The Bull Case For Arista Networks (ANET) Could Change Following Its Russell Top 50 Index Debut - Learn Why

Arista Networks Inc ANET | 0.00 |

- In late June 2026, Arista Networks, Inc. was added to the Russell Top 50 Index, placing it among the largest US-listed companies and increasing its presence in major institutional benchmarks.

- This index inclusion coincides with growing attention on Arista’s role in AI-focused networking and public cloud-managed LAN solutions, tying its profile more closely to long-term infrastructure trends.

- We’ll now examine how Arista’s elevation into the Russell Top 50 Index shapes its investment narrative, particularly around AI-driven networking demand.

Explore 26 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

Arista Networks Investment Narrative Recap

To own Arista Networks today, you need to believe that Ethernet-based AI and cloud networking, plus software-rich campus offerings, can support durable demand even as competition intensifies. Inclusion in the Russell Top 50 raises Arista’s profile and may support liquidity, but it does not materially change the key near term catalyst of AI data center spending or the biggest risk around heavy reliance on a few hyperscale and AI customers.

The most relevant announcement alongside the index move is the growing focus on public cloud managed LAN and Campus Network as a Service, where third party research points to accelerated growth from 2026 to 2030. This ties directly into Arista’s efforts to broaden its enterprise and campus footprint, which could help offset concentration in a small number of hyperscale buyers if adoption of these cloud managed and NaaS offerings scales as expected.

Yet beneath the AI and index excitement, investors should be aware that Arista’s dependence on a handful of hyperscale customers...

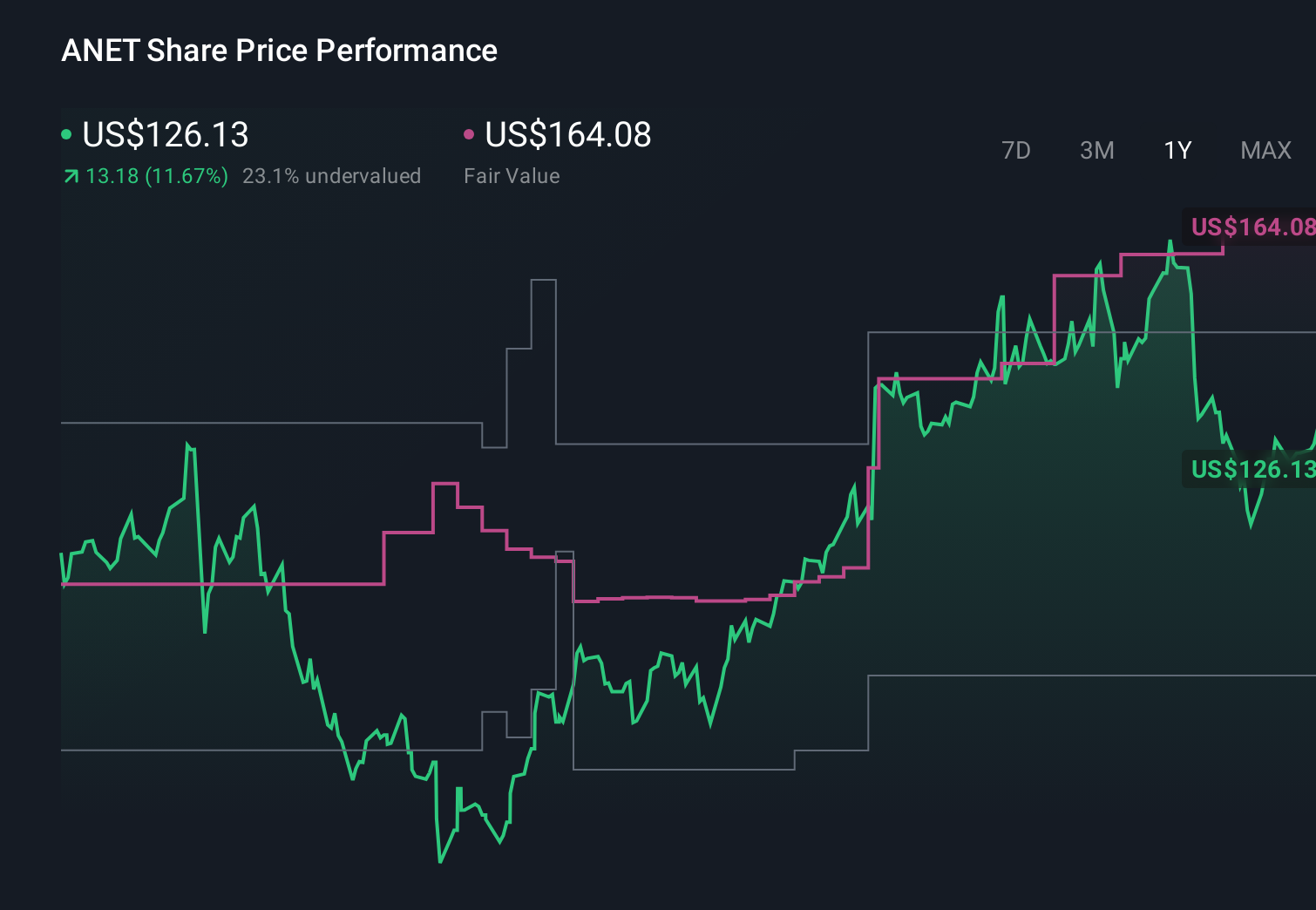

Arista Networks’ narrative projects $18.2 billion revenue and $6.6 billion earnings by 2029. This requires 23.3% yearly revenue growth and about a $2.9 billion earnings increase from $3.7 billion today.

Uncover how Arista Networks' forecasts yield a $190.09 fair value, a 12% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were already penciling in about US$20.2 billion of revenue and US$7.3 billion of earnings by 2029, which is far more aggressive than the consensus narrative, so this index inclusion and AI focus could either reinforce that bullish view or prompt you to reconsider how concentration risk might cap those expectations.

Explore 13 other fair value estimates on Arista Networks - why the stock might be worth as much as 25% more than the current price!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Arista Networks research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Arista Networks research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Arista Networks' overall financial health at a glance.

No Opportunity In Arista Networks?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- The future of work is here. Discover the 29 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Outshine the giants: these 15 early-stage AI stocks could fund your retirement.

- We've uncovered the 10 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.