Supply Chain Stocks Facing A Pricing Power Test

Liquidity Services, Inc. LQDT | 0.00 |

Supply chain disruptions are doing more than keeping shelves patchy; they are reshaping pricing power across logistics, shipping, ports, and storage. When goods are harder to replace, companies that move and manage them can sometimes set terms instead of just accepting them, while weaker operators risk being squeezed by higher costs and lost volumes. This article looks at three stocks from a Supply Chain Infrastructure and Logistics Companies screener that are closely tied to these pressures. Each stock is exposed to the same news catalyst, but in different ways, and the goal is to help you decide whether it belongs on your watchlist or not.

RB Global (RBA)

Overview: RB Global operates global marketplaces and digital platforms that help companies buy, sell, finance, and move commercial assets and vehicles, from construction equipment and trucks to autos and industrial machinery. Through brands like Ritchie Bros. and IAA, it connects sellers looking to turn idle assets into cash with buyers seeking pre owned equipment, while layering on data, appraisal, and lifecycle services.

Operations: RB Global generates about US$4.7b in revenue from Business Services, with its largest geographic exposure in the United States at roughly US$3.3b, followed by Canada, Europe, and Australia.

Market Cap: US$21.7b

Investors watching how supply chain strains are reshaping pricing power may find RB Global interesting because it sits at the crossroads of logistics, equipment turnover, and asset reuse. The company can be sensitive to environments where tight supply pushes more businesses toward pre owned equipment and structured marketplaces, and its earnings profile and longer term track record have attracted analyst attention. At the same time, a rich P/E multiple, reliance on external borrowing, and execution risks from ongoing acquisitions and international expansion mean expectations are high and missteps could be costly. The full story is how these forces interact with RB Global’s digital ecosystem and service mix in a world where equipment scarcity and logistics resilience matter more than ever.

RB Global’s rich P/E and expanding digital ecosystem suggest expectations are high, but the real question is whether the current set up justifies that confidence. Get the DCF valuation analysis for RB Global and see what the market might be missing.

Charter Hall Group (ASX:CHC)

Overview: Charter Hall Group is an Australian property investor and fund manager that raises capital from investors and deploys it into office, industrial and logistics, retail, and social infrastructure assets, earning fees for managing those funds and income from co investing in the properties alongside clients.

Operations: Charter Hall Group generates about A$433.7m from Funds Management, A$387.1m from Property Investments, and A$90.3m from Development Investments, with A$860.7m of revenue coming from Australia.

Market Cap: A$10.5b

Charter Hall Group is closely linked to how Australia houses its warehouses, offices and essential infrastructure, so persistent supply chain pressures and the need for more resilient logistics networks are directly relevant to its industrial and logistics portfolio. Record equity inflows, solid margins and a large, diversified funds management platform provide multiple ways it can grow fee income and rental revenue. Investors still need to weigh this against its exposure to office and retail assets, higher funding risk from reliance on external borrowing, and an earnings history that has not always been smooth. Overall, CHC combines quality assets with real risks, and may be more suitable for investors who understand where the key value drivers and pressure points sit.

Charter Hall Group’s fee engine and co investment income can look powerful, but the real story is how those cash flows stack up against its property exposure and funding needs. Review the Charter Hall Group financial health report for the context most investors are missing.

