Stocks to Watch | Buffett’s Sitting on $370B Cash: Are U.S. Stocks Too Expensive? Is Big Tech Finally in the "Strike Zone"?

Berkshire Hathaway Inc. Class A BRK.A | 704760.00 | -0.20% |

Dow Jones Industrial Average DJI | 49230.71 | -0.16% |

NASDAQ IXIC | 24836.60 | +1.63% |

Apple Inc. AAPL | 271.06 | -0.87% |

Microsoft Corporation MSFT | 424.62 | +2.13% |

Warren Buffett’s remarks in a recent interview have sparked intense debate on Wall Street this week.

Facing a recent pullback in U.S. equities, the legendary investor who has weathered countless bull and bear markets didn't mince words: "Stock market valuations remain unattractive. If the market plunges, Berkshire Hathaway Inc. Class A(BRK.A.US) will deploy cash."

Currently, Berkshire Hathaway is sitting on a massive pile of over $370 billion in cash and Treasury bills. Even as the Dow Jones Industrial Average(DJI.US) and the NASDAQ(IXIC.US) briefly slipped into technical correction territory, and his beloved Apple Inc.(AAPL.US) fell more than 14% from its peak, the Oracle of Omaha remains unfazed. He frankly admitted that Apple is "still not cheap enough." While he might back up the truck at a certain sweet spot in the future, it definitely won't be in today's market.

Buffett’s reluctance to deploy capital is causing anxiety among investors eager to buy the dip: Are U.S. stocks really too expensive? If I jump in now, am I catching a falling knife?

For investors focused on steady capital appreciation, maintaining a healthy respect for the market must be coupled with data-driven clarity. A deep dive into the current valuation structure reveals that the real "wealth effect" hasn't stalled out entirely—it has just undergone a deep, structural rotation.

1. The Macro View: Indices aren't dangerously high; they're approaching the "strike zone"

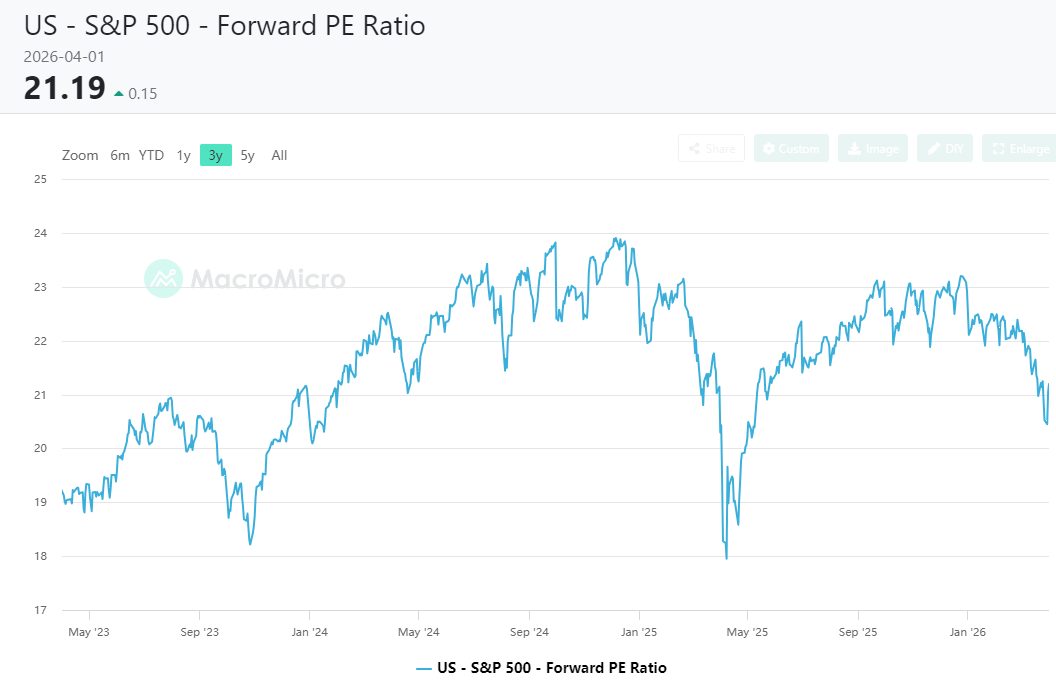

Buffett’s view that the broader market lacks appeal stems from his colossal capital base and stringent absolute-return requirements. But if we objectively examine the broader market data, U.S. stock valuations have actually retreated from "extreme exuberance" to a "relatively reasonable" range. Looking at the trailing three-year P/E trend of the broader market:

Following the recent pullback, the P/E ratio of the S&P 500 has returned to the level of last May. (Source: macromicro)

What does this mean? It indicates that the systemic risk of multiple compressions in the broader market has largely been released. For agile, smaller-scale retail investors, the market has entered a "strike zone" for scaling into positions, rather than a time for blind panic.

