Take Two Stock Stands Out As Live Service Gaming Loses Its Grip

Electronic Arts Inc. EA | 0.00 |

The live service model that once helped power hits like Destiny 2 is now under pressure, and that shift is rippling through gaming stocks. As Bungie, owned by Sony, pulls back on Destiny 2 updates and the industry leans toward blockbuster single player titles, investors are reassessing where future cash flows might come from. This article explains how that news connects to three stocks exposed to the same forces, highlighting one where the changing model could be a relative positive and two where it may add earnings and sentiment risk.

Take-Two Interactive Software (TTWO)

Overview: Take-Two Interactive Software is a global video game publisher behind blockbuster franchises like Grand Theft Auto, Red Dead Redemption, NBA 2K and a large Zynga mobile portfolio across consoles, PC and smartphones, sold through both physical and digital channels.

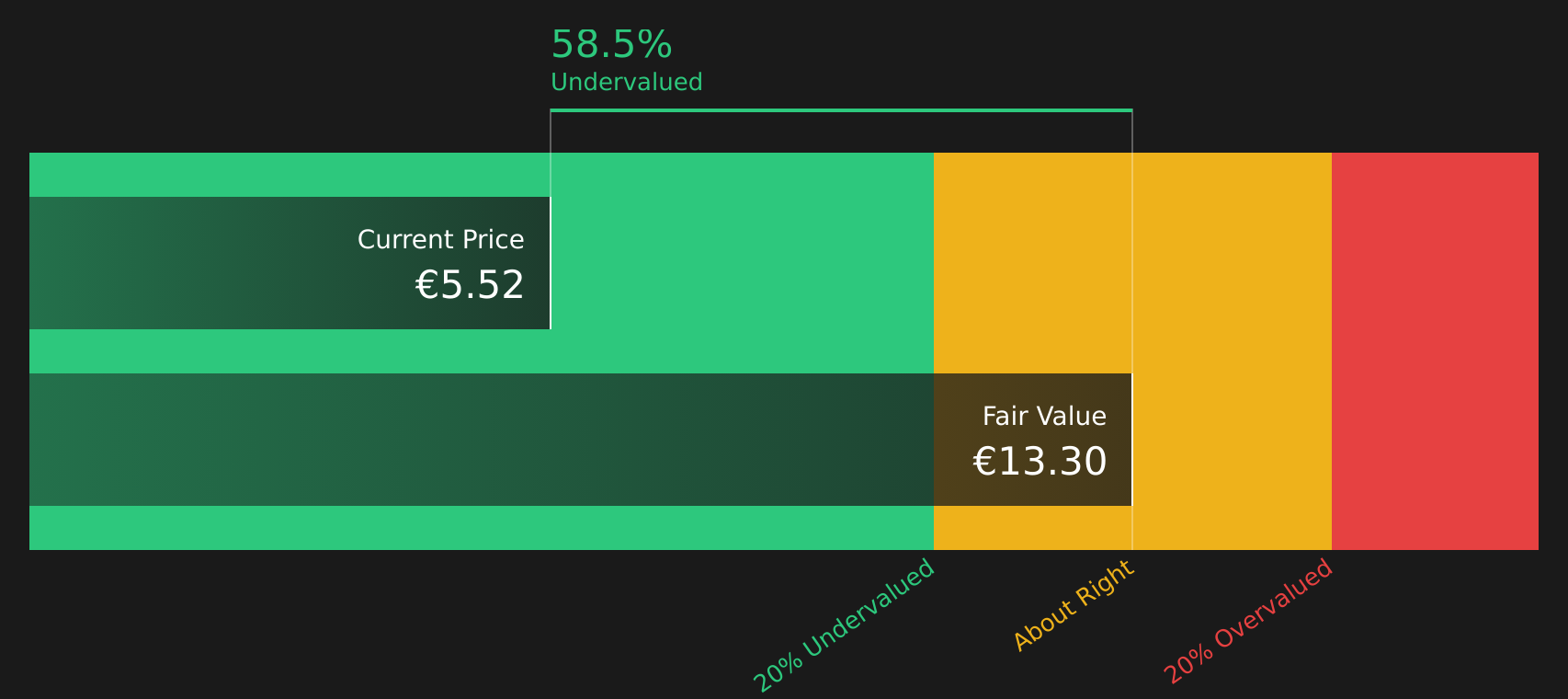

Operations: Take-Two generates all of its US$6.7b revenue from the sale of software titles, with about US$3.9b coming from the United States and roughly US$2.7b from international markets.

