The Bull Case For CAVA Group (CAVA) Could Change Following Upbeat Q1 2026 Results And Expansion Plans

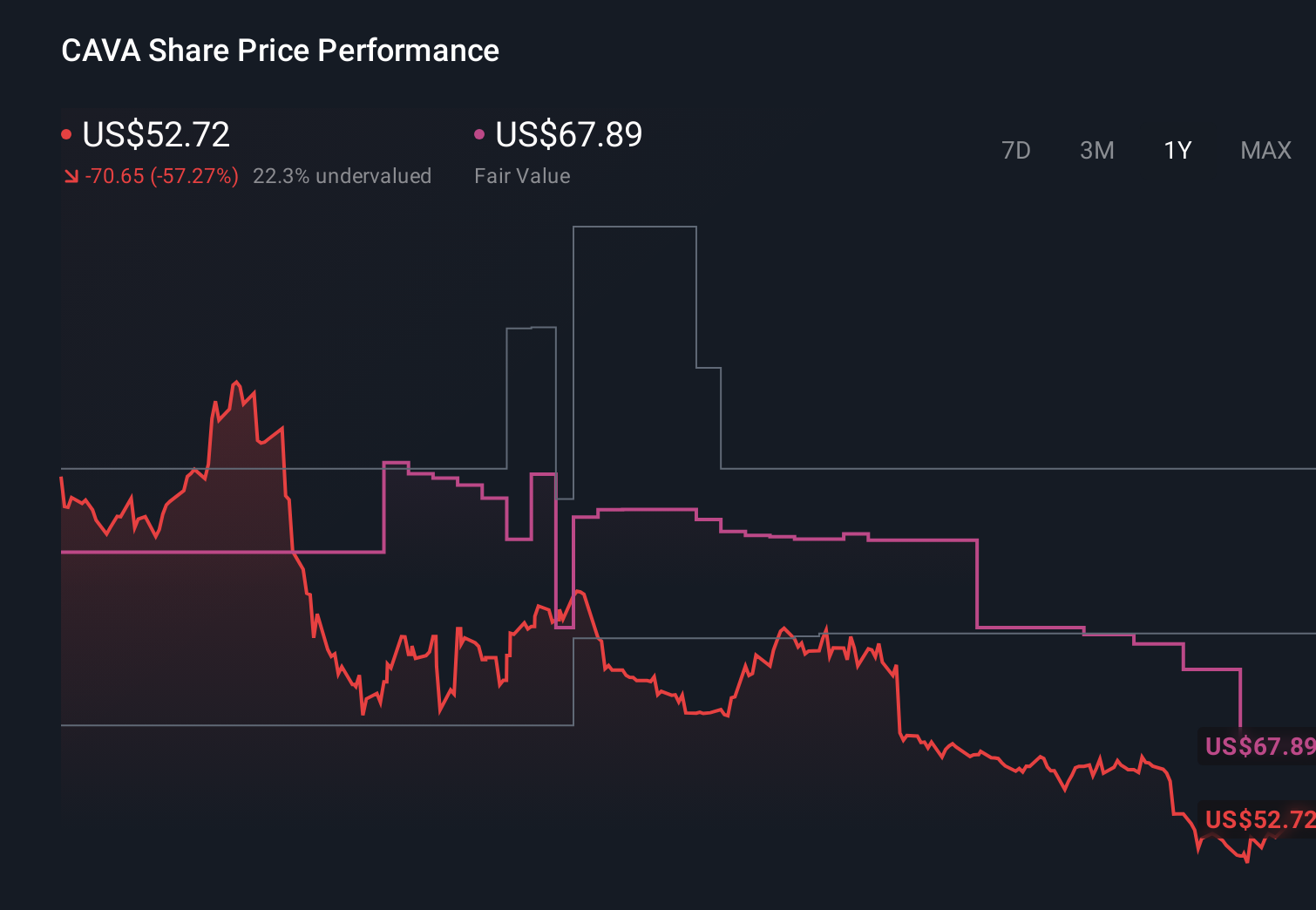

CAVA Group CAVA | 0.00 |

- CAVA Group’s first-quarter 2026 results showed sales rising to US$438.27 million from US$331.83 million a year earlier, while net income eased slightly to US$23.57 million, alongside a 9.7% increase in same-restaurant sales and an expanded outlook for new openings and adjusted EBITDA.

- At the same time, CAVA continued its rapid buildout, including a new Columbus, Ohio location and a plan to reach at least 1,000 restaurants by 2032, underscoring how menu innovation, digital engagement, and Midwest expansion are central to its growth ambitions.

- We’ll now examine how CAVA’s stronger same-restaurant sales and raised full-year guidance might influence the company’s existing investment narrative.

AI is about to change healthcare. These 34 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

CAVA Group Investment Narrative Recap

To own CAVA, you need to believe it can keep growing traffic and unit count without eroding margins or overextending its concept. The key near term catalyst is sustaining strong same-restaurant sales as new stores open quickly, while the biggest risk is that premium expectations and rapid expansion leave little room for operational missteps. The latest quarter’s revenue beat, 9.7% same-restaurant sales growth, and higher full year guidance support the catalyst, but do not remove the execution and valuation risk.

The most relevant update here is CAVA’s raised 2026 outlook, including more planned openings and higher adjusted EBITDA guidance alongside robust same-restaurant sales. That guidance sits on top of a footprint that is set to hit roughly 500 locations this year, with new Midwest markets like Columbus testing whether the concept can travel efficiently. For investors, this combination of faster expansion and upgraded profit targets sharpens the focus on how sustainable unit economics and traffic really are.

Yet even with strong momentum, investors should be aware that rapid expansion, premium pricing and insider selling could all become pressure points if...

CAVA Group's narrative projects $2.1 billion revenue and $122.3 million earnings by 2029.

Uncover how CAVA Group's forecasts yield a $87.27 fair value, a 9% upside to its current price.

Exploring Other Perspectives

While consensus leans optimistic, the lowest analysts were assuming about US$2.1 billion revenue and US$120.7 million earnings by 2029, so this strong same restaurant performance may either ease their concerns about traffic sustainability or sharpen fears that such growth still cannot fully justify today’s high earnings multiples.

Explore 8 other fair value estimates on CAVA Group - why the stock might be worth less than half the current price!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your CAVA Group research is our analysis highlighting 1 key reward and 2 important warning signs that could impact your investment decision.

- Our free CAVA Group research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate CAVA Group's overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- Outshine the giants: these 13 early-stage AI stocks could fund your retirement.

- Find 48 companies with promising cash flow potential yet trading below their fair value.

- We've uncovered the 10 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.