Tapestry (TPR) Stock After 89% Annual Gain Is Future Growth Already Priced In

Tapestry TPR | 0.00 |

- Wondering if Tapestry stock still offers value after its recent run, or if expectations have already been priced in? This article breaks down what the current share price could mean for you.

- The stock last closed at US$147.42, with returns of 5.2% over 7 days, 11.1% over 30 days, 14.2% year to date and 89.2% over 1 year, plus very large 3-year and 5-year gains of 265.6% and 307.6% respectively.

- Recent attention on Tapestry has been shaped by ongoing coverage of the luxury sector and its role in consumer spending, which keeps investor focus on how resilient premium brands can be. Broader discussions about consumer confidence and discretionary spending trends also feed into how the market currently prices Tapestry stock.

- Despite this strong share price history, Tapestry currently scores 0 out of 6 on Simply Wall St's valuation checks for potential undervaluation, giving it a value score of 0/6. Next, you will see how different valuation methods assess the stock and, later on, an even more rounded way to think about valuation as part of your overall decision making.

Tapestry scores just 0/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

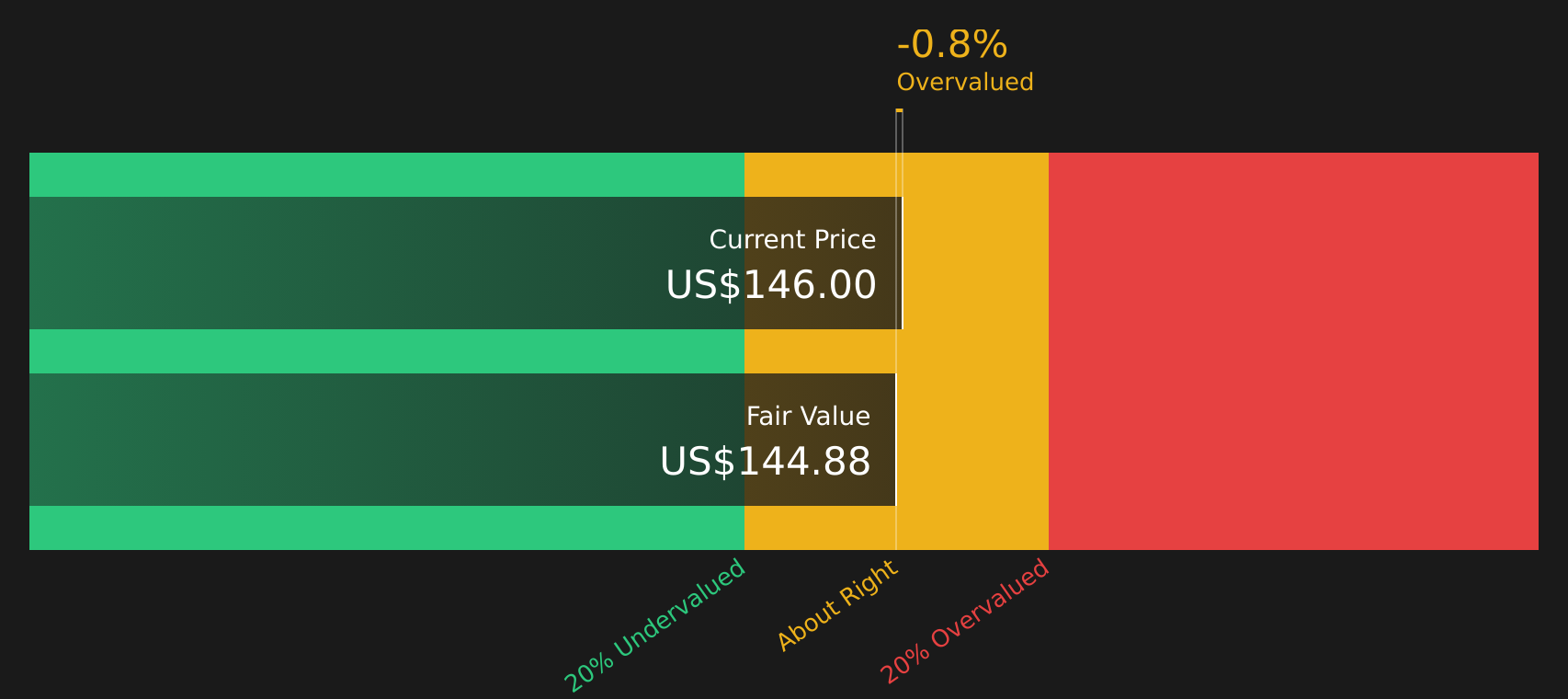

Approach 1: Tapestry Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model projects the cash Tapestry could generate in the future and then discounts those cash flows back to today to estimate what the business might be worth in dollars right now.