Market Cap: US$47.3b

Investors watching the industry move away from fragile live service models toward premium, story led games may find Take-Two Interactive Software especially interesting. Its core strength is exactly that kind of blockbuster content, anchored by Grand Theft Auto VI, Red Dead Redemption and NBA 2K, plus a broad mobile lineup that spreads risk across many titles. At the same time, the stock is not cheap on P/S, the company is currently loss making and analysts highlight reliance on external borrowing and heavy GTA VI development spend as key financial pressure points. With analyst expectations tied closely to GTA VI’s launch and GTA Online monetization, the key consideration is whether this pivot away from live service headwinds leaves Take-Two in a stronger position than more exposed peers.

Take-Two’s blockbuster pipeline and heavy GTA VI spend could be masking a tighter funding story, so it can help to see how the balance sheet and cash flows fit together in one place using the Take-Two Interactive Software financial health report

Ubisoft Entertainment (ENXTPA:UBI)

Overview: Ubisoft Entertainment is a French video game publisher that creates, develops and operates franchises like Assassin’s Creed, Far Cry, Rainbow Six and Just Dance across consoles, PC and mobile, selling both boxed and digital versions worldwide.

Market Cap: €743m

Ubisoft Entertainment sits at the uncomfortable center of the live service debate, with heavy exposure to ongoing titles such as Rainbow Six Siege and The Division, at a time when the Destiny 2 reset is making investors question how durable this model really is. The company is still loss making, with a reported net loss of €1,475.2m on €1,395.7m of sales and share price performance that has lagged the French entertainment sector, while funding is fully reliant on external borrowing. At the same time, the Tencent backed Vantage Studios stake, cloud streaming rights from the Activision deal and a refreshed portfolio built around Assassin’s Creed and other “billionaire brands” mean the gap between asset value and today’s distressed valuation is hard to ignore, especially if the live service bets do not pay off as planned.

Ubisoft Entertainment’s loss making profile and reliance on live service titles raise the question of what might still be hidden in its funding and portfolio reset. Get the full picture inside the analysis report for Ubisoft Entertainment

Electronic Arts (EA)

Overview: Electronic Arts is a global game publisher that creates and sells console, PC and mobile titles across genres such as sports, racing, shooters and simulation, including long running franchises like EA SPORTS football and Madden NFL, as well as live service worlds built around The Sims, Apex Legends and Battlefield.

Operations: Electronic Arts generates US$7.5b of revenue from console, mobile and PC free to download games, with around US$4.5b from international markets and US$3.0b from North America.

Market Cap: US$51.5b

Electronic Arts sits at the heart of the live service debate, with management saying about three quarters of the business comes from recurring live services just as the Destiny 2 reset is shaking confidence in this model. That heavy exposure, combined with revenue and earnings forecasts that trail broader US market expectations and an elevated P/E multiple, leaves less room for disappointment if titles like Apex Legends or EA SPORTS FC underperform. At the same time, the company is being taken private in a US$55b leveraged buyout backed by a US$20b debt package. This shifts risk toward balance sheet leverage and away from ordinary shareholders. If live services soften while debt costs bite, the gap between EA’s quality franchises and its funding profile could matter more than many investors expect.

Electronic Arts’ heavy live service reliance, lofty P/E and new leveraged buyout raise the question of what investors might be missing on future resilience. Get the fuller story inside the analysis report for Electronic Arts

Take Control of Your Investment Journey

If Take-Two Interactive Software or any of these companies have caught your attention, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value and track any new developments as they happen. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Fresh Alternatives Before They Fly?

New themes can move from quiet to breakout quickly, and the best entry points often drop out of sight once momentum builds. Check these curated stock ideas and consider whether they fit your approach.

- Explore potential early-stage momentum by scanning 18 high quality undiscovered gems that are still under the radar for now but might not stay overlooked for long.

- Strengthen your core with a curated list of solid balance sheet and fundamentals (47 results) so you are focusing on companies where financial resilience is a key consideration.

- Review opportunities in automation by checking the 29 robotics and automation stocks that could be positioned to participate as robotics and smart factories gain real world traction.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.