Starbucks (SBUX) Valuation in Focus Following $1 Billion Turnaround Plan and Store Closures

Starbucks Corporation SBUX | 96.92 96.90 | -0.30% -0.02% Pre |

Starbucks (SBUX) just set off alarm bells across the investing world after revealing a sweeping $1 billion restructuring plan. The announcement includes shuttering roughly 1% of its company-operated stores across North America and cutting about 900 non-retail positions. These moves are central to CEO Brian Niccol’s larger turnaround vision, which aims to address consistent sales declines, simplify company operations, and reshape the in-store experience for customers. For investors weighing what to do with Starbucks stock right now, these changes mark the company’s most aggressive reset in years. This is far more than business as usual.

Zooming out, Starbucks has spent the past year battling through a period of reduced momentum. The stock’s value has slipped about 12% over the past twelve months, and its decline has persisted through the year. Yet, despite persistent challenges, Starbucks continues to generate annual revenue and net income growth, suggesting the underlying business hasn’t lost its fundamental strength. Still, with competitors expanding and consumer trends shifting, the pressure is on for Starbucks to prove that these management actions can restore the growth story investors have come to expect.

With the share price sliding but operational shifts underway, is Starbucks now trading at a discount, or are markets simply recalibrating for a slower-growth future? Could this reset be a long-term buying opportunity, or is the market getting it right?

Most Popular Narrative: 14.6% Undervalued

According to the most followed narrative, Starbucks stock is currently seen as undervalued, with a fair value estimate meaningfully above its recent price. This assessment relies on forward-looking growth and profitability assumptions.

“Using the $42 billion revenue as a starting point, a projected $57.5 billion revenue in 2030 will result in a $5.75 billion net income. Using a terminal P/E ratio of 27.5x, we can calculate that a terminal value in 2030 is $158.1 billion, discounted using the 8.2% rate equals $106.5 billion.”

Curious what is powering this bold price target? The key factors behind the valuation are a combination of aggressive expansion, resilient margins, and a forward profit multiple that could surprise even seasoned investors. Interested in how these projections compare to the consensus? The numbers behind this fair value might change how you view the future for Starbucks.

Result: Fair Value of $97.59 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.However, persistent labor disputes and surging coffee commodity prices could quickly undermine even the most optimistic case for Starbucks’s undervaluation.

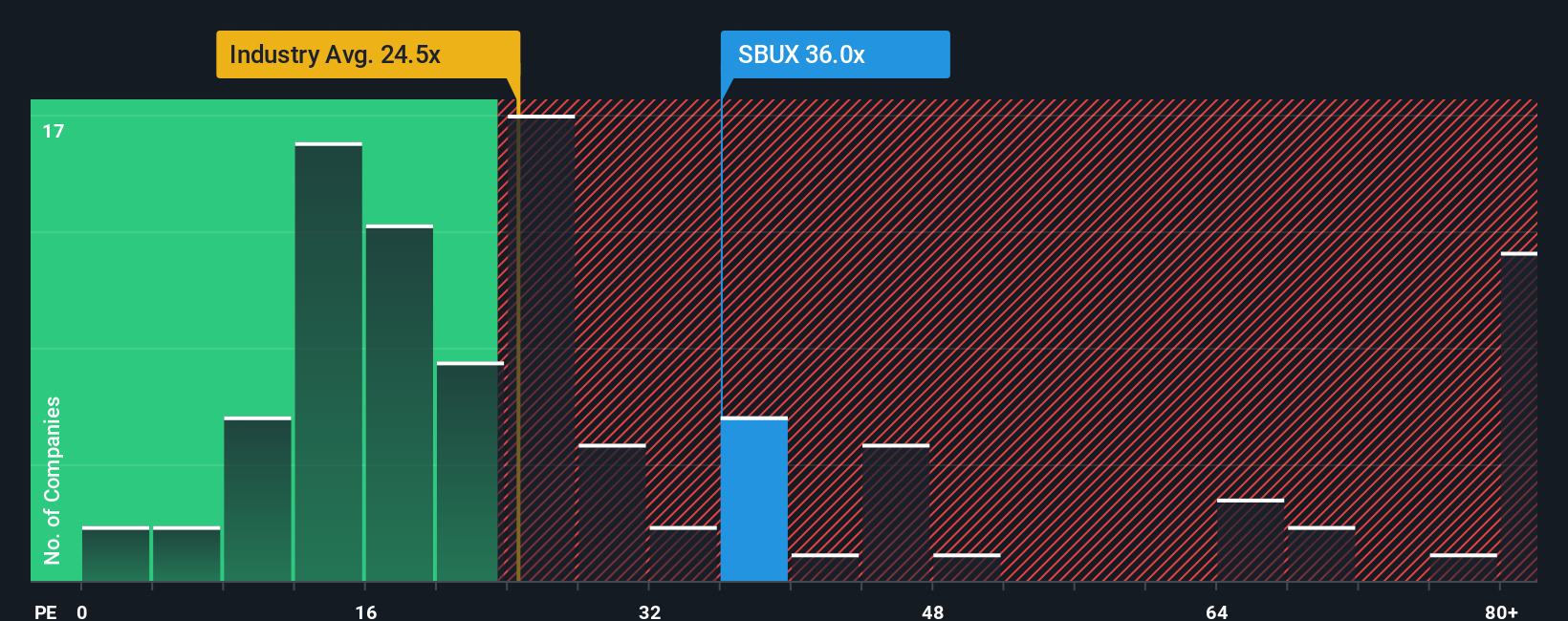

Find out about the key risks to this Starbucks narrative.Another View: Industry Comparison Paints a Different Picture

While the leading narrative sees Starbucks as undervalued, a look at its price-to-earnings ratio compared to the US hospitality industry suggests it might actually be expensive. Which approach will better predict Starbucks’s long-term value?

Build Your Own Starbucks Narrative

If you want a different take or have your own perspective on Starbucks, dive into the numbers and see what narrative you can build in just a few minutes. Do it your way

A great starting point for your Starbucks research is our analysis highlighting 1 key reward and 4 important warning signs that could impact your investment decision.

Looking for More Smart Investment Ideas?

Why settle for just one opportunity? There are stocks out there with the potential to energize your portfolio and keep you ahead of the curve. Seize the moment and check out these promising strategies, each offering a unique path to growth and value.

- Capture the momentum of companies creating the next AI breakthroughs by starting with AI penny stocks. See your tech investing strategy take its next step forward.

- Grow your wealth with confidence by screening for stocks offering consistent income with dividend stocks with yields > 3% and see which companies deliver robust yields above 3%.

- Uncover companies trading below their true value by using undervalued stocks based on cash flows, making undervalued opportunities your advantage before the rest of the market catches on.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.