Standex International (SXI) Stock Could Be 8.4% Overvalued After Analyst Backing And Strong Results

Standex International Corporation SXI | 0.00 |

Standex International (SXI) is back on investors’ radar after a respected William Blair analyst reaffirmed a positive rating, alongside rising institutional ownership, bullish technical signals, and strong year-over-year revenue and profit growth.

The recent 6.56% 1 day share price return, on top of a 23.20% 30 day share price return and 40.16% year to date share price return, reflects strong momentum around Standex International as investors respond to the positive analyst stance, higher institutional ownership and the latest quarterly results. Together, these factors have been associated with a 99.42% 1 year total shareholder return.

If this kind of move has your attention, it could be a useful moment to broaden your watchlist and check out 20 top founder-led companies

With Standex International now trading above one analyst’s price target yet still showing an estimated intrinsic discount, the key question is whether the stock is already fully valued or if markets are still catching up to future growth potential.

Most Popular Narrative: 8.4% Overvalued

On the latest numbers, the most followed narrative pegs Standex International’s fair value at $290.8, below the $315.17 last close. This puts a spotlight on what is built into those future cash flow assumptions.

The analysts have a consensus price target of $290.8 for Standex International based on their expectations of its future earnings growth, profit margins and other risk factors.

However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $323.0, and the most bearish reporting a price target of just $260.0.

Want to understand why this valuation still leans above today’s price despite that analyst spread, slower forecast revenue growth and only moderate margin expansion doing the heavy lifting? The full narrative spells out how earnings, profitability and the chosen discount rate all combine to reach that $290.8 figure.

Result: Fair Value of $290.8 (OVERVALUED)

However, Standex International’s reliance on acquisitions for growth, along with its ongoing exposure to trade and tariff shifts, could quickly challenge the current overvaluation narrative.

Another View: Standex International Through A Cash Flow Lens

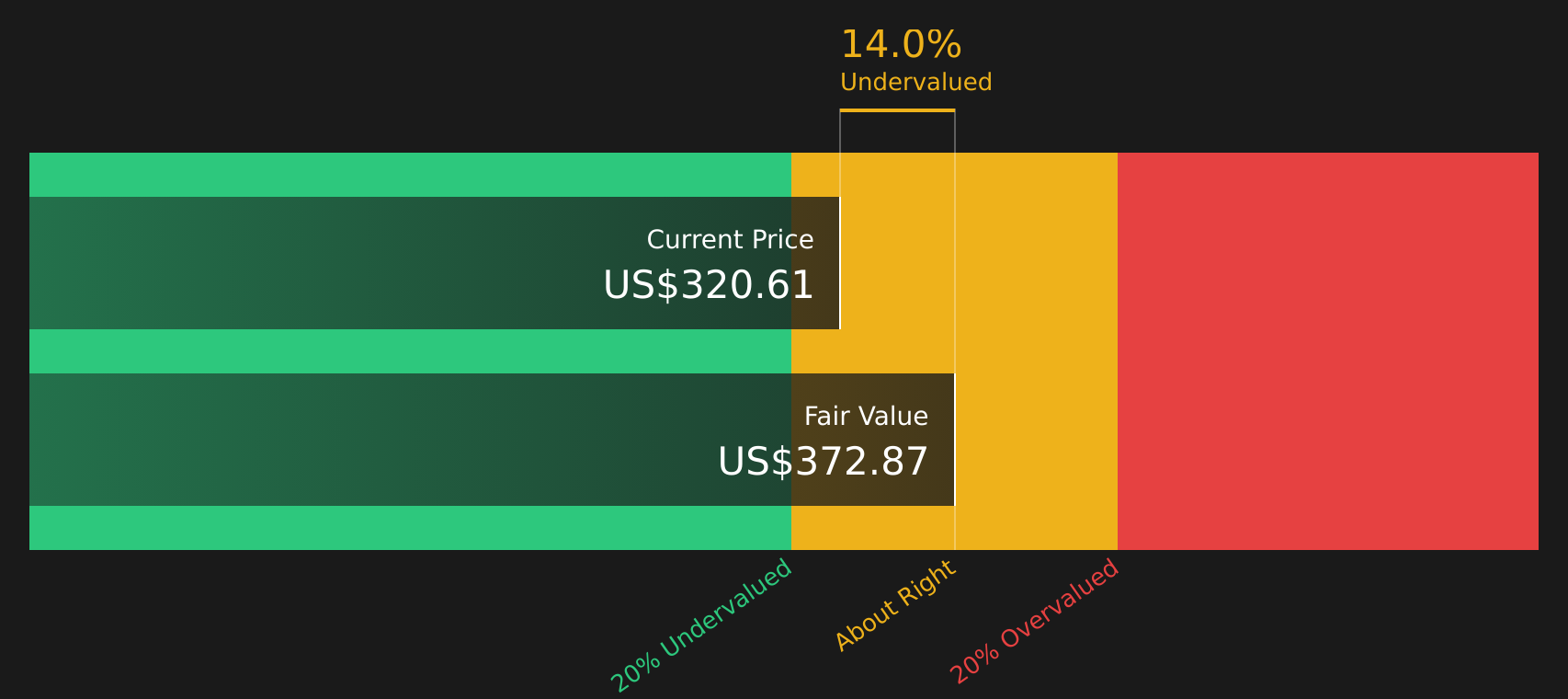

The analyst narrative calls Standex International about 8.4% overvalued at $290.8 per share, yet Simply Wall St’s DCF model points the other way, with an estimated future cash flow value of $372.87. If both use the same business, growth and risk data, which signal should carry more weight for you?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Standex International for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 45 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

Given the mix of optimism and caution around Standex International, this is a good time to review the underlying data yourself and decide how the risk reward trade off fits your goals, starting with the 3 key rewards and 2 important warning signs

Looking for more investment ideas beyond Standex International?

If Standex International has sharpened your focus, do not stop here. Use these focused stock ideas to pressure test your thinking and uncover opportunities you might be missing.

- Target stability first by scanning 66 resilient stocks with low risk scores that may better fit a cautious approach without giving up quality altogether.

- Hunt for value by reviewing 45 high quality undervalued stocks where solid fundamentals and pricing can line up more attractively than the headline names on your radar.

- Get ahead of the crowd by checking the screener containing 19 high quality undiscovered gems before they become widely followed and potential upside is already priced in.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.