Sysco Reaffirms 2025 Outlook While Refocusing On Higher Margin Markets

Sysco Corporation SYY | 71.16 | -0.66% |

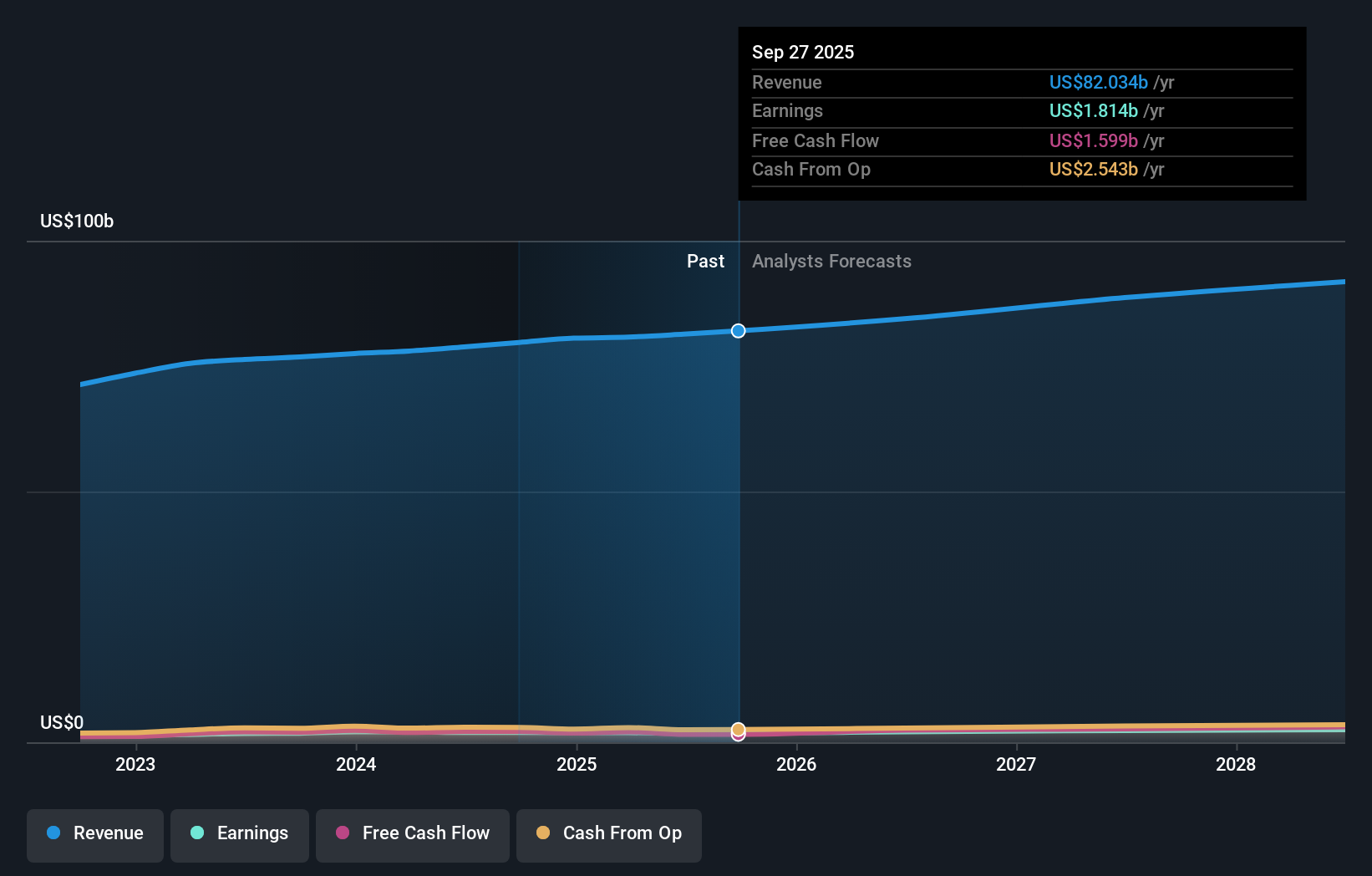

- Sysco (NYSE:SYY) reaffirmed its fiscal 2025 guidance, signaling confidence despite softer restaurant traffic.

- The company plans to divest its joint venture in Mexico to concentrate on higher growth, higher margin international markets.

- These moves reflect a refocus of capital and management attention on select global regions and product lines.

Sysco, trading at $75.63, is in the middle of the pack for recent performance, with the stock up 4.1% year to date and 20.3% over the past five years. For a large foodservice distributor, those returns highlight a relatively steady profile as the company adjusts its global footprint and maintains its outlook for fiscal 2025.

For investors, the reaffirmed guidance and the decision to exit the Mexico joint venture indicate a company tightening its portfolio and sharpening its focus on where it sees better margins internationally. How effectively Sysco executes on this refocus, and how the core North American foodservice business holds up against restaurant traffic headwinds, will likely be key areas to watch over the coming year.

Stay updated on the most important news stories for Sysco by adding it to your watchlist or portfolio. Alternatively, explore our Community to discover new perspectives on Sysco.

Reaffirming fiscal 2025 guidance while restaurant traffic is down 3.6% suggests Sysco is leaning on internal levers such as mix, pricing, and cost control to keep its targets intact. The move to exit the Mexico joint venture and concentrate on higher growth, higher margin international markets points to a tighter product and geographic focus, with execution in those remaining regions likely to matter more for future performance.

Sysco narrative check in a changing business mix

With no established public narrative here, this update still speaks to two themes many investors watch for in large distributors: disciplined capital allocation and consistent earnings delivery. Sysco’s confidence in its guidance, alongside reshaping its international footprint, may shape how you think about the balance between its mature North American base and selected overseas markets.

Risks and rewards investors should weigh

- 🎁 Reaffirmed targets for 4% to 5% net sales growth and 6% to 7% adjusted EPS growth show management is sticking to its plan despite softer traffic.

- 🎁 Solid performance in international operations, national sales, and SYGMA gives Sysco more than one engine to support results.

- ⚠️ Debt is not well covered by operating cash flow, so any setback in earnings or cash generation could matter more for the balance sheet.

- ⚠️ The Mexico JV divestiture may weigh on reported sales comparisons, which could make headline growth numbers harder to interpret in the near term.

What to watch next

From here, the key questions are whether Sysco can turn its international pivot and new sales incentives into steady local volume growth while keeping margins resilient as restaurant traffic softens. You can stay on top of how that story is evolving by following the latest views in the community narratives hub.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.