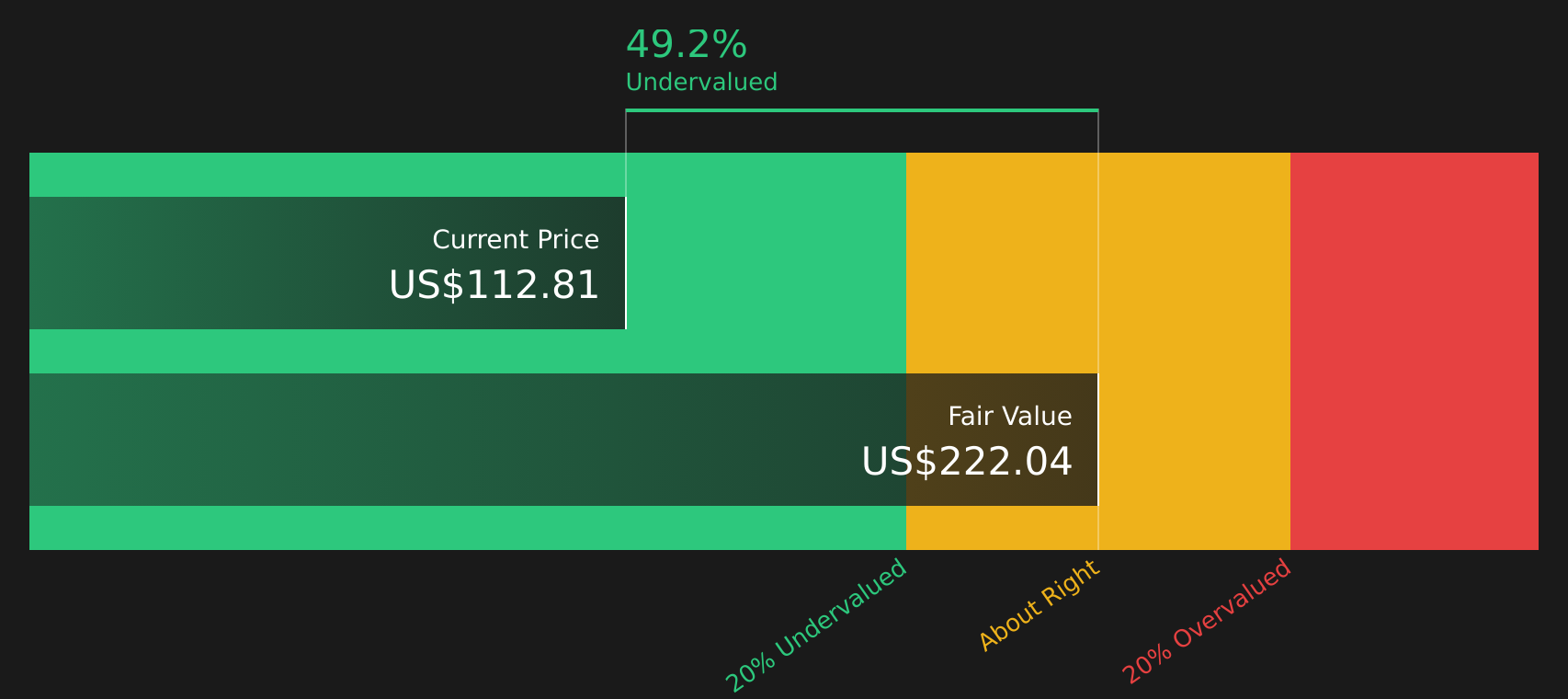

Liquidity Services (LQDT)

Overview: Liquidity Services runs online marketplaces and software that help governments and companies sell surplus, returned, and overstock assets, from consumer goods and apparel to heavy equipment and real estate, while also providing tools for valuation, marketing, and inventory management.

Operations: Liquidity Services generates about US$325.1m from its Retail Supply Chain Group, US$91.2m from GovDeals, US$42.1m from the Capital Assets Group, US$21.5m from Machinio & Software Solutions, and a small segment adjustment of US$0.1m, with around US$433.8m of revenue coming from the United States and US$46.1m from the rest of the world.

Market Cap: US$1.2b

Liquidity Services sits directly in the flow of surplus and hard to source goods. Persistent supply chain friction and product scarcity can push more buyers and sellers onto its marketplaces while also supporting the value of used assets. The company has been reporting strong earnings growth, high quality profits and a 13.6% ROE, yet still trades below one estimate of fair value. This may interest investors who think its role in inventory management and asset recovery has room to expand. On the risk side, a relatively rich P/E, reliance on external funding and recent insider selling are important to weigh. The question is whether Liquidity Services’ position in inflation conscious, supply constrained markets fully explains that gap or not.

Strong earnings, high quality profits and a 13.6% ROE suggest Liquidity Services’ story may still be underappreciated. Get the analyst forecasts for Liquidity Services and see what that growth profile might really be signaling.

The three stocks covered here are just a starting sample, and the full Supply Chain Infrastructure and Logistics Companies screener includes 7 more companies with equally compelling supply chain stories that could change how you think about this theme. Use Simply Wall St to identify and analyze the exact catalysts, business models, and risk profiles that matter to you so you can focus on the highest conviction supply chain infrastructure and logistics ideas.

Take Control of Your Investment Journey

If RB Global or any of these companies sound like a great opportunity, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value the ideal entry point. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Fresh Alternatives Before Others Do

Fresh stock ideas do not stay under the radar for long, and early momentum can be caught or missed in a hurry, so consider acting before the crowd and getting in early.

- Spot early-turn stories and target companies with strong foundations using this curated list of solid balance sheet and fundamentals (47 results) before valuations move away from ideal entry points.

- Focus on income opportunities by zeroing in on hand picked 8 dividend fortresses that could provide cash flow while prices are still moving into more attractive territory.

- Monitor potential AI infrastructure opportunities by scanning carefully selected 53 AI infrastructure stocks while they are still under the radar, and review them before any momentum develops.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.