Tapestry’s latest twelve month free cash flow is about $1.76b. Using a 2 Stage Free Cash Flow to Equity model, analysts supply explicit forecasts through 2028, with Simply Wall St extrapolating beyond that. For example, projected free cash flow for 2028 is $1.78b, and the model then extends out to 2035 with estimated figures such as $2.12b. Each year is discounted back to today using the chosen rate.

Adding these discounted cash flows together gives an estimated intrinsic value of about $144.78 per share. Compared with the recent share price of $147.42, the DCF output suggests Tapestry is around 1.8% above this model’s estimate. This indicates the stock is trading very close to the calculated fair value.

Result: ABOUT RIGHT

Tapestry is fairly valued according to our Discounted Cash Flow (DCF), but this can change at a moment's notice. Track the value in your watchlist or portfolio and be alerted on when to act.

Approach 2: Tapestry Price vs Earnings

For a profitable company like Tapestry, the P/E ratio is a useful way to think about value because it links what you pay for each share to the earnings that share currently generates. In simple terms, higher growth expectations and lower perceived risk usually support a higher, or more generous, P/E, while slower growth and higher risk tend to justify a lower multiple.

Tapestry is currently trading on a P/E of 44.94x. That sits well above both the Luxury industry average P/E of 24.44x and the peer group average of 24.26x. To give more context, Simply Wall St also calculates a “Fair Ratio” of 28.17x for Tapestry. This proprietary figure reflects factors such as earnings growth expectations, profit margins, industry, market cap and company specific risks.

This Fair Ratio can be more informative than a simple comparison with peers or the industry, because it is tailored to Tapestry’s own profile rather than assuming all companies deserve the same multiple. Compared with the current 44.94x P/E, the Fair Ratio of 28.17x indicates that the stock is trading at a richer level than that model suggests.

Result: OVERVALUED

Wall Street's queuing for one rocket. While SpaceX counts down to its IPO, other companies tied to the new space race are already in orbit. → 20 Compelling Space Companies watchlist · Global Space Race Investing Ideas screener · Scan the sector by valuation on Rocket Lab's valuation page.

Upgrade Your Decision Making: Choose your Tapestry Narrative

Earlier it was mentioned that there is an even better way to understand valuation. This is where Narratives come in, a simple tool on Simply Wall St's Community page that lets you attach a clear story about Tapestry to the numbers you think are realistic for its future revenue, earnings, margins and fair value.

Instead of only looking at a single P/E or DCF output, a Narrative links the company story you believe, the forecast that flows from that story, and the fair value that falls out of those assumptions. It then compares that fair value with the current share price to help you decide whether the stock looks expensive or cheap to you.

Narratives are updated automatically when new information such as news or earnings is entered into the platform. This means the fair value that sits behind each story adjusts as the inputs change rather than remaining frozen at one snapshot in time.

For Tapestry, one investor might align with a higher fair value of US$200.00 based on expectations of stronger revenue growth, higher profit margins and a future P/E near 23x. Another investor might lean toward a lower fair value of about US$111.38 using more cautious assumptions and a future P/E closer to 16x, and the Community page makes those differing perspectives easy to compare side by side.

For Tapestry however we will make it really easy for you with previews of two leading Tapestry Narratives:

Start by asking which story you think fits the current price, and whether the assumptions behind it feel realistic given your view on the business.

Fair value in this bullish narrative: US$200.00

Current price compared with this fair value: about 26.3% below the narrative fair value, based on the recent close of US$147.42

Revenue growth assumption: 7.32% a year

- Focuses on younger customer retention and digital sales as a compounding engine for higher revenue and wider margins over time.

- Leans on international growth, especially Europe and Greater China, plus AI supported omnichannel tools to sustain earnings expansion.

- Assumes that disciplined capital allocation and buybacks help support a richer future P/E and a fair value of US$200.00.

Fair value in this cautious narrative: about US$111.38

Current price compared with this fair value: about 32.4% above the narrative fair value, based on the recent close of US$147.42

Revenue growth assumption: 4.51% a year

- Highlights risks from changing consumer preferences, higher trade and compliance costs, and tougher digital competition for Coach and Kate Spade.

- Points to the possibility that tariffs, brand fatigue and rising expenses could pressure margins, even if revenues continue to grow.

- Assumes a lower future P/E and a fair value closer to US$111.38, implying the stock already prices in more optimism than this view supports.

If these two narratives feel too far apart, your own view may sit somewhere in the middle. This is exactly where Community Narratives are useful. You can stress test your assumptions against others and see how different stories translate into very different fair values. See what the community is saying about Tapestry.

Do you think there's more to the story for Tapestry? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.