StoneCo (STNE) Is Down 10.8% After Q1 2026 Earnings And One-Time Dividend - Has The Bull Case Changed?

StoneCo Ltd. STNE | 0.00 |

- StoneCo Ltd. has already reported its first-quarter 2026 results, with revenue of BRL 3,578.02 million and net income of BRL 1,706.53 million, and declared an extraordinary one-time cash dividend of US$2.53 per share funded by proceeds from the Linx sale.

- Behind the headline jump in earnings, largely boosted by a sizable deferred tax benefit, StoneCo also flagged rising credit risk and higher loan-loss provisions that could pressure margins.

- Next, we’ll examine how this mix of stronger reported profitability and rising credit risk could influence StoneCo’s existing investment narrative.

Invest in the nuclear renaissance through our list of 88 elite nuclear energy infrastructure plays powering the global AI revolution.

StoneCo Investment Narrative Recap

To stay invested in StoneCo, you need to believe that Brazil’s shift to digital payments and financial services will keep expanding StoneCo’s merchant base and fee income, despite bumps in credit. The latest quarter supports that narrative on the surface, with higher revenue and a large deferred tax benefit lifting net income, but the sharp rise in credit risk and loan-loss provisions now looks like the key short term swing factor for earnings, while competition in payments remains the biggest ongoing risk.

The extraordinary one time US$2.53 per share dividend, funded from the Linx sale, is the announcement that most directly frames this earnings release. It shows how StoneCo is recycling capital from divested software assets back to shareholders even as it leans harder into credit and financial services. That mix can reinforce the existing catalyst of capital returns, but it also concentrates the business more squarely on payments and lending at a time when asset quality is under pressure.

Yet, while the headline results look strong, investors should be aware that rising non performing loans and a higher cost of risk could...

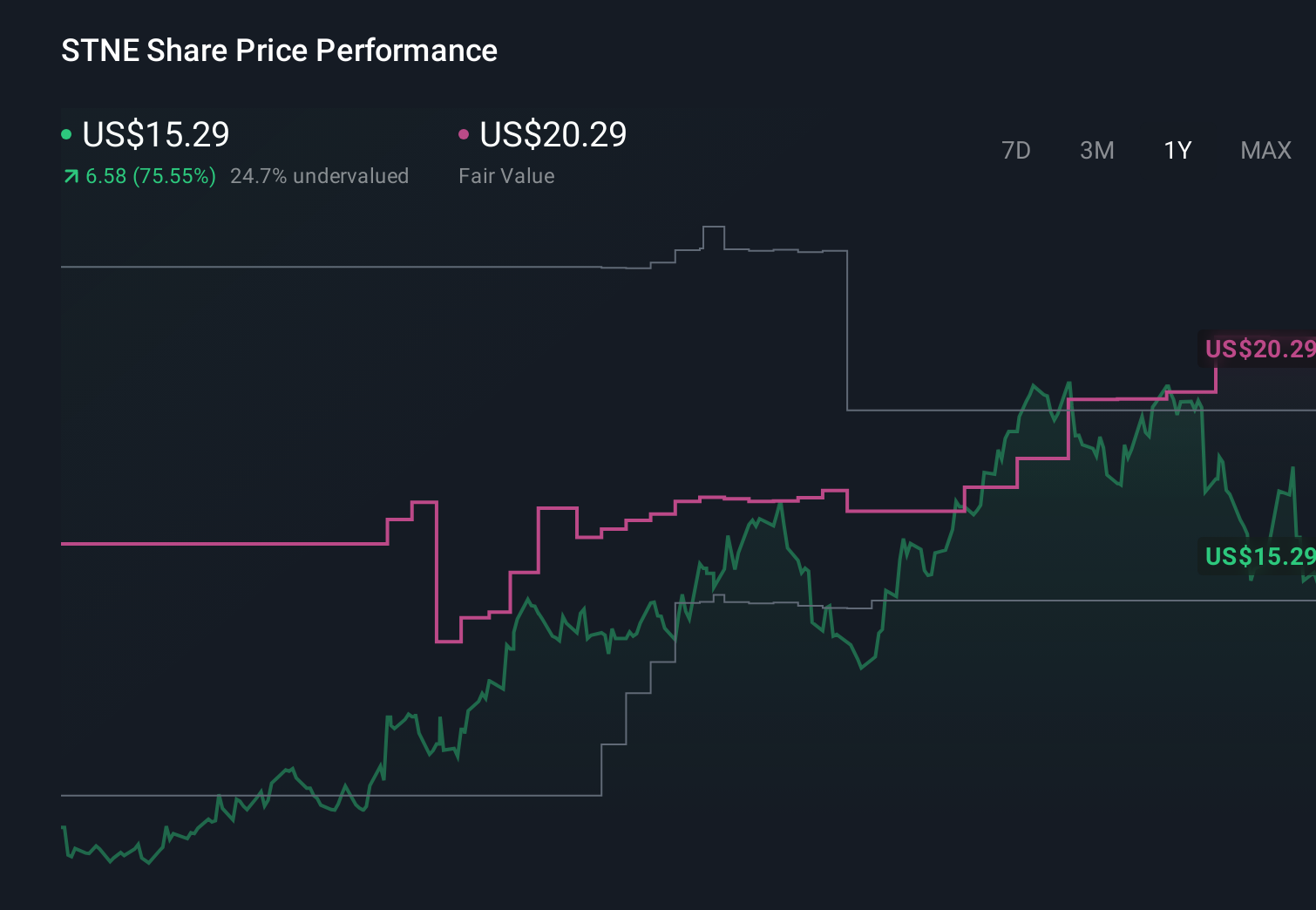

StoneCo's narrative projects R$17.4 billion revenue and R$5.0 billion earnings by 2028. This requires 8.2% yearly revenue growth and an earnings increase of about R$6.3 billion from R$-1.3 billion today.

Uncover how StoneCo's forecasts yield a $20.29 fair value, a 111% upside to its current price.

Exploring Other Perspectives

Before this quarter, the most cautious analysts were already assuming revenue growth of only about 3 percent and earnings drifting to roughly R$2.1 billion by 2029, so this spike in credit losses and provisions could either validate their concerns about rising compliance and credit burdens, or force a rethink if StoneCo stabilizes asset quality more quickly than they expected.

Explore 8 other fair value estimates on StoneCo - why the stock might be worth over 6x more than the current price!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your StoneCo research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free StoneCo research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate StoneCo's overall financial health at a glance.

Ready For A Different Approach?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- Uncover the next big thing with 27 elite penny stocks that balance risk and reward.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 30 best rare earth metal stocks of the very few that mine this essential strategic resource.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 16 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.