Tesla (TSLA) Delivery Beat Keeps Its AI Led Valuation Debate Alive

Tesla Motors, Inc. TSLA | 0.00 |

Tesla (TSLA) has just reported second quarter 2026 deliveries of 480,126 vehicles and production of 451,758 units, giving investors fresh numbers to assess alongside the stock’s recent multi month rebound.

The strong Q2 2026 delivery beat has come alongside a 16.85% 90 day share price return and a 30.06% 1 year total shareholder return, even though the year to date share price return is still down 6.92%. This suggests momentum has recently picked up as investors weigh Tesla's robotaxi, AI and energy stories against ongoing regulatory and execution risks.

If Tesla's latest delivery beat has you thinking about where else growth and automation might matter, it could be worth scanning the 30 robotics and automation stocks.

Tesla now looks like a powerful business story again, but after a sharp rebound and fresh AI and robotaxi excitement, is the stock being priced as a solid car and energy company, or as something far more ambitious?

Most Popular Narrative: 30.7% Undervalued

With Tesla’s last close at $407.76 compared to a narrative fair value of $588.18, the most followed thesis argues the stock reflects much more than car making and energy today.

The Q4 results prove that Tesla can maintain 20%+ margins even while selling fewer cars, validating the shift away from pure volume chasing. The "Sum of the Parts" valuation model is being de-risked in real time, but the stakes have never been higher. Tesla has burned the boats. It is now AI or bust.

Want to see what sits behind that bold Tesla call? According to BlackGoat, the key levers are high growth expectations, richer margins and premium future multiples. Curious which assumptions have to hold together to justify a fair value that far above today’s price?

Result: Fair Value of $588.18 (UNDERVALUED)

However, Tesla’s AI heavy pivot still depends on a successful robotaxi rollout and large scale Optimus deployment, and regulatory or execution setbacks could quickly challenge this bullish narrative.

Another View: Tesla Looks Expensive On Sales

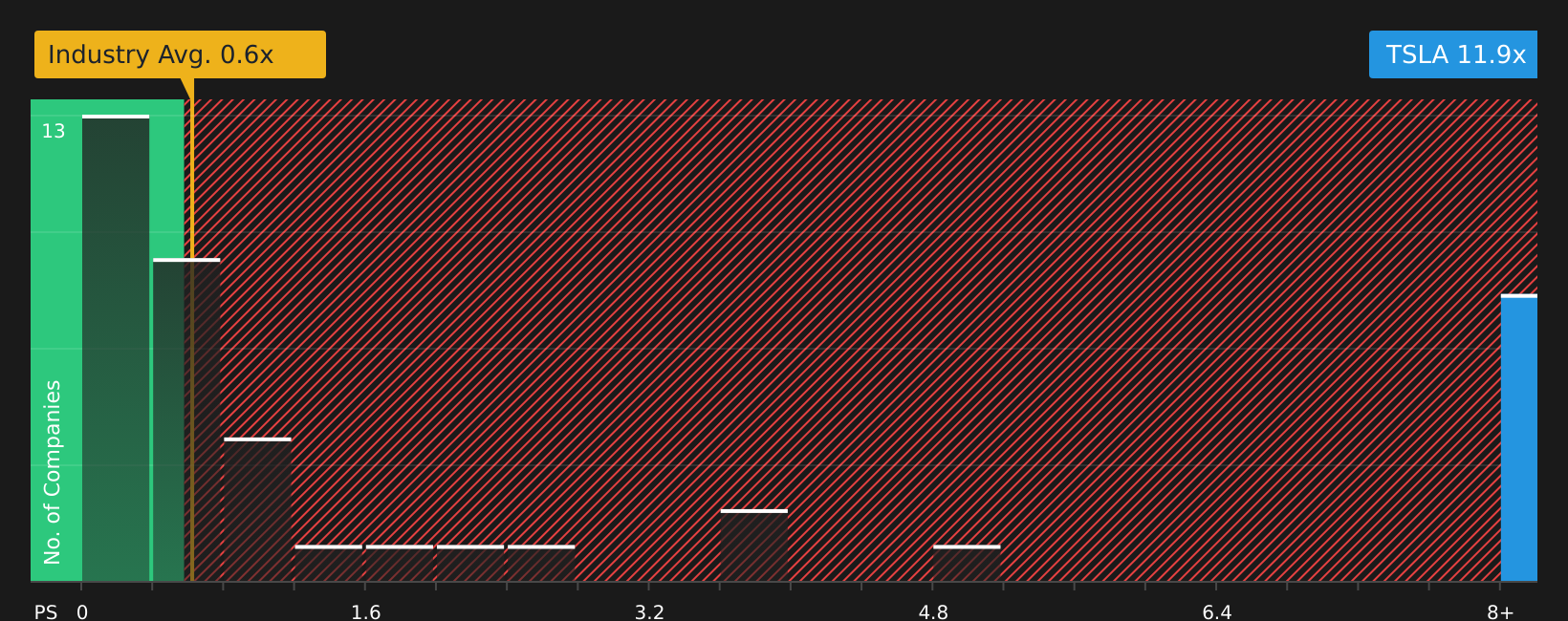

While the BlackGoat narrative points to Tesla as 30.7% undervalued, our P/S based view paints a very different picture. Tesla trades at a 15.6x P/S, compared with 0.6x for the US Auto industry and 1.4x for peers, versus a fair ratio estimate of 3.4x.

That kind of gap suggests the market already prices in a lot of future growth and high margin execution. This raises the question: how comfortable are you paying several times the fair ratio for Tesla’s AI and robotaxi story?

Next Steps

If this Tesla debate feels finely balanced, you can use the data to move quickly and firm up your own stance by checking the 1 key reward and 2 important warning signs.

Looking for more investment ideas beyond Tesla?

If you are serious about making the most of Tesla's latest numbers, do not stop here. Use fresh ideas from broader market screeners to sharpen your watchlist.

- Target potential mispricings early by scanning markets for quality stocks that look attractively valued with the 44 high quality undervalued stocks.

- Strengthen your income stream by focusing on companies with robust payouts using the 9 dividend fortresses.

- Prioritize resilience by filtering for companies that pair solid finances with lower risk profiles through the 76 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.