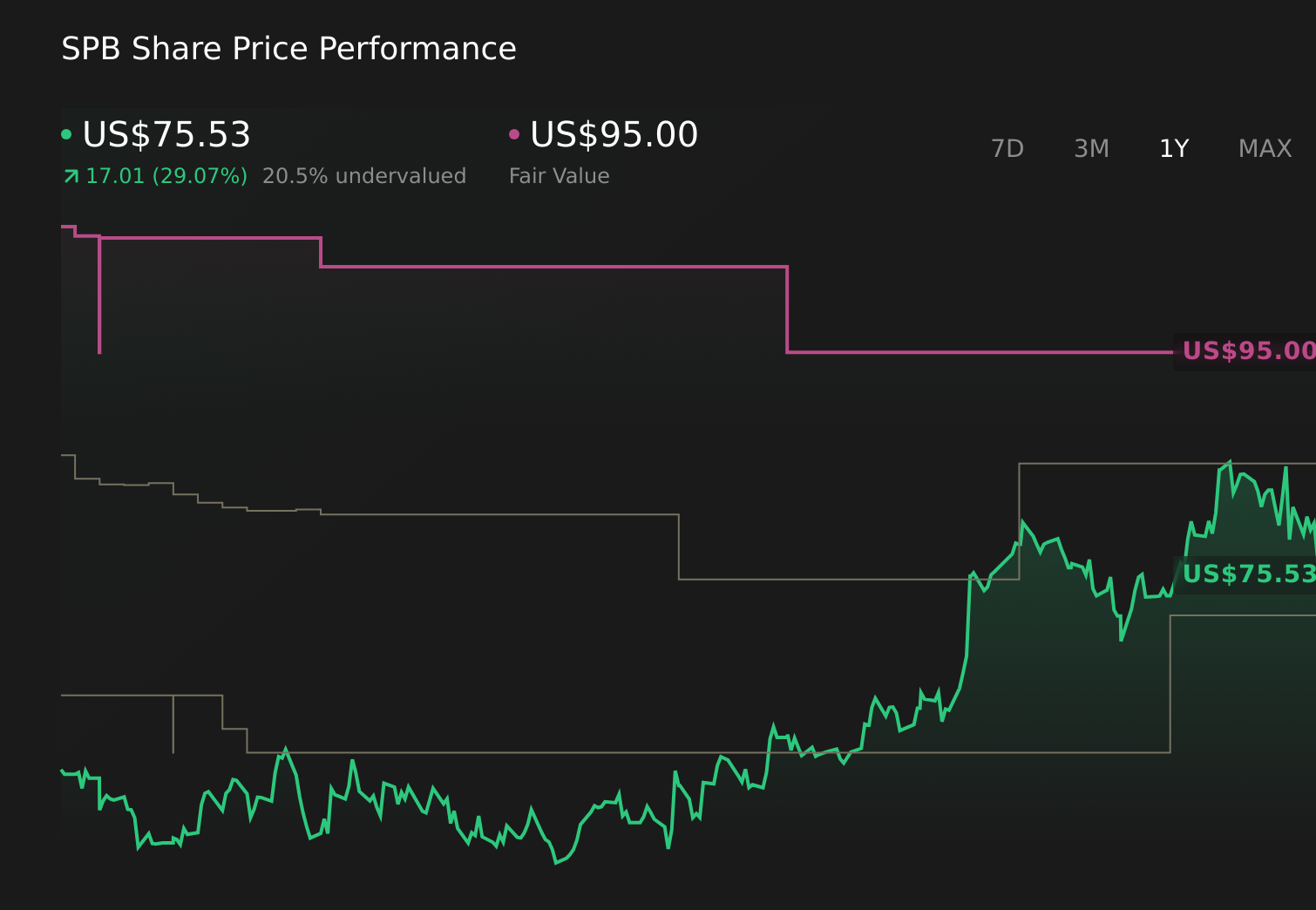

- In its second-quarter 2026 results, Spectrum Brands Holdings reported higher sales of US$708.9 million and net income of US$22.1 million compared with the prior year, alongside sharply improved earnings per share from continuing operations.

- Management also highlighted a healthy balance sheet and reiterated plans to pursue disciplined acquisitions in its Pet and Home & Garden segments, positioning the company as a potential consolidator in those categories.

- We’ll now examine how Spectrum Brands’ stronger earnings and renewed acquisition push may influence its existing investment narrative and outlook.

Outshine the giants: these 14 early-stage AI stocks could fund your retirement.

Spectrum Brands Holdings Investment Narrative Recap

To own Spectrum Brands today, you need to believe in a steady, cash generative consumer business where pet care and Home & Garden remain core earnings engines. The latest quarter’s higher sales and sharply better profitability support that case in the near term, while the renewed push for acquisitions could be a key catalyst if deals are executed prudently. The biggest near term risk remains category and retailer pressure that could squeeze margins if consumer demand softens again.

The most relevant recent announcement alongside the earnings is management’s reaffirmed focus on disciplined M&A in Pet and Home & Garden, backed by what it calls a healthy balance sheet. That matters because it links the improved earnings and ongoing capital access directly to the stated plan to act as a consolidator, which many investors already view as a key potential driver of Spectrum’s story over the next few years.

Yet investors should also be aware that heavy dependence on a handful of large retailers could quickly matter if...

Spectrum Brands Holdings' narrative projects $3.0 billion revenue and $124.7 million earnings by 2029.

Uncover how Spectrum Brands Holdings' forecasts yield a $85.29 fair value, a 14% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts already expected Spectrum to reach about US$3.0 billion in revenue and roughly US$148 million in earnings, and they see the current M&A push as a way to offset risks from retailer concentration, which they view much more harshly than the consensus. If you are weighing today’s stronger results against those bullish forecasts, it is worth remembering that these views were set before this quarter’s news and might shift as the acquisition story unfolds.

Explore 3 other fair value estimates on Spectrum Brands Holdings - why the stock might be worth just $85.29!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Spectrum Brands Holdings research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Spectrum Brands Holdings research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Spectrum Brands Holdings' overall financial health at a glance.

Curious About Other Options?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- The latest GPUs need a type of rare earth metal called Dysprosium and there are only 28 companies in the world exploring or producing it. Find the list for free.

- Uncover the next big thing with 27 elite penny stocks that balance risk and reward.

- Explore 26 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.