The Bull Case For Boeing (BA) Could Change Following Riyadh Air’s First 787 Deliveries Milestone

Boeing Company BA | 0.00 |

- Earlier in June 2026, Boeing and Riyadh Air announced the delivery of the new carrier’s first two 787 Dreamliners to Riyadh, marking a key step in Saudi Arabia’s plan to use a fleet of up to 72 of these jets to connect the Kingdom with more than 100 global destinations by 2030.

- This milestone not only advances Boeing’s widebody presence in a fast-growing Middle Eastern hub, it also underpins long-term demand for its aircraft and services as Riyadh Air builds out a globally connected network.

- Now we’ll examine how Boeing’s progress with Riyadh Air’s 787 fleet plan could influence the company’s broader investment narrative and outlook.

The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 14 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

Boeing Investment Narrative Recap

To own Boeing today, you need to believe the company can translate its large commercial backlog and improving operations into sustainable cash generation while managing high debt and ongoing quality and certification challenges. The Riyadh Air 787 deliveries support the long term widebody story, but the key near term catalyst remains monthly orders and deliveries data, which directly affects cash flow, and the biggest risk is still further delays or disruptions in getting aircraft out the door.

In that context, Boeing’s recent report of 60 aircraft deliveries in May, up from 47 in April, is particularly relevant. It ties directly to how quickly Boeing can convert its backlog, including Riyadh Air’s planned 787 fleet, into revenue and cash. Any setbacks here, whether from supply chain issues, customer deferrals like Air India’s, or new quality problems, would matter more to the investment case than a single airline milestone.

Yet against these encouraging headlines, investors should also be aware of the risk that persistent production and certification delays could still...

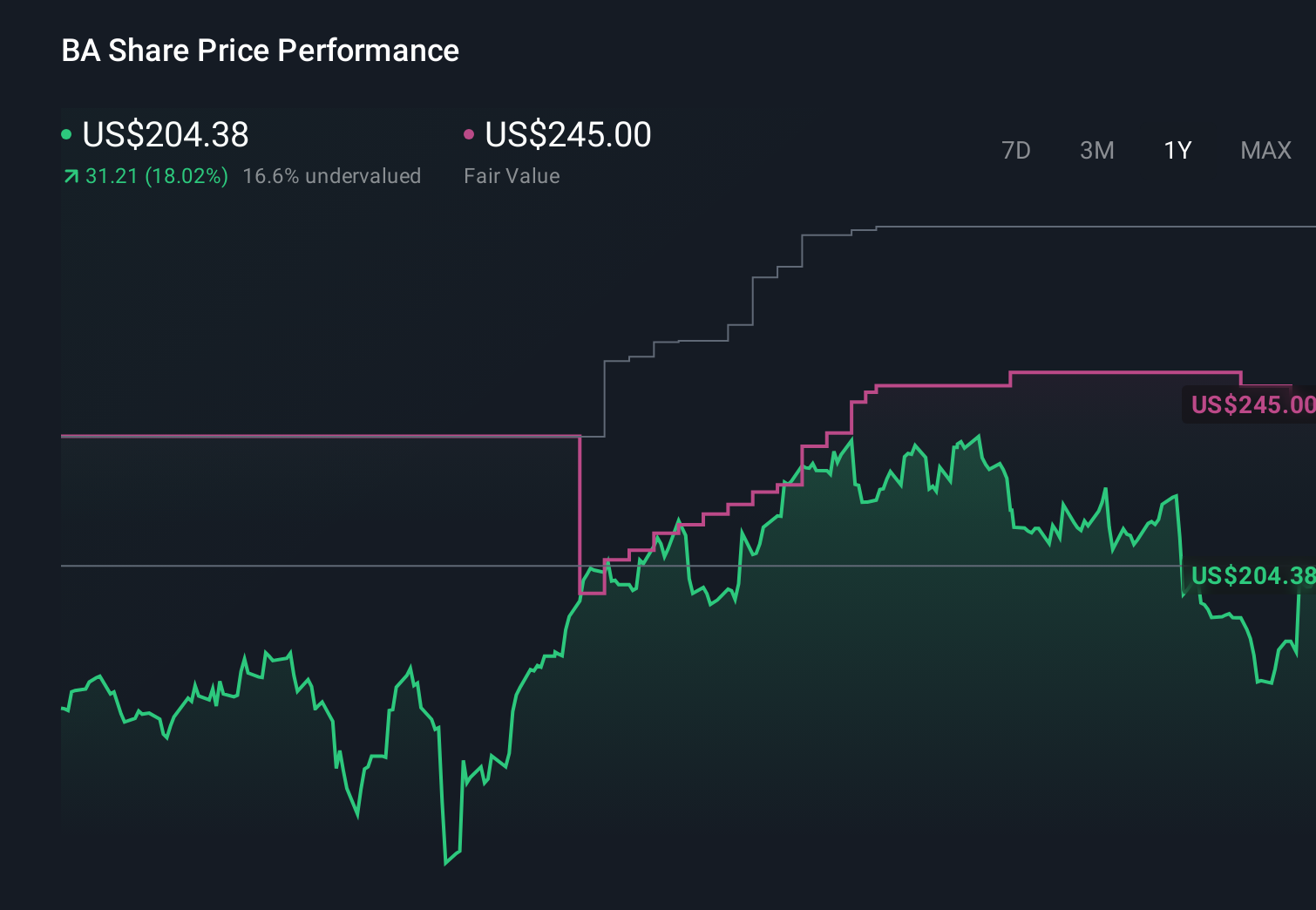

Boeing's narrative projects $125.3 billion revenue and $7.9 billion earnings by 2029. This requires 10.8% yearly revenue growth and a $6.0 billion earnings increase from $1.9 billion today.

Uncover how Boeing's forecasts yield a $269.52 fair value, a 23% upside to its current price.

Exploring Other Perspectives

While consensus already assumed solid recovery, the most optimistic analysts were penciling in US$132.7 billion of revenue and US$11.7 billion of earnings by 2028, so this Riyadh Air milestone and the broader quality concerns could either bolster or challenge that faster rebound story, reminding you that reasonable views on Boeing’s upside and downside can differ sharply.

Explore 7 other fair value estimates on Boeing - why the stock might be worth just $269.52!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Boeing research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Boeing research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Boeing's overall financial health at a glance.

Ready For A Different Approach?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- Explore 29 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Find 44 companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.