The Bull Case For Celsius Holdings (CELH) Could Change Following Deutsche Bank’s Upgrade And Margin Outlook

Celsius Holdings, Inc. CELH | 0.00 |

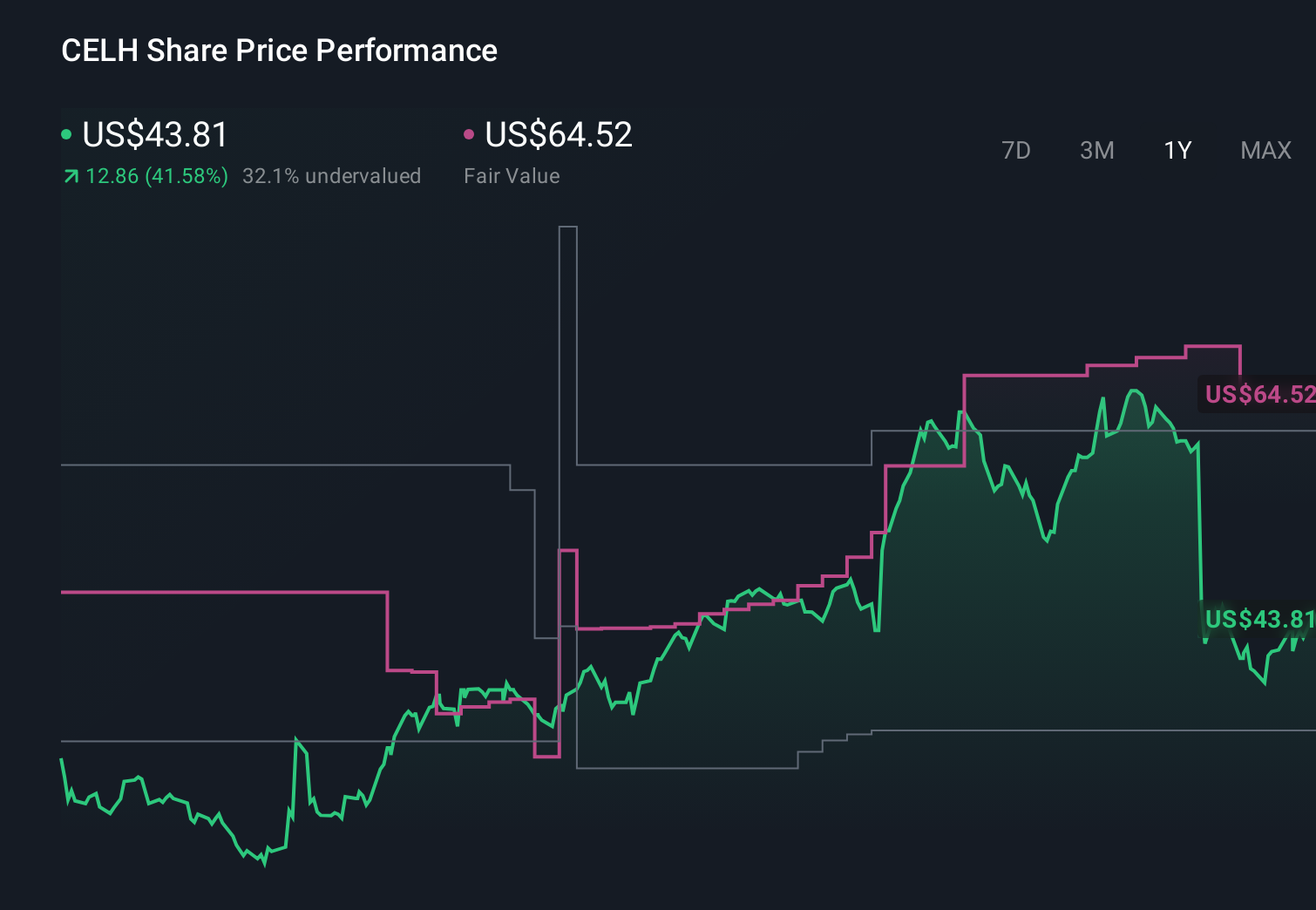

- In recent weeks, Celsius Holdings reported quarterly revenue of US$721.63 million and earnings per share of US$0.26, both beating analyst estimates, while Deutsche Bank upgraded its rating after reassessing competition from Costco’s private-label energy drink and the company’s integration of Alani Nu and Rockstar.

- Together with Celsius’s roughly 20% share of U.S. energy drink dollars and expectations for gross margin recovery to the low 50s by mid-2026, these developments highlight how brand scale and execution on integrations are becoming central to the company’s long-term profit profile.

- We’ll examine how Deutsche Bank’s upgrade, grounded in confidence about Costco competition and margin recovery, may reshape Celsius’s investment narrative.

The latest GPUs need a type of rare earth metal called Neodymium and there are only 26 companies in the world exploring or producing it. Find the list for free.

Celsius Holdings Investment Narrative Recap

To own Celsius, you have to believe its brand, distribution partnerships, and integrations (Alani Nu, Rockstar) can justify a rich valuation despite margin pressure and recent share price weakness. In the near term, the key catalyst is whether gross margins can move toward management’s low‑50s target, while the biggest risk remains rising input costs and integration‑related spending. The Deutsche Bank upgrade mostly reinforces the margin recovery story and does not materially change those near‑term drivers.

The Deutsche Bank upgrade, which argues Costco’s private‑label energy drink risk is overblown given it is only about 10% of projected 2025 sales, is especially relevant here. It directly addresses concerns around dependence on large club channels and suggests that Celsius’s roughly 20% U.S. energy drink dollar share and integration progress may be more important to the story than any single retailer’s private‑label push.

Yet behind the upbeat margin recovery narrative, investors should be aware of how rising aluminum and ingredient costs could still...

Celsius Holdings' narrative projects $3.7 billion revenue and $532.9 million earnings by 2028.

Uncover how Celsius Holdings' forecasts yield a $64.00 fair value, a 86% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were penciling in earnings near US$757 million by 2029, which contrasts sharply with current cost and competitive risks that could prompt a rethink after this news.

Explore 16 other fair value estimates on Celsius Holdings - why the stock might be worth over 2x more than the current price!

Form Your Own Verdict

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Celsius Holdings research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Celsius Holdings research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Celsius Holdings' overall financial health at a glance.

Ready For A Different Approach?

Our top stock finds are flying under the radar-for now. Get in early:

- Find 63 companies with promising cash flow potential yet trading below their fair value.

- The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Uncover the next big thing with 31 elite penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.