Terreno Realty (TRNO) Could Be 4% Overvalued On Fresh Leasing And Acquisitions

Terreno Realty Corporation TRNO | 0.00 |

Terreno Realty (TRNO) has reported a cluster of fresh leasing and acquisition activity, including new leases in California and New Jersey, as well as recent industrial property purchases in Florida, Maryland and Virginia, giving investors more detail on portfolio positioning.

Terreno Realty's recent leasing and acquisition updates come as the stock trades at $65.98, with an 8.72% 90 day share price return and a 21.64% 1 year total shareholder return, which suggests momentum has been building rather than fading.

If these industrial updates have caught your eye, it can also be useful to see what other infrastructure style plays are doing right now, starting with 35 power grid technology and infrastructure stocks

With Terreno Realty trading at $65.98, sitting only modestly below the average analyst price target and carrying a relatively low value score of 2, the key question is whether the recent leasing and acquisition news signals a genuine opportunity or if the market is already pricing in future growth.

Price-to-Earnings of 16.6x: Is it justified?

Terreno Realty is trading on a P/E of 16.6x, which sits below the wider US market but slightly higher than the global Industrial REITs group.

The P/E ratio compares the current share price with earnings per share. In other words, it shows how much investors are paying for each dollar of Terreno Realty's earnings.

Terreno Realty's P/E is below the overall US market average of 18.9x and below an estimated fair P/E of 24.1x. This points to a lower price tag relative to those benchmarks. However, the stock trades on a higher P/E than the global Industrial REITs industry average of 15.7x, which suggests investors are paying a premium compared to sector peers.

Result: Price-to-Earnings of 16.6x (ABOUT RIGHT)

However, Terreno Realty's annual net income contraction and its relatively low value score of 2 suggest that earnings quality and valuation support could still face pressure.

Another View on Terreno Realty's Value

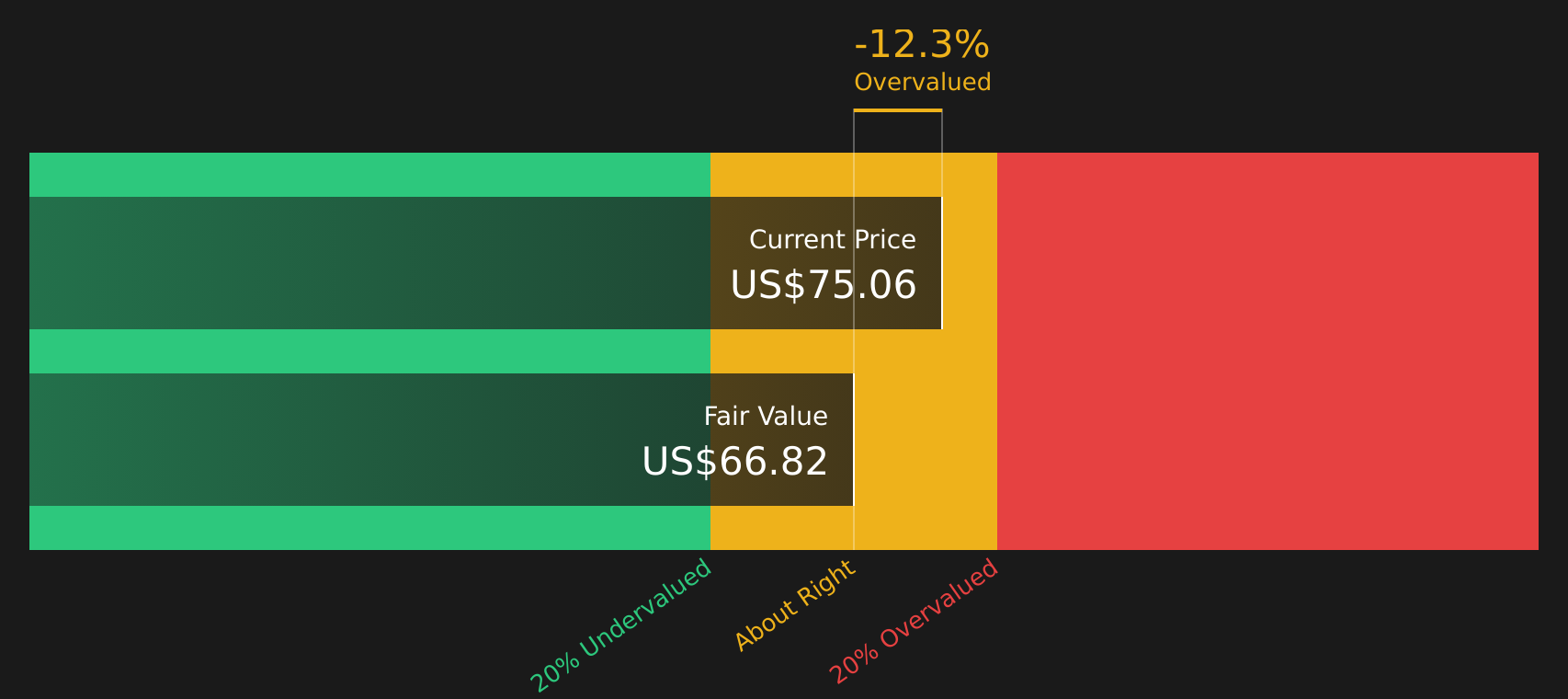

While Terreno Realty screens as good value on its 16.6x P/E compared with a fair ratio of 24.1x, a different lens tells a more cautious story. The SWS DCF model estimates the stock's future cash flow value at $63.49, which is below the current $65.98 share price and points to a degree of overvaluation.

For readers who want to see how that cash flow based estimate is built step by step, Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Terreno Realty for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 44 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With sentiment on Terreno Realty appearing finely balanced between concerns and optimism, take a moment to review the data yourself and act while the details are fresh, starting with 3 key rewards and 2 important warning signs.

Looking for more investment ideas beyond Terreno Realty?

If Terreno Realty has sharpened your focus on opportunities, do not stop here. Broaden your watchlist now so you are not late to the next idea.

- Spot potential value opportunities early by scanning companies highlighted in the 44 high quality undervalued stocks.

- Prioritize capital preservation and consistency by reviewing companies in the 71 resilient stocks with low risk scores.

- Hunt for under-the-radar opportunities with strong fundamentals using the screener containing 19 high quality undiscovered gems.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.