The Bull Case For Celsius Holdings (CELH) Could Change Following Bullish Coverage And Rising Regulatory Scrutiny

Celsius Holdings, Inc. CELH | 0.00 |

- Celsius Holdings recently saw renewed attention after Bernstein initiated coverage with an Outperform rating and highlighted its evolution into a multi-brand energy beverage platform through the Alani Nu and Rockstar Energy acquisitions, alongside strong post-deal revenue growth and ongoing integration challenges.

- At the same time, regulatory scrutiny over alleged youth-focused marketing practices and an investor investigation have added a layer of legal and reputational risk that now sits alongside the company’s expanding product and distribution footprint.

- We’ll now examine how Bernstein’s upbeat initiation amid regulatory probes could reshape Celsius Holdings’ investment narrative and risk-reward balance.

Capitalize on the AI infrastructure supercycle with our selection of the 48 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

Celsius Holdings Investment Narrative Recap

To own Celsius today, you need to believe its shift into a multi-brand, health-oriented energy platform can justify a rich valuation despite margin pressure and intense competition. In the near term, the key catalyst remains execution on integrating Alani Nu and Rockstar, while the biggest risk now includes the Texas investigation and related securities probe. Bernstein’s upbeat initiation does not remove that risk, but it does underscore continuing confidence in the brand and distribution story.

The most relevant recent development is Celsius’s Q1 2026 update, where revenue grew 138% year over year, largely from the Alani Nu and Rockstar deals, while gross margin slipped from 52.3% to 48.3%. That mix of rapid top line expansion and profitability strain sits directly at the heart of today’s catalyst and risk balance, especially as legal and regulatory scrutiny raise fresh questions about how sustainable that growth may be.

Yet behind the growth story, there is a regulatory and legal overhang that investors should be aware of, including potential actions related to...

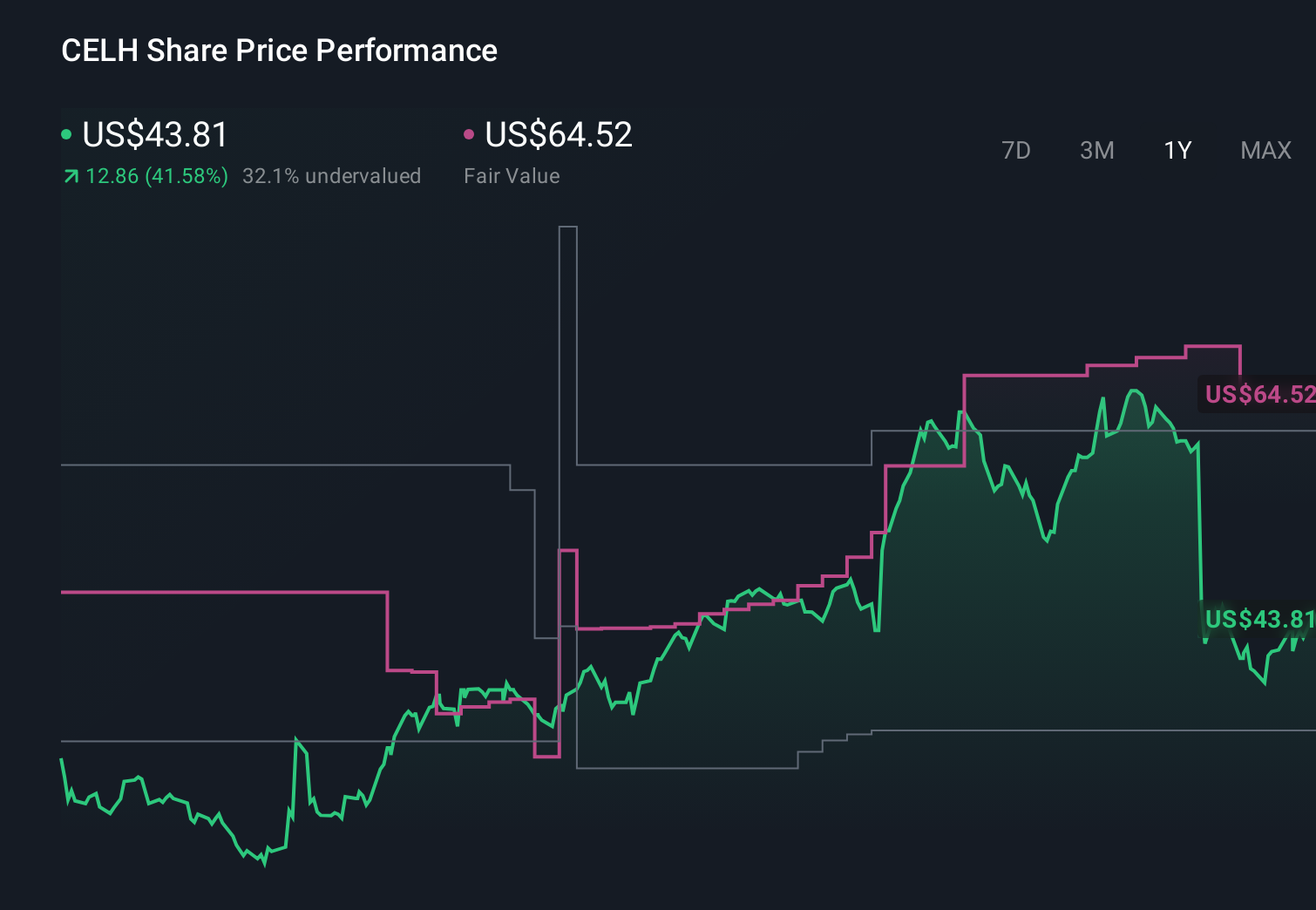

Celsius Holdings' narrative projects $4.0 billion revenue and $600.4 million earnings by 2029. This requires 10.5% yearly revenue growth and about a $486 million earnings increase from $114.5 million today.

Uncover how Celsius Holdings' forecasts yield a $61.35 fair value, a 110% upside to its current price.

Exploring Other Perspectives

Compared with consensus, the lowest analysts were already more cautious, assuming revenue of about US$3.8 billion and earnings near US$550.8 million by 2029, and your view on the new Texas probe could easily tilt you closer to or further from that more pessimistic path.

Explore 14 other fair value estimates on Celsius Holdings - why the stock might be worth over 2x more than the current price!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Celsius Holdings research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Celsius Holdings research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Celsius Holdings' overall financial health at a glance.

Seeking Other Investments?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- AI is about to change healthcare. These 40 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Invest in the nuclear renaissance through our list of 88 elite nuclear energy infrastructure plays powering the global AI revolution.

- Outshine the giants: these 14 early-stage AI stocks could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.