SPX Technologies (SPXC) Stock May Trade At A Premium Following Its 236% Run

SPX Technologies, Inc. SPXC | 0.00 |

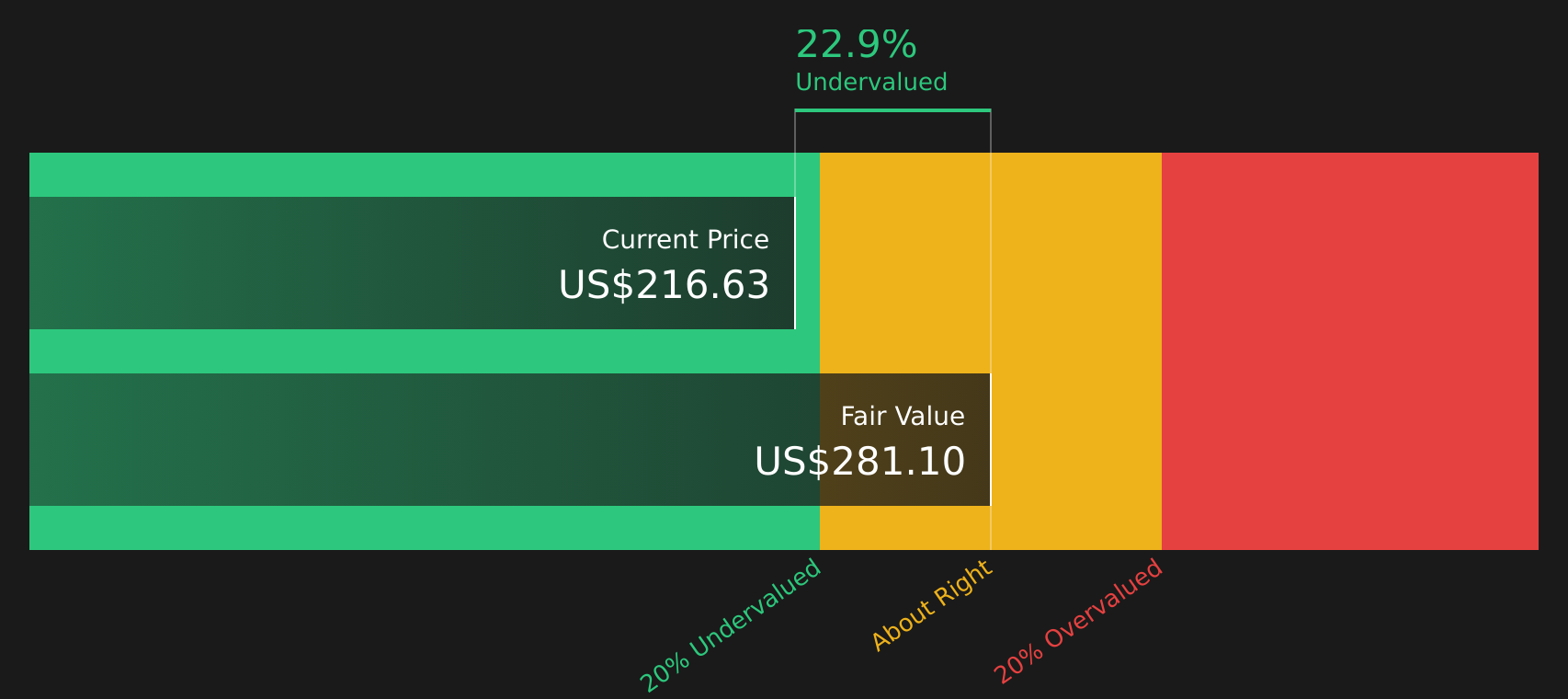

SPX Technologies stock has delivered a very strong 235.7% return over the past five years, yet the valuation signals are split, with a Discounted Cash Flow (DCF) estimate pointing to roughly 23.2% upside to intrinsic value while earnings multiples paint a richer picture.

