Tetra Tech (TTEK): Evaluating Valuation After Rare Earths Partnership Expansion and 2026 Growth Guidance

Tetra Tech, Inc. TTEK | 30.73 30.73 | +2.03% 0.00% Post |

Tetra Tech is expanding its partnership with American Rare Earths to help secure U.S. government funding for the Halleck Creek project. This move aligns with federal efforts to bolster domestic supply chains. The company also reported increased quarterly net income and released growth guidance for 2026, signaling continued business momentum.

Tetra Tech’s latest moves, including a deeper partnership in U.S. rare earths and fresh 2026 growth forecasts, have stirred investor interest. The share price sits at $34.12, recovering slightly with a 1.01% return over the past month after recent volatility. While short-term price performance has been choppy, long-term total shareholder returns remain solid, up nearly 46% over five years. This indicates that momentum is still on the company’s side for patient investors.

If you’re looking for your next discovery beyond Tetra Tech, now’s a perfect moment to explore fast growing stocks with high insider ownership.

So with business expanding and a fresh upturn in earnings, is there untapped value left in Tetra Tech’s shares, or have markets already accounted for its future growth potential?

Most Popular Narrative: 19% Undervalued

With Tetra Tech trading at $34.12 and the most-followed narrative assigning a fair value of $42.17, investor attention is focused on potential upside. The stage is set for further scrutiny of the underlying drivers behind this valuation gap.

Ongoing expansion of advanced digital automation and analytics offerings, catalyzed by rising adoption of AI and recent strategic acquisitions, positions Tetra Tech for higher-margin, tech-driven consulting services and recurring revenue streams. This supports long-term net margin and earnings growth.

Want a behind-the-scenes look at what’s driving this target? This valuation leans heavily on Tetra Tech’s shift toward smarter, recurring revenue and bold profit margin bets that could rewrite its financial future. Find out what powerful assumptions put the spotlight on these high-flying numbers.

Result: Fair Value of $42.17 (UNDERVALUED)

However, challenges such as reduced government contracts and unpredictable disaster response revenues could limit Tetra Tech's projected earnings momentum.

Another View: Market Multiples Tell a Cautionary Tale

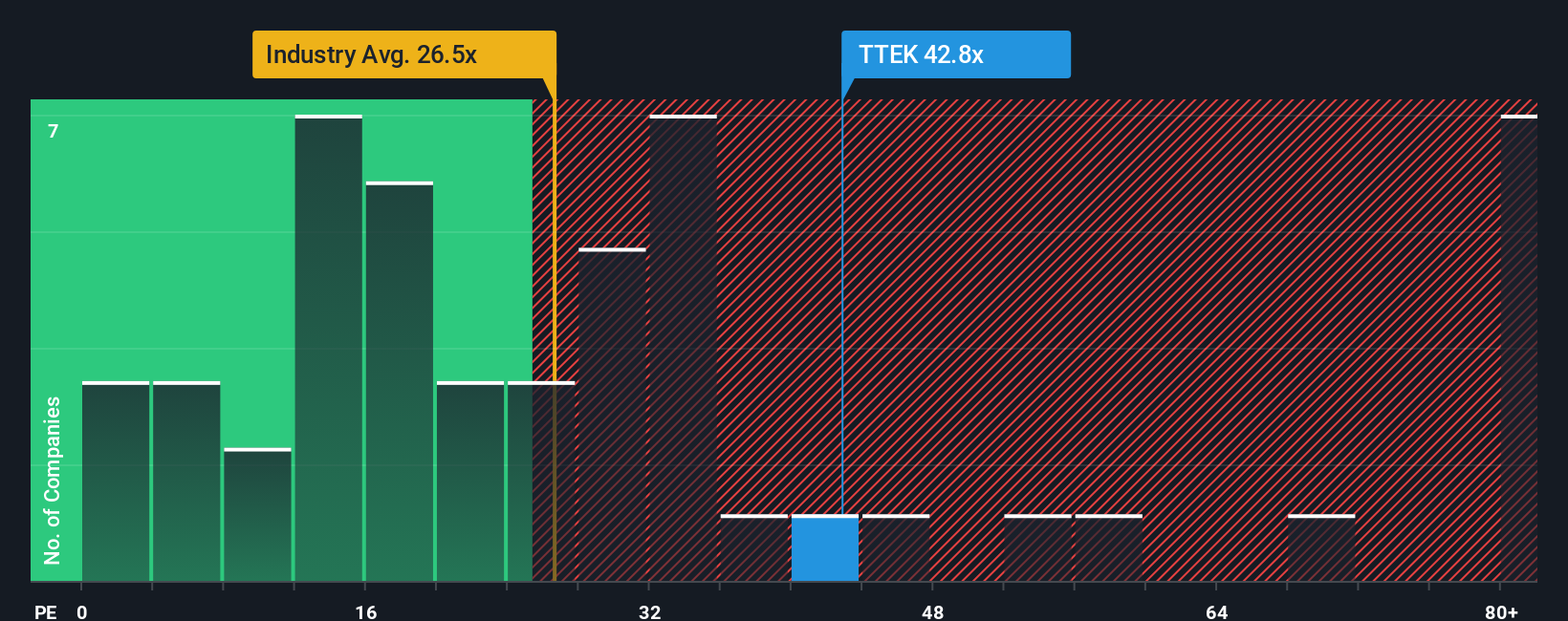

While analysts see upside based on future growth expectations, Tetra Tech’s current price-to-earnings ratio of 35.9x stands notably above the industry average of 21.9x and even higher than the peer average of 34.6x. It also exceeds the fair ratio of 31.5x, raising concerns that shares could be pricing in too much optimism already. Does this signal an elevated valuation risk, or do investors believe future profits warrant the premium?

Build Your Own Tetra Tech Narrative

If you’d rather dig deeper and construct your own story around Tetra Tech’s outlook, the data is yours to explore and analyze. Do it your way.

A great starting point for your Tetra Tech research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Looking for More Smart Investment Ideas?

There’s a world of opportunity beyond Tetra Tech. Use the Simply Wall Street Screener to zero in on unique stocks and fresh investment angles tailored to your interests.

- Catch early-stage gains by checking out these 3581 penny stocks with strong financials with strong financials and breakout momentum before the crowd moves in.

- Capitalize on the AI transformation by analyzing these 26 AI penny stocks as they lead cutting-edge advancements across industries for long-term upside.

- Boost your portfolio’s income stream by finding these 14 dividend stocks with yields > 3% that deliver generous yields above 3% and robust fundamentals.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.