Stronger Sales, Higher Dividend and Buybacks Might Change The Case For Investing In Advanced Drainage Systems (WMS)

Advanced Drainage WMS | 0.00 |

- Earlier this week, Advanced Drainage Systems reported past quarterly and full-year results showing higher sales but lower net income, completed a multi-year US$1.04 billion share repurchase program, and raised its annual cash dividend to US$0.80 per share, with a quarterly payment of US$0.20 scheduled for June 15, 2026.

- The combination of stronger top-line performance, the NDS acquisition’s contribution, and increased cash returns to shareholders highlights management’s focus on balancing growth investments with capital returns amid inflation-driven margin pressure.

- We’ll now examine how the stronger revenues but compressed margins, alongside the higher dividend, could reshape Advanced Drainage Systems’ investment narrative.

Uncover the next big thing with 25 elite penny stocks that balance risk and reward.

Advanced Drainage Systems Investment Narrative Recap

To own Advanced Drainage Systems, you need to believe in long term demand for modern stormwater and wastewater infrastructure, even if construction markets stay choppy. The latest results reinforce that tension: stronger sales and the NDS acquisition support the growth story, while lower net income and inflation driven margin pressure keep profitability as the key near term swing factor. The completed US$1.04 billion buyback and higher dividend do not materially change that core risk around earnings sensitivity to costs.

The 11% increase in the annual dividend to US$0.80 per share is the clearest new signal for shareholders right now, sitting alongside the recent revenue growth but compressed margins. It ties into the main catalyst many investors are watching: whether higher margin Allied and treatment solutions, including the NDS portfolio, can gradually improve earnings quality without overstretching the balance sheet or relying too heavily on acquisition driven growth.

Yet investors should be aware that if resin and other input costs stay elevated, the pressure on margins and earnings could...

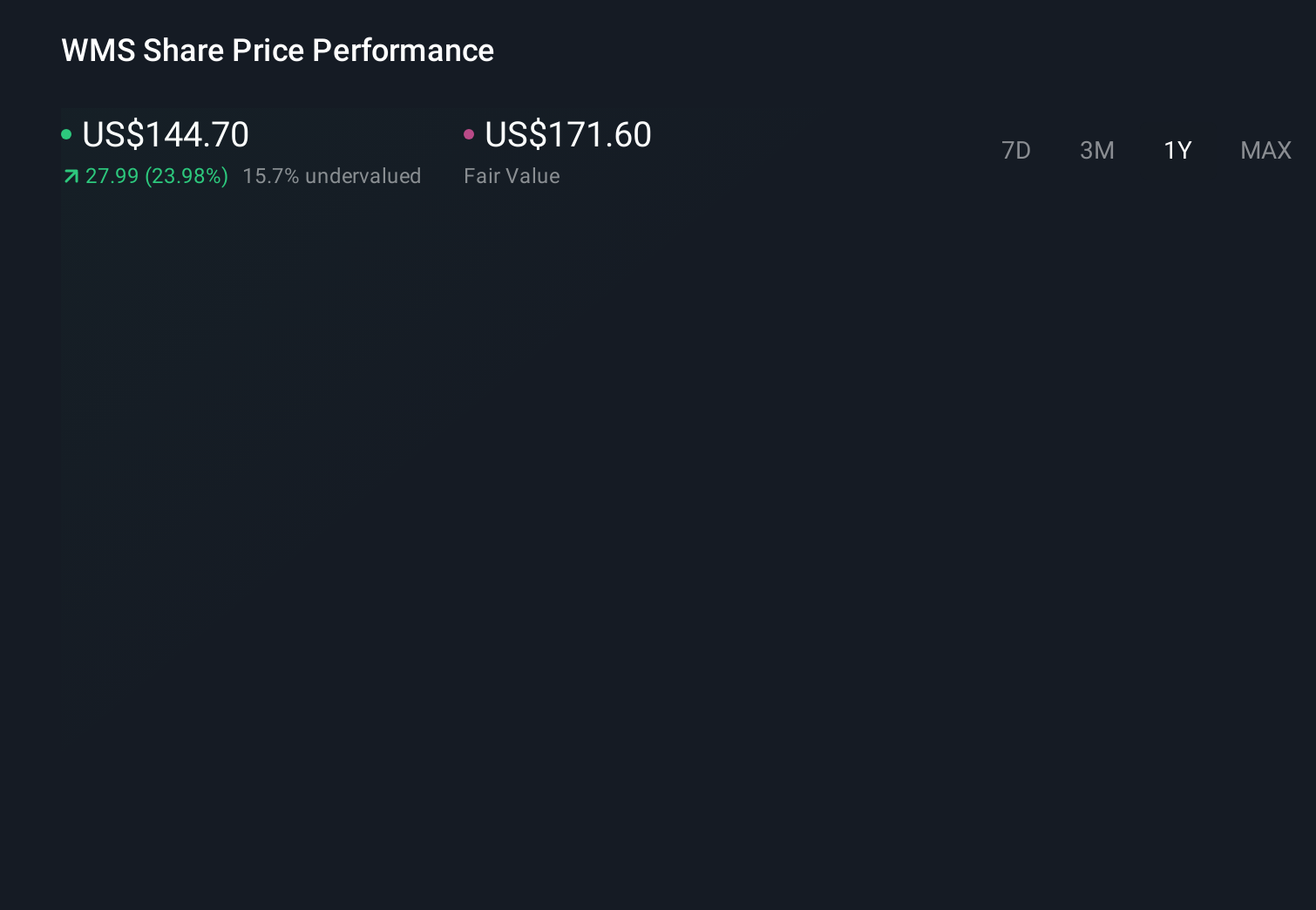

Advanced Drainage Systems' narrative projects $4.0 billion revenue and $674.0 million earnings by 2029. This requires 9.5% yearly revenue growth and about a $246 million earnings increase from $427.6 million today.

Uncover how Advanced Drainage Systems' forecasts yield a $185.75 fair value, a 40% upside to its current price.

Exploring Other Perspectives

Two Simply Wall St Community fair value estimates cluster between US$170.44 and US$185.75, showing how differently individual investors can view Advanced Drainage Systems. Against that backdrop, the recent margin compression tied to higher material and transport costs becomes a key factor that could influence how these various expectations for the company’s performance evolve, so it is worth weighing several viewpoints before deciding what the stock is worth.

Explore 2 other fair value estimates on Advanced Drainage Systems - why the stock might be worth as much as 40% more than the current price!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Advanced Drainage Systems research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Advanced Drainage Systems research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Advanced Drainage Systems' overall financial health at a glance.

Searching For A Fresh Perspective?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- The latest GPUs need a type of rare earth metal called Dysprosium and there are only 27 companies in the world exploring or producing it. Find the list for free.

- AI is about to change healthcare. These 34 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- We've uncovered the 10 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.