- Over five years, SPX Technologies has returned 235.7%, which puts extra focus on whether the recent share price now builds in most of the good news.

- Growing data center cooling demand in the HVAC segment can support higher revenue expectations, while the stock trading around 44 times earnings may limit how much more investors are willing to pay if growth or cash flow timing disappoints.

- On Simply Wall St's valuation checks, SPX Technologies passes 3 of 6 tests, so the overall assessment is a mixed picture rather than a clear bargain or clear overvaluation (3/6 score).

The stock's next move may depend on whether SPX Technologies ultimately trades closer to its intrinsic value estimate or to the richer signals implied by its P/E multiple.

Is SPX Technologies Still Cheap on Cash Flow?

The Discounted Cash Flow (DCF) approach estimates what SPX Technologies is worth today based on the cash it can return to shareholders over time. On this model, the company is valued using its latest twelve month free cash flow of about $311 million and a set of growing cash flow projections that gradually slow as the business matures.

Those cash flows translate into an estimated intrinsic value of about $278 per share, which sits above the current share price and points to the stock trading at roughly a 23.2% discount. Because SPX Technologies has been investing to serve rising data center cooling demand and expand capacity, the DCF essentially assumes that this growth supports higher, but eventually steadier, cash generation.

Because SPX Technologies has nearly doubled its revenue since 2021 with a stronger free cash flow margin, the market’s focus on near term growth helps explain why the share price still sits below the level implied by its discounted cash flows.

On balance, the DCF work suggests SPX Technologies stock currently appears undervalued relative to its projected cash flows.

Our Discounted Cash Flow (DCF) analysis suggests SPX Technologies is undervalued by 23.2%. Track this in your watchlist or portfolio, or discover 44 more high quality undervalued stocks.

Does SPX Technologies Look Pricey on Earnings?

The P/E ratio suits SPX Technologies because earnings quality is central to how investors value industrial and HVAC-focused businesses. SPX Technologies currently trades on a P/E of about 41.4x, which is well above the Machinery industry average of roughly 26.5x and also above the peer group average of about 27.0x. That places the stock at a clear premium to many similar companies.

The Fair Ratio model, which blends factors like SPX Technologies' growth profile, margins, size and risk characteristics, points to a P/E of around 33.7x as a more balanced level. Compared with the current 41.4x, the market is assigning a sizeable extra premium on top of what this framework suggests. Even allowing for the strong interest in SPX Technologies' HVAC and data center exposure, the earnings multiple screens as rich rather than modest.

On this P/E yardstick, SPX Technologies stock appears expensive relative to what the Fair Ratio model implies.

The SPX Technologies Narrative: What Would Justify Today's Price?

Simply Wall St Narratives for SPX Technologies pick up where the mixed DCF and P/E signals leave off by spelling out which combinations of growth, margins and earnings paths would make SPX Technologies' current price look high, fair or low. Each narrative ties its valuation number to a specific view on how growth, profitability and risk could evolve, giving you a reference point you can return to as fresh information comes through.

Share a narrative on SPX Technologies to put your own, number-driven view on the stock's data center cooling push and expanding production capacity on the record, then see how it compares as new results arrive.

By setting out your assumptions on SPX Technologies' growth, margins and cash generation, you can be one of the first voices in the Simply Wall St community to track how that thesis holds up against future company updates.

Do you think there's more to the story for SPX Technologies? Head over to our Community to see what others are saying!

The Bottom Line

For SPX Technologies, the Discounted Cash Flow (DCF) work points to meaningful upside to intrinsic value, while the earnings multiple signals that the stock already trades at a premium to peers. That split reflects a cash flow view grounded in existing projects and capacity on one side, and a market view that leans heavily on strong growth expectations and sentiment on the other. With the broader valuation checks sitting in mixed territory, the key question from here is whether SPX Technologies can deliver the growth and cash conversion the market is pricing in, without the P/E multiple needing to cool off.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.