Stocks To Watch | Stop Blindly Buying Big Tech: Discover 2026’s Top Stock Picks from the Magnificent Seven

NVIDIA Corporation NVDA | 177.39 | +0.93% |

Advanced Micro Devices, Inc. AMD | 217.50 | +3.47% |

Oracle Corporation ORCL | 146.38 | +0.79% |

Microsoft Corporation MSFT | 373.46 | +1.11% |

Apple Inc. AAPL | 255.92 | +0.11% |

Many Wall Street professionals believe that as tech giants’ earnings growth slows and doubts grow over enormous AI investments, the divergence within the so-called Magnificent Seven will continue into 2026.

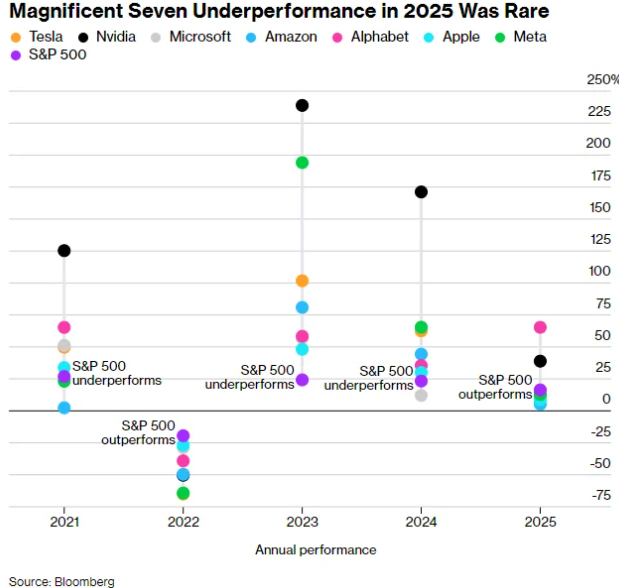

In the past, simply investing in major US tech stocks was a winning strategy. That changed in 2025, when most of these market leaders began underperforming the S&P 500 index(SPX.US) for the first time since the Fed’s rate hike cycle started in 2022. Even though the Magnificent Seven index outpaced the S&P 500 in 2025, the gains relied almost entirely on Google and Nvidia.

As capital begins flowing into other sectors, picking the right stocks within the tech group has become more critical. “The market can no longer be beaten with a single strategy,” says Jack Janasiewicz, Chief Portfolio Strategist at Natixis. “Losses in certain names may easily offset gains in others.”

At the same time, there’s still interest in these stocks since valuations have retreated from their highs. However, the future outperformance of the Magnificent Seven now depends less on broad sector trends and more on careful stock selection.

Magnificent Seven 2026 Outlooks:

The dominant AI chipmaker faces mounting competition and concerns about the sustainability of spending from key clients. After soaring about 1,100% since late 2022, Nvidia shares have pulled back 8% from their October 2024 peak. Rivals such as Advanced Micro Devices, Inc.(AMD.US) have won AI chip contracts from OpenAI and Oracle Corporation(ORCL.US), and Nvidia’s largest customers—like Google—are ramping up development of in-house custom chips.

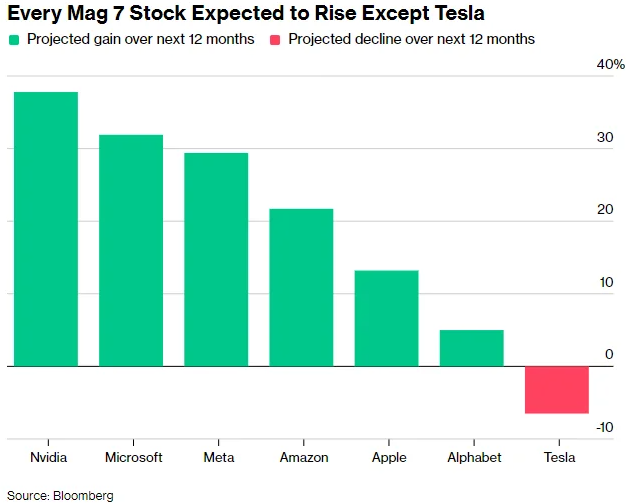

Nevertheless, Nvidia’s revenues continue to rise rapidly thanks to unrelenting demand for AI hardware. Wall Street remains bullish: Out of 82 covering analysts, 76 rate Nvidia a “Buy.” Consensus target prices suggest 39% upside over the next 12 months—the highest among the Magnificent Seven.

