St. Joe (JOE) Draws Fresh Valuation Focus, Is It Still A Bargain?

St. Joe Company JOE | 0.00 |

St. Joe (JOE) continues to attract attention as a real estate development and asset management company centered in Panama City Beach, Florida, with a US$3.8b market value and diversified residential, hospitality, and commercial operations.

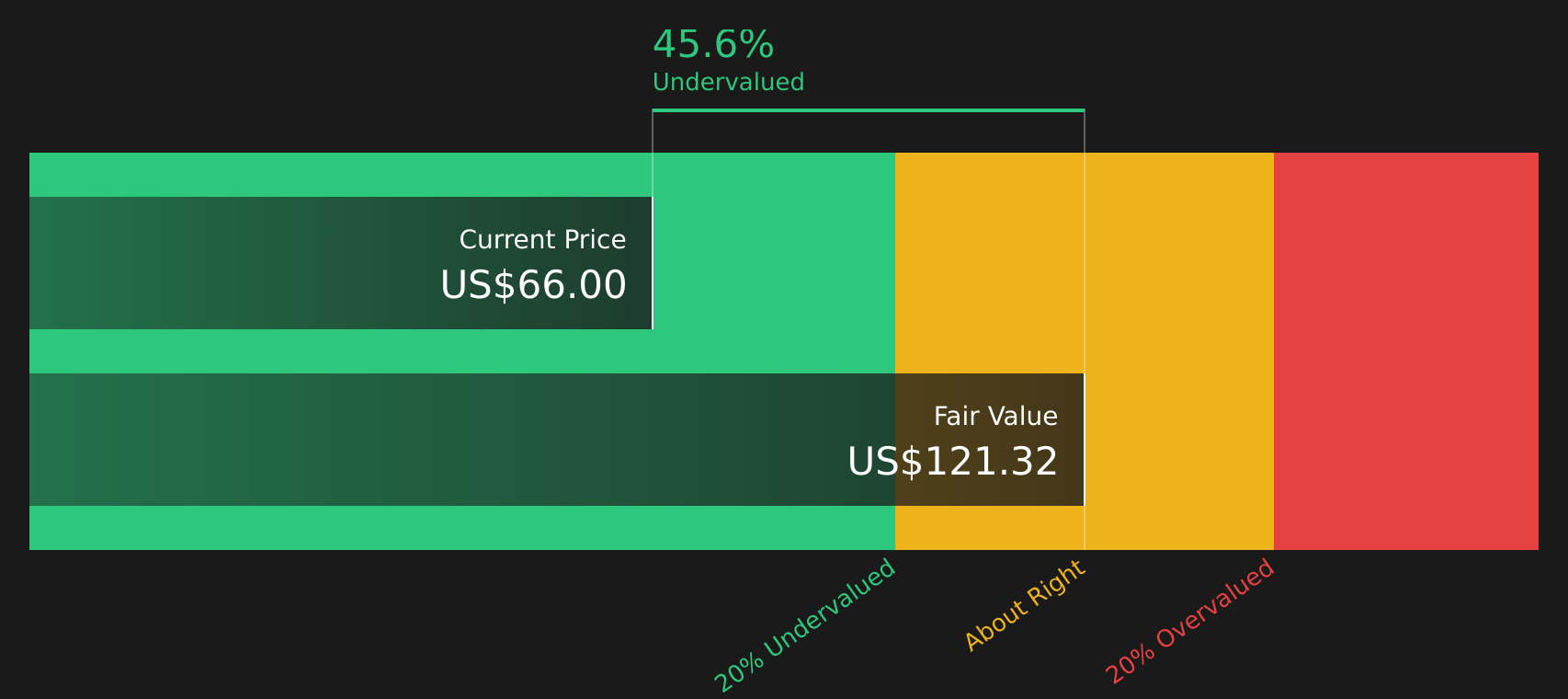

St. Joe’s share price has been firming, with a 30 day share price return of 3.33% and a 90 day share price return of 7.46%, while the 1 year total shareholder return of 35.76% points to stronger long term momentum at a last close of US$66.0.

If St. Joe’s performance has you thinking about what else might be gaining attention, this could be a useful moment to widen your search with 20 top founder-led companies

With St. Joe trading at US$66.0 and an estimated intrinsic discount of 45.82%, the key question is whether the stock still offers value or if the market is already pricing in significantly stronger future growth.

Price-to-Earnings of 33.8x: Is it justified?

St. Joe is trading on a P/E of 33.8x, while the stock is flagged as trading 45.8% below the SWS DCF fair value estimate of $121.82, which sends a mixed message on valuation.

The P/E ratio compares the current share price to the company’s earnings per share, so a higher P/E often reflects the market paying more for each dollar of profit.

For St. Joe, the 33.8x P/E sits well above the peer average of 13.3x and also above the US Real Estate industry average of 25.2x. This suggests investors are currently paying a premium for its earnings relative to both direct peers and the broader sector.

At the same time, the SWS DCF model, which projects future cash flows and discounts them back to today, points to a fair value of $121.82 versus the last close of $66.0. On a cash flow basis the stock screens as undervalued even though earnings are priced at a premium multiple.

Result: Price-to-Earnings of 33.8x (OVERVALUED)

However, St. Joe’s premium P/E and reliance on US real estate activity mean any cooling in buyer demand, or pressure on hospitality and commercial leasing, could challenge that valuation.

Another View on St. Joe’s Valuation

The earlier focus on St. Joe’s 33.8x P/E painted the stock as expensive relative to peers, but the SWS DCF model tells a different story. On that cash flow view, an estimated fair value of $121.82 versus a $66.0 share price suggests the stock screens as undervalued.

If earnings look pricey while projected cash flows suggest a gap to fair value, it raises a simple question for investors: which signal carries more weight for you?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out St. Joe for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 44 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

If the mixed valuation signals around St. Joe leave you uncertain, act while the data is fresh and weigh both sides for yourself by reviewing the 2 key rewards and 1 important warning sign

Looking for more St. Joe style investment ideas?

If St. Joe has sharpened your focus on finding quality opportunities, do not stop here, use the Simply Wall Street Screener to keep building a stronger watchlist.

- Target potential mispricings by scanning for quality stocks that trade below estimated worth through the 44 high quality undervalued stocks.

- Secure more dependable income ideas by focusing on companies built to support higher yields with the 8 dividend fortresses.

- Prioritize capital preservation and steadier profiles using the 71 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.