2. The Micro Breakdown: Valuation divergence and the "wealth effect" among Big Tech

If the broader market offers reasonable risk-reward, why does Buffett still think Apple is too expensive?

The answer lies in the divergence of earnings expectations among mega-caps. The real "wealth effect" always trails companies that can quickly digest high valuations with robust earnings growth.

Based on Yahoo Finance data, here are the current Forward P/E ratios for core tech stocks:

| Ticker | Forward P/E |

|---|---|

| Microsoft Corporation(MSFT.US) | 19.42 |

| Meta Platforms(META.US) | 19.42 |

| NVIDIA Corporation(NVDA.US) | 21.55 |

| Taiwan Semiconductor Manufacturing Co., Ltd. Sponsored ADR(TSM.US) | 24.88 |

| Amazon.com, Inc.(AMZN.US) | 25.91 |

| Alphabet Inc. Class A(GOOGL.US) | 25.97 |

| Broadcom Limited(AVGO.US) | 27.78 |

| Apple Inc.(AAPL.US) | 29.67 |

| Tesla Motors, Inc.(TSLA.US) | 181.82 |

Key Takeaways:

- Growth-bottlenecked giants remain expensive: Apple's Forward P/E is still hovering at 29.67. Without an explosive new growth curve, this valuation struggles to attract capital that prioritizes a strict margin of safety, like Buffett's. Meanwhile, Tesla Motors, Inc.(TSLA.US) sits at a lofty 181.82x Forward P/E.

- The top three cheapest: Microsoft Corporation(MSFT.US) and Meta Platforms(META.US), tie for the lowest valuation at 19.42x, boasting strong growth and cash flow. NVIDIA Corporation(NVDA.US) follows closely at 21.55x, offering solid value backed by massive AI expectations.

- The Semiconductor space (NVIDIA Corporation(NVDA.US) / Taiwan Semiconductor Manufacturing Co., Ltd. Sponsored ADR(TSM.US) / Broadcom Limited(AVGO.US)): Valuations are clustered in the 21-28x range, showing relative balance, with Taiwan Semiconductor Manufacturing Co., Ltd. Sponsored ADR(TSM.US) looking slightly more attractive than Broadcom.

- Tesla remains a high-flyer: At 181x+, Tesla Motors, Inc.(TSLA.US) is priced almost entirely on future narratives like robotics and autonomous driving.

- The broader average: Excluding Tesla, the group's average Forward P/E is roughly 24.5x, a reasonable valuation that has come off its previous highs.

(Note: Forward P/E is based on analyst consensus for the next fiscal year's EPS and updates rapidly during earnings season. Today, April 2, before the bell, data matches yesterday's close.)

High market cap does not equal high valuation. Wall Street's capital is becoming highly concentrated in AI infrastructure and commercialization leaders that offer ironclad earnings certainty and deeply discounted forward valuations.

3. Investment Strategy: How to replicate Buffett’s"winning with stability" playbook

For retail investors, Buffett’s sideline stance isn't a signal to liquidate portfolios. Rather, it’s a masterclass in extreme asset allocation and risk management during volatile times. In today's choppy market, investors should consider the following strategies:

- Build a "cash fortress" to maintain strategic agility: Never go all-in. Mimic Berkshire by holding ample cash or cash equivalents (like short-term U.S. Treasurys or money market funds). This isn't just a shield against extreme tail risks; it’s the ammunition you need to scoop up bargains with confidence when a massive sell-off occurs.

- Ditch blind buying; target "low forward P/E" giants: In this sideways market, Beta (broad market) returns are shrinking, while Alpha (stock picking) returns are shining. Focus your firepower on unfairly punished assets with strong cash flow and earnings certainty—like NVIDIA Corporation(NVDA.US)—trading at forward P/Es between 15x and 20x.

- Execute a "pyramid" dollar-cost averaging strategy: Don't try to call the absolute bottom; watch valuation percentiles instead. With indices approaching their median lines, it's reasonable to establish a starter position. If macroeconomic shocks push indices down further to the 20th percentile or historical bottoms, gradually scale up your buying.

Bottom Line

Buffett may be waiting for a macro-level storm, but investors can still pick up mispriced pearls on the beach before the clouds break. Identifying reasonable support levels for the broader market, locking into valuation pockets within Big Tech, staying patient, and scaling in gradually—this is the highest-probability playbook for navigating today's market.