Microsoft Corporation(MSFT.US)

2025 marked Microsoft’s second straight year of underperforming the S&P 500. The company is among the heaviest AI spenders, with capex expected to reach $100 billion in fiscal 2026 (ending June). Analysts think capex could climb even higher to $116 billion for the following year.

While data center expansion is reviving Azure cloud growth, Microsoft has yet to convince customers to pay a premium for AI-embedded software. “Some investors are now seeking companies with stronger cash flow management and clearer profitability from AI,” says Brian Mulberry, a portfolio manager at Zacks Investment Management.

Apple has been the most conservative among the Seven about AI investment. This cautious stance weighed on its stock price in early 2025, with shares plunging nearly 20% by early August.

But Apple later rebounded as investors saw it as a ‘non-AI risk’ play, appreciating its avoidance of costly AI gambles. The stock soared 34% by year-end 2025. Robust iPhone sales provide reassurance that Apple’s core products remain in high demand.

For 2026, accelerating earnings growth will be key to further gains. Despite narrowly averting its longest losing streak since 1991, Apple’s recent share rally has slowed. Still, revenue is projected to rise 9% in fiscal 2026 (ending September), the fastest since 2021. Apple now trades at 31x forward earnings—second only to Tesla among the Seven—so continued financial outperformance will be necessary to justify the valuation.

Alphabet Inc. Class A(GOOGL.US)

Once feared to lag behind OpenAI, Google is now seen as an AI frontrunner across the industry. Its Gemini AI model has won widespread praise, easing concerns that OpenAI would dominate. Google’s in-house TPU chips are also a future revenue engine, with potential to take share from Nvidia in AI semiconductors.

Shares climbed over 65% in 2025—the best among the Seven—but future gains may be limited. With a market cap near $4 trillion and a forward P/E of 28 (well above its five-year average of 20), the stock’s 2026 upside is just 3.9% according to analyst estimates.

In 2025, Amazon was the weakest performer among the Seven for the seventh year in a row. Yet, early 2026 has seen a strong rebound, with Amazon leading its peers. The driver: growth at Amazon Web Services (AWS), which saw its fastest revenue increase in years.

Concerns that AWS was ceding ground to rivals, alongside heavy AI/automation spending, have held back the stock. Investors now expect Amazon’s supply chain automation and AI initiatives to pay off, potentially making 2026 a ‘comeback year.’

“Warehouse automation and more efficient distribution may be Amazon’s next big catalysts,” says Clayton Allison, portfolio manager at Prime Capital Financial. “This feels like last year’s Google, which the market doubted—until it soared.”

Meta’s AI pivot has mirrored broader investor skepticism toward outsized AI spending. CEO Mark Zuckerberg bet big on AI, acquiring companies, hiring top talent, and investing $14 billion in AI firm Scale AI (including its CEO, Alexandr Wang, now Meta’s AI chief).

While investors initially cheered, sentiment reversed after Meta raised its 2025 capex forecast to $72 billion and predicted a “substantial increase” for 2026—causing shares to tumble. Meta reached a record high in August 2025 after a 35% rally, but has since dropped 17%. For 2026, Meta’s challenge is clear: prove that enormous AI investments can drive real profit growth.

Tesla’s stock was the worst Magnificent Seven performer in the first half of 2025, only to surge over 40% in the second half as CEO Elon Musk shifted focus from sluggish EV sales to autonomous vehicles and robotics. As a result, Tesla’s forward P/E spiked to 200—second only to acquisition target Warner Bros Discovery (WBD.US) in the S&P 500.

After two years of flat revenue, Tesla is expected to return to growth, with sales projected to shrink 3% in 2025 but rebound by 12% in 2026 and 18% in 2027. Still, Wall Street is generally bearish: analysts on average forecast a 9.1% price decline over the next 12 months.