The Bull Case For Air Products and Chemicals (APD) Could Change Following Yara-Linked Hydrogen Megaproject Talks - Learn Why

Air Products and Chemicals, Inc. APD | 0.00 |

- In early March 2026, Air Products and Chemicals reported that it was in advanced talks with Yara International on major hydrogen and ammonia projects in the U.S. and Saudi Arabia, while reaffirming its 2026 adjusted EPS guidance despite helium-related pressures.

- The planned Louisiana complex, estimated at about US$8.00–US$9.00 billion and targeting completion by 2030, together with expected renewable ammonia agreements linked to the NEOM Green Hydrogen Project from 2026, underscores how large energy-transition projects could reshape Air Products’ long-term contract base and project mix.

- We’ll now explore how reaffirmed earnings guidance amid these large Yara-linked hydrogen and ammonia projects may influence Air Products’ investment narrative.

Find 49 companies with promising cash flow potential yet trading below their fair value.

Air Products and Chemicals Investment Narrative Recap

To own Air Products and Chemicals, you really need to believe in its long term build out of hydrogen and ammonia projects, backed by take or pay style contracts, while accepting the hit from heavy capital spending and helium related earnings pressure. The latest Yara discussions and reaffirmed 2026 EPS guidance do not materially change the near term picture, where the key catalyst is execution on major energy transition projects and the main risk remains delays or cost overruns on these large builds.

Among recent announcements, the company’s decision in January 2026 to raise its quarterly dividend to US$1.81 per share, marking 44 consecutive years of increases, stands out. For many investors, that track record of returning cash, even while committing to multibillion dollar projects like the US$8.0–US$9.0 billion Louisiana complex and NEOM linked ammonia supply, is central to the appeal but also heightens sensitivity to how efficiently new capital in process is converted into earnings.

Yet behind the reaffirmed guidance and dividend growth, investors should be aware that...

Air Products and Chemicals' narrative projects $14.9 billion revenue and $3.8 billion earnings by 2028.

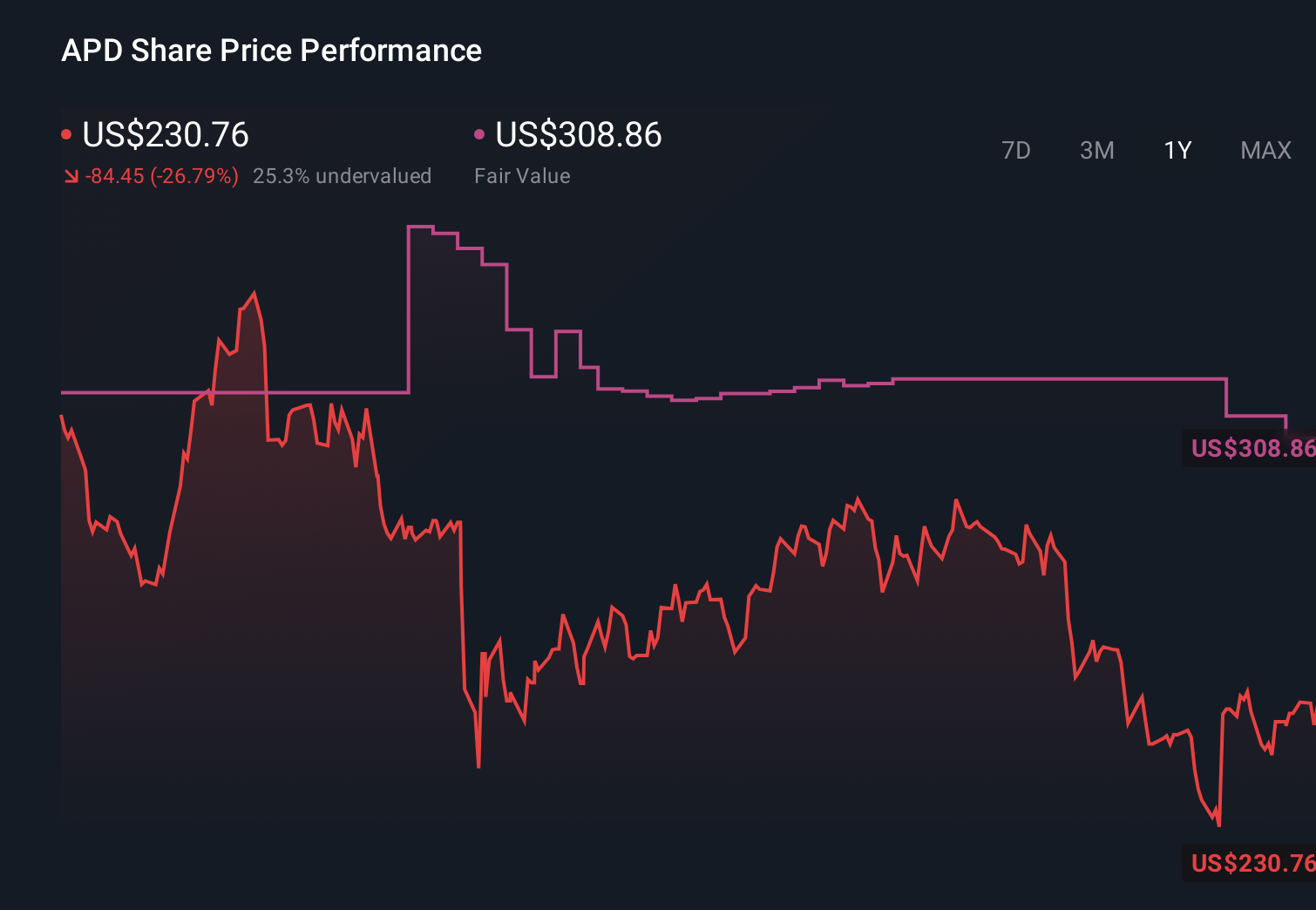

Uncover how Air Products and Chemicals' forecasts yield a $302.36 fair value, a 11% upside to its current price.

Exploring Other Perspectives

Three members of the Simply Wall St Community currently place fair value for Air Products between US$290.86 and US$302.36 per share, underscoring how much individual views can differ. You should weigh those against the execution risk that large, capital intensive hydrogen and ammonia projects could face cost overruns or delays, and consider how different scenarios might affect the company’s future performance.

Explore 3 other fair value estimates on Air Products and Chemicals - why the stock might be worth as much as 11% more than the current price!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Air Products and Chemicals research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Air Products and Chemicals research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Air Products and Chemicals' overall financial health at a glance.

Looking For Alternative Opportunities?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- Uncover the next big thing with 32 elite penny stocks that balance risk and reward.

- Invest in the nuclear renaissance through our list of 85 elite nuclear energy infrastructure plays powering the global AI revolution.

- We've uncovered the 16 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.