TeraWulf (WULF): Evaluating Valuation After Preferred Stock Conversion and AI Infrastructure Pivot

TeraWulf Inc. WULF | 0.00 |

TeraWulf (WULF) recently converted all outstanding Series A preferred shares into common stock after meeting its conversion threshold. This move simplifies the company’s capital structure and underscores its stronger financial footing.

TeraWulf’s strategic pivot from bitcoin mining to developing renewable-powered AI infrastructure has fueled a surge in investor confidence, particularly following its recent lease agreements and improved capital structure. In the past 90 days, the stock recorded a share price return of over 61 percent, while its one-year total shareholder return is nearly 112 percent. This indicates significant momentum as the company expands its growth narrative beyond mining.

If you’re watching major developments like TeraWulf’s, now could be a great time to broaden your investing horizons and discover fast growing stocks with high insider ownership

With shares up sharply in the past year and analyst price targets still well above current levels, investors now face a familiar dilemma: is there more upside ahead for TeraWulf, or has the market already priced in its transformation?

Most Popular Narrative: 27.7% Undervalued

With TeraWulf last closing at $15.51, the most widely followed narrative places its fair value at $21.44 per share. This premium is attributed to optimism surrounding the company's transition and growth outlook.

Long-term partnerships and investments from marquee players (Google's $1.8B lease backstop and equity stake) signal institutional validation, enhance creditworthiness, and are likely to lower WULF's future cost of capital, directly supporting margin expansion and accelerated infrastructure growth.

The real surprise? This narrative is built on bold assumptions, including substantial revenue growth, significant margin improvements, and positive profit projections. Want to see the exact growth numbers and margin changes driving TeraWulf’s premium fair value? Find out what’s fueling analyst conviction behind that price target.

Result: Fair Value of $21.44 (UNDERVALUED)

However, persistent risks remain, particularly around increased capital expenditures and uncertainty in demand for AI hosting. Both of these factors could quickly change the outlook.

Another View: Valuation Gaps Highlight Risk

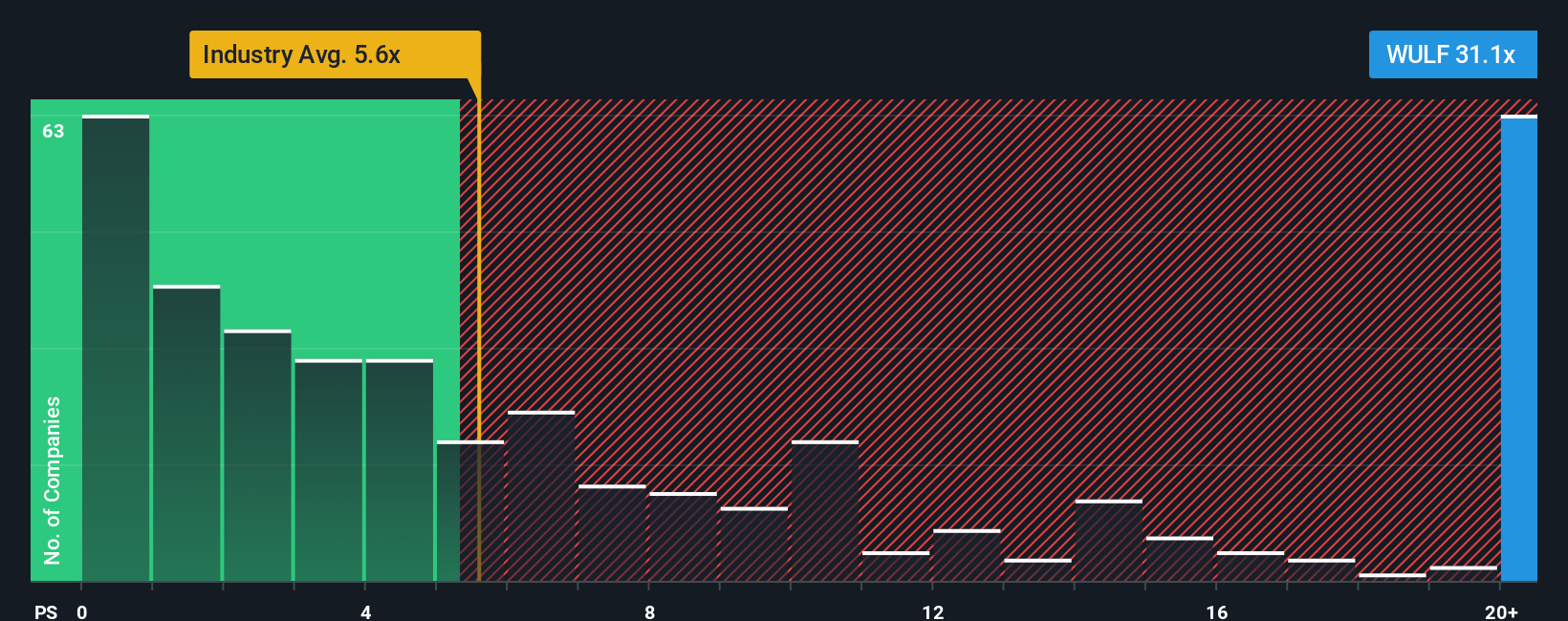

Looking through the lens of price-to-sales, TeraWulf’s valuation stands out. Its ratio of 38.7x is significantly higher than both the US Software industry average of 4.9x and the peer average of 20.7x. Even compared to the market’s fair ratio of 14x, WULF appears stretched, raising larger questions about downside risk if the narrative changes. Could momentum alone keep these multiples elevated?

Build Your Own TeraWulf Narrative

If you have a different perspective or want to dig deeper into the numbers, take a few moments to craft your personal take. You can do it in just minutes with Do it your way.

A great starting point for your TeraWulf research is our analysis highlighting 1 key reward and 3 important warning signs that could impact your investment decision.

Looking for more investment ideas?

There's a world of opportunities beyond TeraWulf. Here are three smart places to put your research to work and help you spot your next big winner.

- Spot companies redefining healthcare by tapping into leading-edge advances in medical technology with these 30 healthcare AI stocks.

- Unlock additional long-term growth potential by checking out these 913 undervalued stocks based on cash flows, where cash flow fundamentals reveal companies trading below their true worth.

- Capture rising trends in digital transformation by zeroing in on these 25 AI penny stocks propelling artificial intelligence into everyday life.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.