Stronger HVAC Bookings And Raised 2026 Outlook Might Change The Case For Investing In Trane (TT)

TRANE TECHNOLOGIES PLC TT | 0.00 |

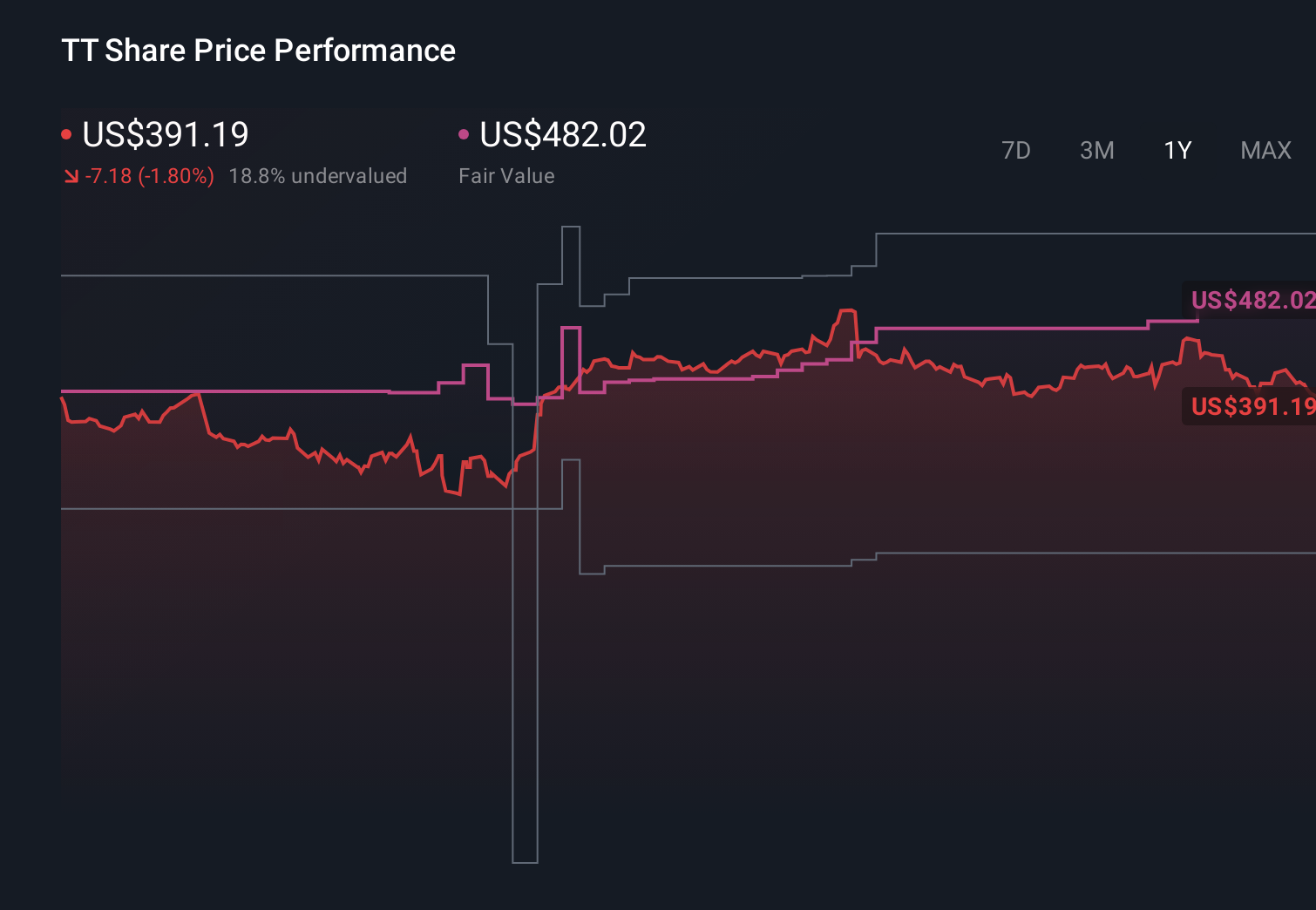

- In late April 2026, Trane Technologies reported first-quarter 2026 results showing higher sales of US$4,969.4 million but slightly lower earnings per share year-on-year, while also raising its full-year 2026 guidance to approximately 9.5% reported revenue growth and GAAP and adjusted EPS of US$14.75 to US$14.95.

- The company highlighted strong momentum in its Americas Commercial HVAC and global services businesses, supported by record bookings, a robust backlog, and meaningful contributions from the Stellar Energy acquisition, underscoring the importance of data center and modular cooling demand in its growth profile.

- With guidance raised and commercial HVAC strength underscored, we’ll now examine how this updated outlook could influence Trane Technologies’ investment narrative.

Find 49 companies with promising cash flow potential yet trading below their fair value.

Trane Technologies Investment Narrative Recap

To own Trane Technologies, you need to believe in the durability of its Americas Commercial HVAC engine, particularly data center and services demand, and its ability to convert record bookings into sustained earnings. The key near term catalyst is execution on that commercial backlog and services growth; the main risk is a downturn in data center and other key verticals that softens bookings. The latest guidance raise supports the positive near term story rather than changing it in a material way.

The most relevant update here is Trane’s decision on 30 April 2026 to lift full year 2026 guidance to about 9.5% reported revenue growth and GAAP and adjusted EPS of US$14.75 to US$14.95. That outlook sits alongside management’s emphasis on record commercial HVAC bookings and a strong services run rate, reinforcing the idea that backlog conversion and services expansion remain central to the near term catalyst for the stock.

Yet against this strength, investors should still be aware of how exposed Trane is if data center and other high growth commercial HVAC demand were to...

Trane Technologies' narrative projects $28.3 billion revenue and $4.5 billion earnings by 2029. This requires 9.4% yearly revenue growth and about a $1.6 billion earnings increase from $2.9 billion today.

Uncover how Trane Technologies' forecasts yield a $517.69 fair value, a 9% upside to its current price.

Exploring Other Perspectives

Some of the lowest estimate analysts were already cautious, assuming revenue of about US$26.0 billion and earnings near US$3.9 billion by 2029, so you should weigh whether the stronger Q1 and higher 2026 guidance ease those worries about over reliance on North American commercial HVAC or simply delay them.

Explore 4 other fair value estimates on Trane Technologies - why the stock might be worth as much as 9% more than the current price!

Decide For Yourself

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Trane Technologies research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Trane Technologies research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Trane Technologies' overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- Invest in the nuclear renaissance through our list of 91 elite nuclear energy infrastructure plays powering the global AI revolution.

- We've uncovered the 12 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Uncover the next big thing with 25 elite penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.