Stronger Quarter and EPS Upgrade Could Be A Game Changer For Laureate Education (LAUR)

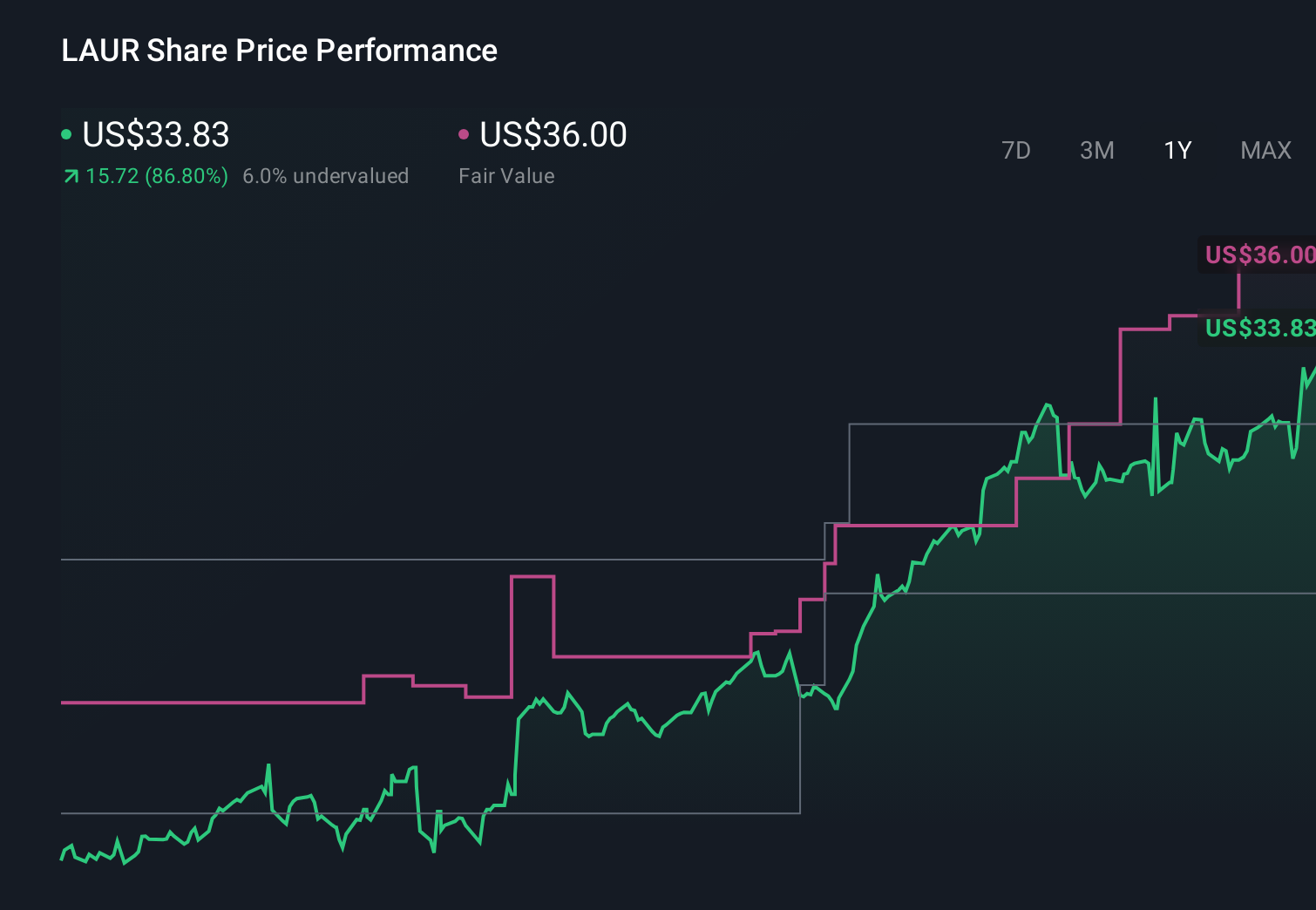

Laureate Education, Inc. LAUR | 0.00 |

- Earlier this year, Laureate Education reported quarterly revenue growth of 15.4% year on year, beating analyst expectations, lifting full-year adjusted EPS guidance, and completing about US$105 million of share repurchases supported by strong enrollments in Peru and Mexico.

- Institutional investors have increased their overall ownership and Laureate currently ranks highly on industry risk metrics, underscoring growing professional interest in the company’s risk-return profile.

- We’ll now assess how Laureate’s stronger-than-expected quarter and higher full-year earnings guidance affect the existing investment narrative.

Rare earth metals are the new gold rush. Find out which 30 stocks are leading the charge.

Laureate Education Investment Narrative Recap

To own Laureate, you need to believe its focus on higher education in Mexico and Peru, including digital programs, can keep enrollments healthy enough to support ongoing revenue and earnings growth despite concentrated country risk and rising competition. The latest quarter’s revenue beat and higher full-year earnings guidance reinforce enrollment momentum as a key short term catalyst, while the biggest near term risk remains that demand in these core markets could soften after recent campus and capacity investments.

Among the recent developments, the most relevant here is Laureate’s stepped up share repurchase activity, with about US$105 million bought back in the first quarter. Combined with higher earnings guidance, this capital return policy amplifies the impact of any future growth surprises, but it can also increase sensitivity if enrollment trends or regulatory conditions in Mexico or Peru do not evolve as optimistically as current expectations imply.

Yet behind the strong quarter, investors should still be aware of how concentrated exposure to Mexico and Peru could quickly become a problem if...

Laureate Education's narrative projects $2.3 billion revenue and $373.6 million earnings by 2029. This requires 9.1% yearly revenue growth and about a $93.8 million earnings increase from $279.8 million today.

Uncover how Laureate Education's forecasts yield a $40.25 fair value, a 10% upside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts take a much more cautious view, even before this news, assuming around US$2.2 billion of revenue and US$369 million of earnings by 2029, and warning that demographic shifts and digital disruption could still restrain Laureate’s growth, so it is worth comparing these assumptions to your own expectations.

Explore 3 other fair value estimates on Laureate Education - why the stock might be worth just $36.50!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Laureate Education research is our analysis highlighting 2 key rewards that could impact your investment decision.

- Our free Laureate Education research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Laureate Education's overall financial health at a glance.

Ready For A Different Approach?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

- Explore 31 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- Capitalize on the AI infrastructure supercycle with our selection of the 49 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.