Tempus AI (TEM) Valuation Revisited After New Immune Profile Score Clinical Validation

Tempus Al TEM | 45.98 46.45 | +7.08% +1.02% Pre |

Tempus AI (TEM) is back in focus after unveiling new clinical data on its Immune Profile Score test. The company says the test predicts responses to immune checkpoint inhibitors more accurately than established biomarkers like TMB, MSI, and PD L1.

The IPS update lands after a mixed stretch for the stock, with a 1-day share price return of 4.71% taking Tempus AI to US$54.91. However, a 30-day share price return of 21.30% and 1-year total shareholder return of 20.37% both point to fading momentum despite recent product and data milestones.

If Tempus AI’s progress in oncology has caught your attention, it could be worth seeing what else is emerging in this space with our screener of 26 healthcare AI stocks.

With Tempus AI shares down over the past month and year despite clinical and product progress, and with a wide gap to published analyst targets and intrinsic estimates, it is reasonable to ask whether this is a mispriced opportunity or whether the market is already factoring in future growth.

Most Popular Narrative: 37.5% Undervalued

Tempus AI’s most followed narrative puts fair value at about $87.92 per share, well above the last close at $54.91. This sets up a clear valuation gap built on growth and margin expectations.

Robust discipline in investment and operating leverage, as evidenced by rapid revenue growth paired with improving adjusted EBITDA and gross margins, supports near-term profitability and strengthens the case for long-term scalable earnings expansion. Secular increases in the adoption of AI and data analytics in drug development, along with broadening regulatory clarity for digital diagnostics, suggest Tempus AI is uniquely positioned to capture a growing share of healthcare spending, directly increasing revenue and fortifying future margin improvement opportunities.

Want to see what is baked into that price gap? The narrative leans heavily on brisk revenue compounding, richer margins and a premium future earnings multiple. The model also applies a specific discount rate to pull those future cash flows back to today. Curious which assumptions need to line up for $87.92 to make sense?

Result: Fair Value of $87.92 (UNDERVALUED)

However, you still need to weigh real pressure points, including reimbursement and regulatory setbacks that could limit assay uptake, along with heavier R&D spending straining margins.

Another Take: Multiples Point to a Richer Price

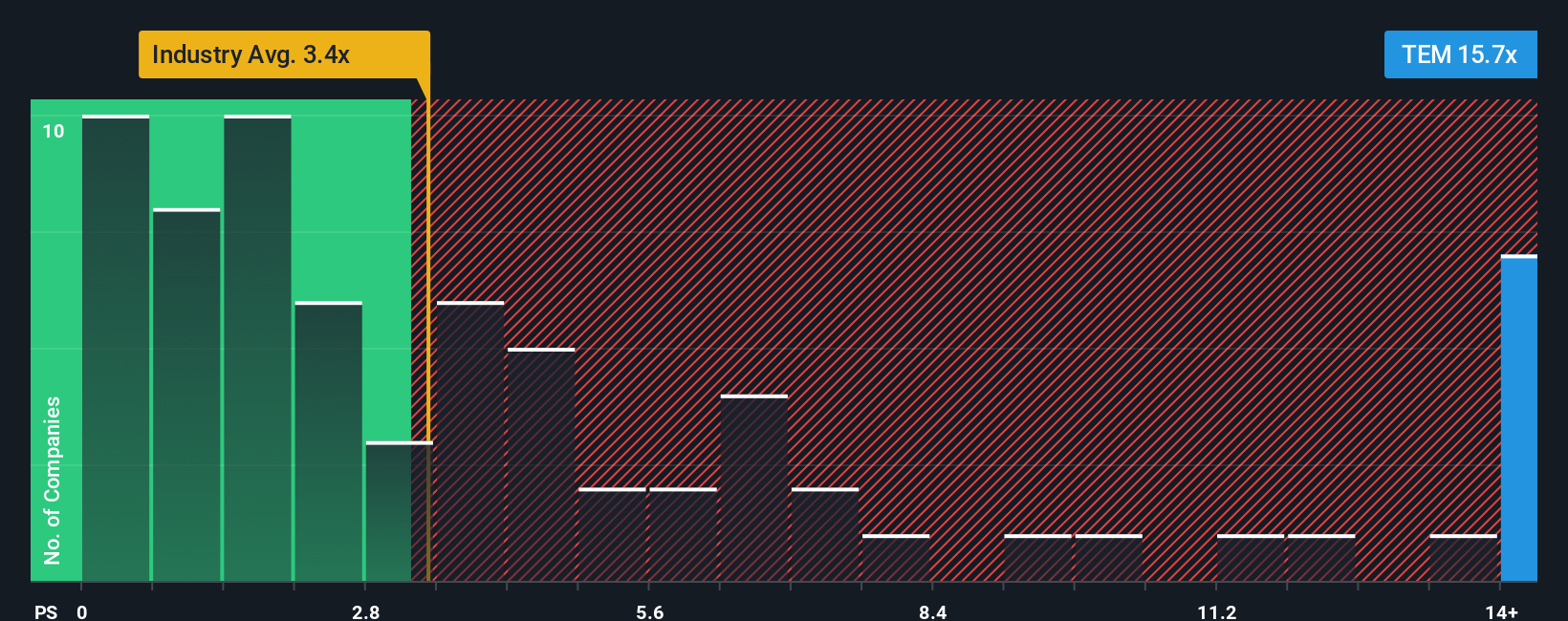

The narrative model sees Tempus AI as 37.5% undervalued, yet the market is already pricing the stock at a P/S of 8.8x. That is materially higher than the US Life Sciences industry at 2.8x, peers at 4.7x, and even its own fair ratio of 7.8x. This suggests there may be less margin for error than the story implies. Which signal do you trust more: the story or the sticker price?

Build Your Own Tempus AI Narrative

If you are not fully aligned with these views or prefer to weigh the data on your own terms, you can build a custom thesis in minutes with Do it your way.

A great starting point for your Tempus AI research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If Tempus AI has you thinking more broadly about opportunities, do not stop here, the market is full of other ideas that could suit your style.

- Target value by running through 53 high quality undervalued stocks, a focused set of companies where price and fundamentals may be out of sync.

- Prioritise resilience with 87 resilient stocks with low risk scores, highlighting businesses that score well on stability and downside protection.

- Hunt for under the radar potential using our screener containing 25 high quality undiscovered gems, where quality fundamentals meet limited current attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.