Taking A Fresh Look At Construction Partners (ROAD) Valuation After Recent Share Price Moves

Construction Partners, Inc. Class A ROAD | 106.72 | -1.98% |

Event driven snapshot of Construction Partners

Construction Partners (ROAD) has attracted fresh attention after recent share price moves, with the stock closing at $114.77. Investors are weighing this level against the company’s fundamentals, returns, and current valuation metrics.

After a small 2.37% decline in the latest session, the recent 2.33% year to date share price return sits alongside a 1 year total shareholder return of 41.83% and a very large 5 year total shareholder return. Together, these suggest momentum has been broadly positive even if short term sentiment has cooled.

If ROAD’s move has you thinking about where else capital could work hard, this might be a good moment to broaden your search with fast growing stocks with high insider ownership.

So with ROAD delivering a 41.83% 1 year total return and trading at $114.77 against an average analyst target of $127.43, is the stock still mispriced, or is the market already baking in future growth?

Most Popular Narrative: 9.2% Undervalued

At $114.77 against a narrative fair value of about $126.43, Construction Partners is framed as undervalued, with the story hinging on multi year funding and margin assumptions.

The company's concentration in high growth Sunbelt regions, particularly with recent transformative acquisitions like Lone Star in Texas and Durwood Greene in Houston, aligns with continued migration and urbanization trends that will drive outsized growth in contract awards, organic revenue, and market share.

Ongoing vertical integration through investment in owned asphalt plants and material sourcing combined with increasing scale, is already enhancing operational efficiencies and margin expansion, as shown by record adjusted EBITDA margins despite weather disruptions, this should drive higher net margins and improved earnings resilience going forward.

For readers curious about the revenue path and earnings changes implied by that fair value, and how rich a future P/E multiple the narrative leans on, the full story lays out the exact growth pace, margin lift and valuation bridge that need to line up for that $126.43 view to hold.

Result: Fair Value of $126.43 (UNDERVALUED)

However, that story can unravel quickly if public infrastructure funding tightens, or if higher labor and material costs start to squeeze margins more than expected.

Another View: High P/E Puts Pressure On The Story

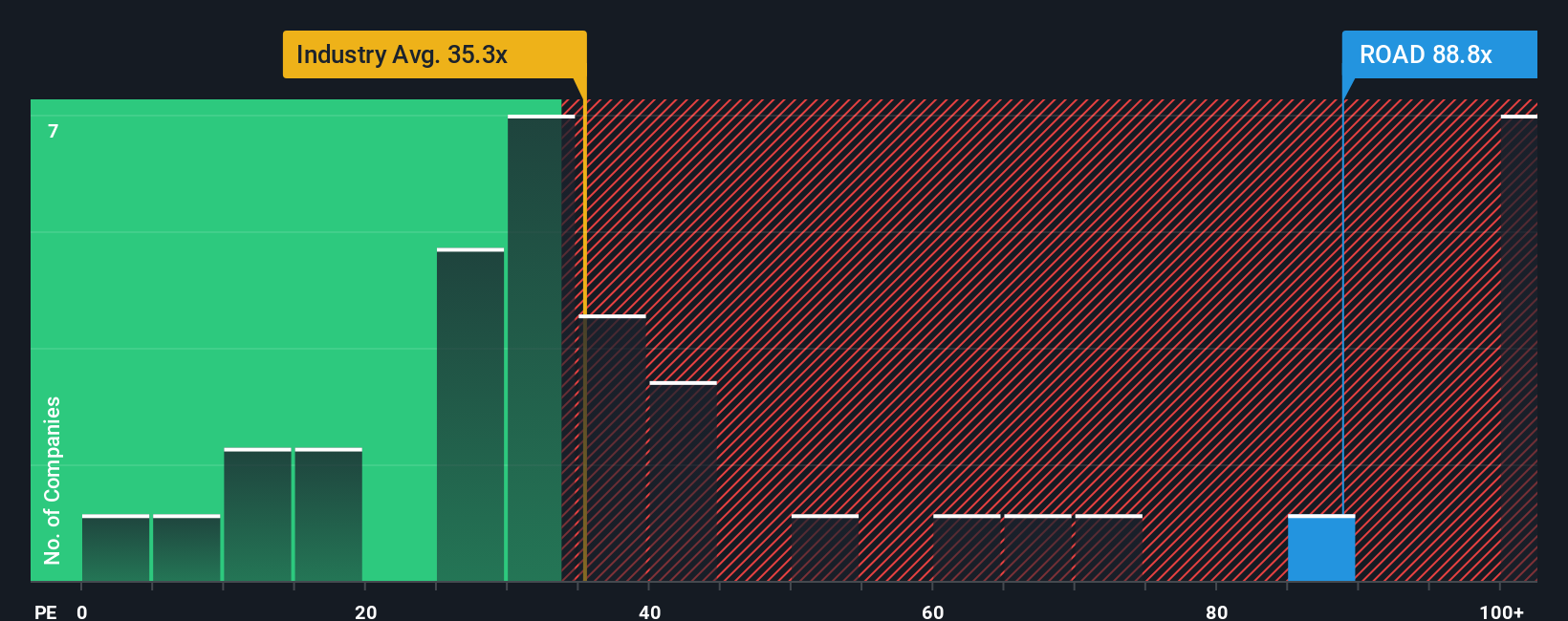

The narrative fair value points to about 9.2% upside, but the current P/E of 63.7x tells a different story. That is well above the US Construction industry at 36.9x, the peer average at 34.5x, and the fair ratio of 32.3x, which suggests less room for error if growth or margins fall short. So is this a valuation cushion or a valuation tightrope for you?

Build Your Own Construction Partners Narrative

If parts of this story do not quite fit your view, or you would rather test the numbers yourself, you can build a custom thesis in minutes with Do it your way.

A great starting point for your Construction Partners research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If ROAD has you thinking more broadly about where to put your next dollar to work, do not stop here, the market offers plenty of other focused ideas.

- Spot potential mispricings by scanning these 864 undervalued stocks based on cash flows that line up with your own view of fair value and cash flow strength.

- Back bold growth themes by checking out these 27 AI penny stocks that are tying artificial intelligence to real business models and financials.

- Position for income and compounding by reviewing these 11 dividend stocks with yields > 3% that already offer yields above 3%.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.