Talen Energy (TLN) Is Up 21.0% After AWS Pact, Plant Acquisitions, And Equity Shelf Filing

Talen Energy Corp TLN | 0.00 |

- Talen Energy Corporation recently filed a shelf registration to offer 2,399,998 shares of common stock, totaling approximately US$983.54 million, while also expanding its credit facilities and completing acquisitions of three natural gas power plants in the western PJM market.

- Goldman Sachs has now initiated coverage of Talen Energy, highlighting the company’s long-term power purchase agreement with Amazon Web Services and positioning within a tightening PJM power market as key drivers of its investment appeal.

- Building on Goldman Sachs’ focus on Talen’s long-term AWS agreement, we’ll examine how this development may reshape the company’s investment narrative.

Capitalize on the AI infrastructure supercycle with our selection of the 49 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

Talen Energy Investment Narrative Recap

To own Talen, you need to believe that data center driven demand in PJM and the long term AWS contract can underpin more stable cash flows while the company manages fossil fuel exposure and leverage. The latest shelf registration and credit expansions mainly affect how Talen funds growth rather than its key near term catalyst, which remains execution on contracted nuclear supply to AWS, while elevated leverage tied to acquisitions is still the most important risk.

The completion of the three natural gas plant acquisitions in the western PJM market is especially relevant here, because it deepens Talen’s exposure to the very region Goldman Sachs highlights as tightening and extends the company’s dependence on fossil assets that sit at the heart of both its cash flow potential and its policy and decarbonization risk.

Yet against this growth story, investors should also weigh the possibility that tighter regulation and faster decarbonization policy could materially affect Talen’s fossil fleet...

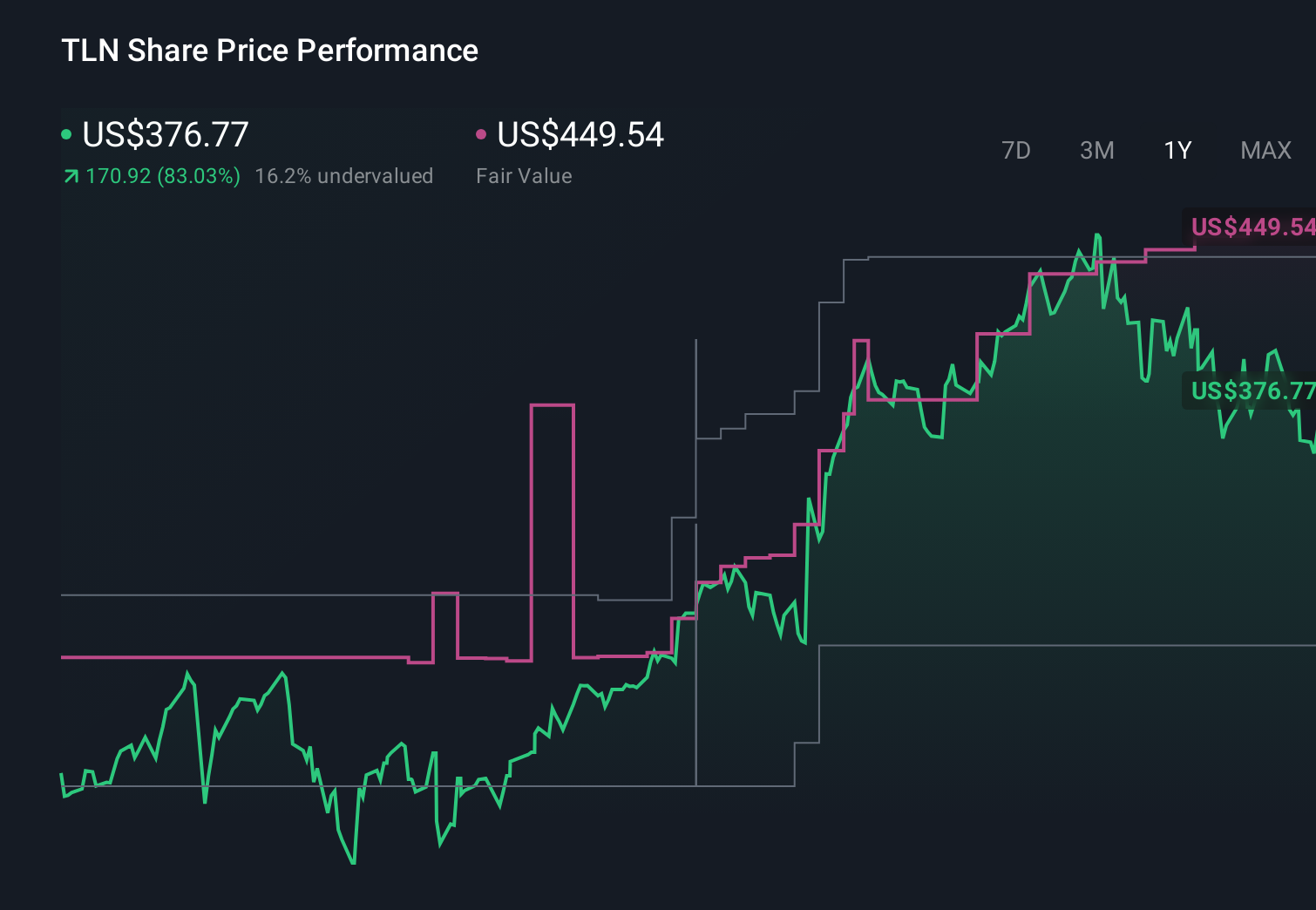

Talen Energy’s narrative projects $4.9 billion revenue and $1.4 billion earnings by 2029.

Uncover how Talen Energy's forecasts yield a $469.57 fair value, a 8% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were already modeling about US$6.2 billion of 2029 revenue and US$2.1 billion of earnings, which is far more upbeat than the baseline view and assumes fossil heavy assets face manageable policy headwinds rather than severe long term pressure.

Explore 6 other fair value estimates on Talen Energy - why the stock might be worth over 3x more than the current price!

Form Your Own Verdict

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Talen Energy research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Talen Energy research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Talen Energy's overall financial health at a glance.

Contemplating Other Strategies?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 29 best rare earth metal stocks of the very few that mine this essential strategic resource.

- AI is about to change healthcare. These 41 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Find 45 companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.