STERIS (STE) Stock Looks Below Fair Value Following Its 15% Slide

STERIS plc STE | 0.00 |

Steris stock has declined 15.1% year to date, yet the current Discounted Cash Flow (DCF) intrinsic value estimate points to about 13.2% potential upside from the latest closing price of US$212.30, while the broader valuation checks paint a less generous picture.

- Steris is down 15.1% year to date, which puts more focus on whether the current price already reflects cautious expectations for the business.

- For a company built around recurring healthcare equipment and services, expectations for steady cash generation can support the DCF upside, while any pressure on margins or capital spending needs may limit how much value investors are willing to assign today.

- The stock only passes 2 of 6 value checks, which suggests Steris does not screen as a clear bargain when looking beyond the intrinsic value model to a broader set of valuation metrics.

The issue now is whether Steris’ current share price leaves enough margin of safety compared with its intrinsic value estimate, or whether the weak broader score is the more reliable guide.

Is STERIS a Bargain on Cash Flow?

The Discounted Cash Flow (DCF) model here uses projected free cash flows to estimate what STERIS might be worth today. In this approach, STERIS is treated as a business with relatively steady cash generation rather than one built on aggressive expansion assumptions.

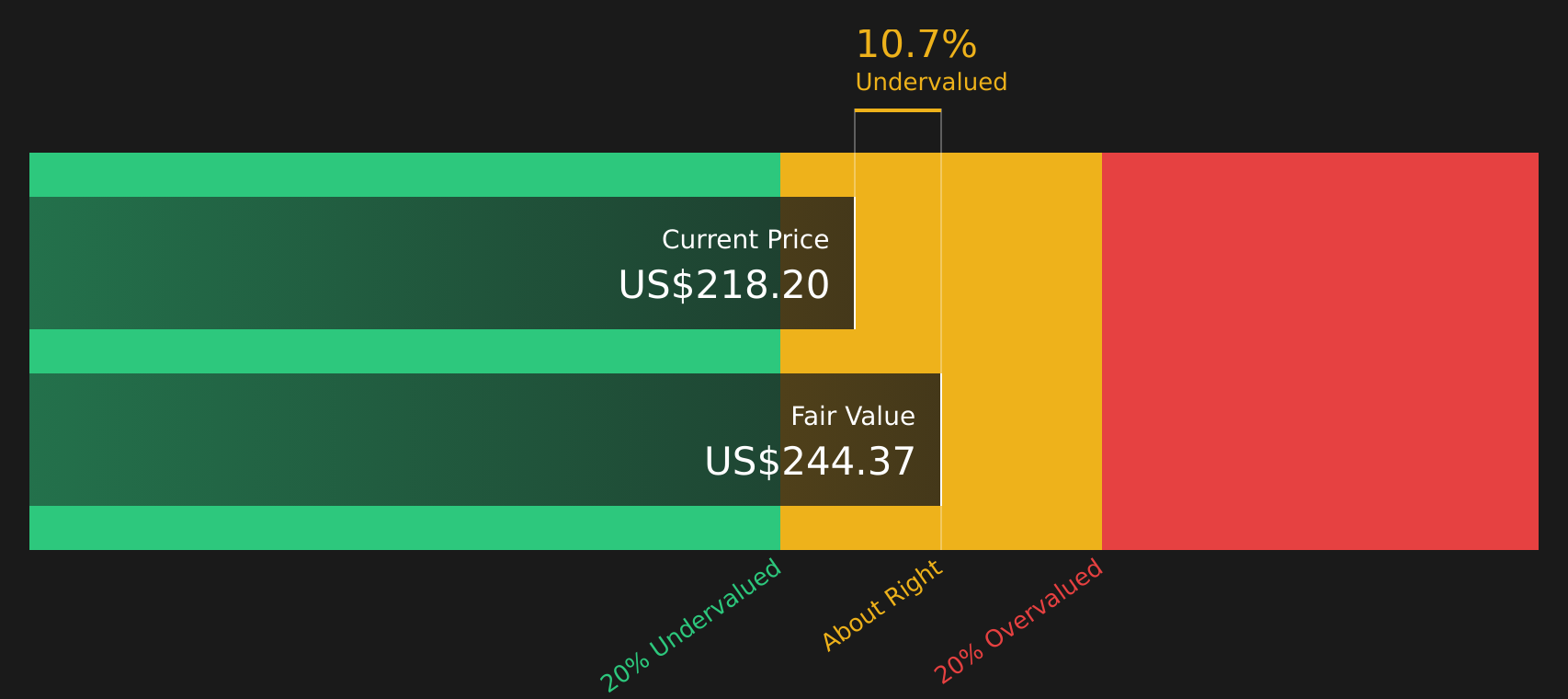

Over the latest twelve months, STERIS generated about US$946.7 million in free cash flow, and the model assumes these cash flows continue growing rather than shrinking over time. When those future cash flows are brought back to today, the intrinsic value comes out at about $245 per share, compared with the recent share price around $212. This gap implies roughly 13.2% potential undervaluation, although that conclusion still depends on the cash flow and discount rate assumptions holding up.

On this DCF view, STERIS stock currently screens as undervalued relative to its projected cash flows.

Our Discounted Cash Flow (DCF) analysis suggests STERIS is undervalued by 13.2%. Track this in your watchlist or portfolio, or discover 41 more high quality undervalued stocks.

Where Does STERIS Sit on Earnings?

P/E is a useful lens for STERIS because earnings are a core focus for many investors in established medical equipment businesses. STERIS currently trades on a P/E of about 26.4x, which is slightly above the Medical Equipment industry average of roughly 25.6x and above the broader peer group average of around 21.1x.

A tailored fair P/E ratio for STERIS, which reflects its sector, profitability profile, size and risk, is estimated at about 24.6x. That is modestly below the current multiple, so the stock does not stand out as either cheap or stretched on earnings alone. Instead, STERIS appears to be priced close to what this model suggests is reasonable for a profitable, established healthcare equipment company.

Overall, STERIS appears roughly fairly valued on its P/E multiple when set against both its tailored fair ratio and industry benchmarks.

The STERIS Narrative: What Would Justify Today's Price?

Simply Wall St Narratives for STERIS pick up where the valuation checks leave off by explaining which assumptions about STERIS' future growth, margins and earnings would need to hold for the stock to be worth significantly more or less than today's price. Each narrative ties a fair value estimate to a particular mix of potential catalysts and risks, allowing you to later compare how the actual business progress lines up with that story on the Community page.

If you have a numbers driven view on where STERIS' growth, margins and execution go from here, consider adding your own Narrative to the Simply Wall St community and set out the case you want to track. Sharing a clear thesis now gives you a reference point to revisit as new results and updates come through.

Do you think there's more to the story for STERIS? Head over to our Community to see what others are saying!

The Bottom Line

For STERIS, the Discounted Cash Flow (DCF) intrinsic value estimate points to some undervaluation, while the market-multiple view suggests the stock is priced roughly in line with peers. That split, combined with a weak overall value score, means the cash flow model looks more optimistic than the broader set of checks. The real question from here is whether STERIS can sustain the cash generation profile implied in the DCF without margin or capital spending pressure eroding that apparent discount.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.