Terreno Realty (TRNO) Stock Looks Fairly Priced With A Slight DCF Premium

Terreno Realty Corporation TRNO | 0.00 |

Terreno Realty (TRNO) continues to attract investor attention as an industrial REIT focused on major U.S. coastal markets. The stock recently closed at $64.35 and has shown mixed short term return trends.

Over the past year Terreno Realty has paired a 9.03% year to date share price return with a 14.53% 1 year total shareholder return, while the stronger 24.01% 3 year total shareholder return suggests momentum has been building over a longer period.

If this kind of steady interest in Terreno Realty has you thinking about what else is on investors’ radar, it may be worth scanning for other opportunities through our 20 top founder-led companies

With Terreno Realty trading at $64.35, revenue growth reported at 10.28% and a value score of 2, the key question is whether the recent performance leaves upside on the table or if the market is already pricing in future growth.

Price-to-Earnings of 16.2x: Is it justified?

Terreno Realty is trading on a P/E of 16.2x, which sits slightly below the wider US market but above the global Industrial REITs average, so the market appears to be paying a moderate premium relative to sector peers.

The P/E ratio compares the current share price to earnings per share and is often used for income focused, asset heavy businesses like REITs. For Terreno Realty, this multiple sits alongside a reliable 3.23% dividend yield and a recent history of strong reported earnings growth, although that growth is affected by one off items.

Compared with the global Industrial REITs industry average of 15.2x, Terreno Realty looks more expensive, which suggests investors are willing to pay more for each dollar of current earnings than they pay for the sector overall. However, when compared with the peer average P/E of 31x and an estimated fair P/E of 24.3x, the current 16.2x level is considerably lower. This indicates there may be room for the market multiple to move closer to that fair ratio if conditions justify it.

Result: Price-to-Earnings of 16.2x (ABOUT RIGHT)

However, Terreno Realty’s annual net income decline of 18.64% and its exclusive exposure to U.S. industrial real estate could challenge the current valuation narrative.

Another View on Terreno Realty: Cash Flows Paint a Tighter Picture

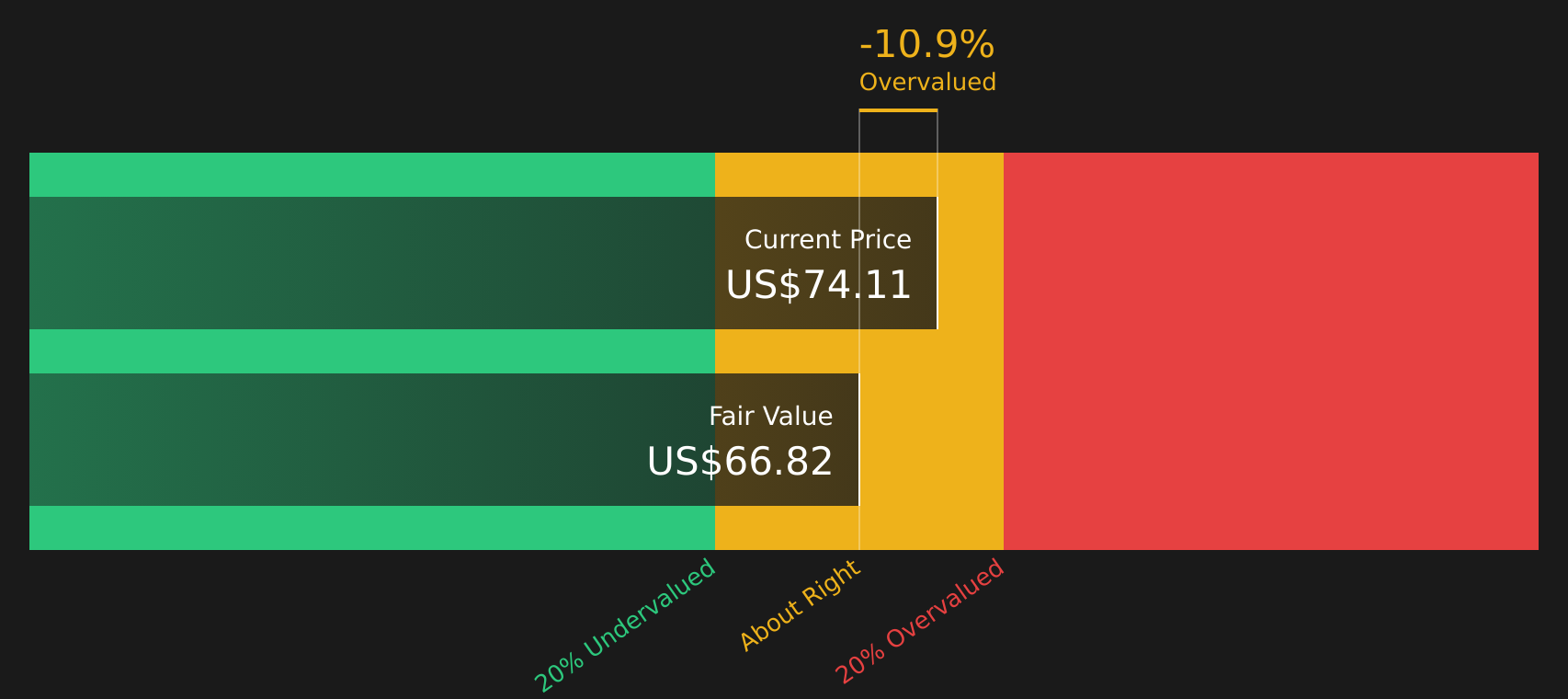

While Terreno Realty’s 16.2x P/E looks roughly in line with what investors might accept for an industrial REIT, the SWS DCF model tells a slightly different story. With the stock at $64.35 versus a future cash flow value estimate of $63.21, it screens as modestly overvalued rather than comfortably priced.

That gap is small in dollar terms, but it raises a useful question for you as an investor: is the market paying a bit extra for Terreno Realty’s story, or is the model being too cautious about its future cash generation?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Terreno Realty for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 45 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

Seeing mixed signals around Terreno Realty’s valuation and outlook? Take a closer look at the numbers, weigh both sides, and move quickly to form your own stance with the help of 3 key rewards and 2 important warning signs

Looking for more investment ideas beyond Terreno Realty?

If Terreno Realty has sharpened your focus on quality, do not stop here. Use the Simply Wall St Screener to uncover other stocks that could suit your approach.

- Target potential bargains with resilient fundamentals by scanning 45 high quality undervalued stocks that might align with your return goals and risk comfort.

- Strengthen your income stream by reviewing 8 dividend fortresses that aim to combine yield with staying power through different market conditions.

- Prioritize capital protection by focusing on 66 resilient stocks with low risk scores that score well on stability so you are not caught off guard when sentiment shifts.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.