The Bull Case For CleanSpark (CLSK) Could Change Following CEO Return and Profitable Quarter Learn Why

Cleanspark, Inc. CLSK | 0.00 |

- CleanSpark, Inc. announced in August 2025 that co-founder and executive chairman Matt Schultz has returned as CEO and President, following the resignation of Zachary Bradford; the board also reduced its size from six to five members, effective August 10.

- This leadership change was accompanied by a significant turnaround in CleanSpark’s financial performance, as third-quarter results showed a return to profitability with net income of US$257.39 million compared to a net loss a year earlier.

- We'll take a closer look at how the combination of executive changes and renewed profitability shapes CleanSpark’s investment narrative moving forward.

We've found 19 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

CleanSpark Investment Narrative Recap

To be a CleanSpark shareholder right now, you need to believe in the long-term growth of Bitcoin mining, backed by operational efficiency and continual infrastructure scaling. The recent CEO transition seems unlikely to immediately alter the key short-term catalyst, Bitcoin price action, but reintroducing a founder with deep industry experience could reinforce stability. The largest risk remains CleanSpark’s near-total exposure to Bitcoin volatility and structural mining economics, which could leave earnings vulnerable if external conditions worsen.

Among recent announcements, CleanSpark’s return to profitability in the latest quarter, reporting net income of US$257.39 million, is most relevant. This marks a meaningful change in operating results and may help to support both market confidence and future investment capacity, especially given the capital-intensive nature of mining expansion. However, this positive momentum faces ongoing risk from fluctuating Bitcoin prices and rising energy costs.

But for investors, it is equally important to recognize that against the backdrop of impressive recent earnings, CleanSpark’s ongoing reliance on Bitcoin’s price leaves it open to external shocks if...

CleanSpark's narrative projects $1.5 billion in revenue and $324.9 million in earnings by 2028. This requires 32.7% yearly revenue growth and a $32.4 million earnings increase from $292.5 million today.

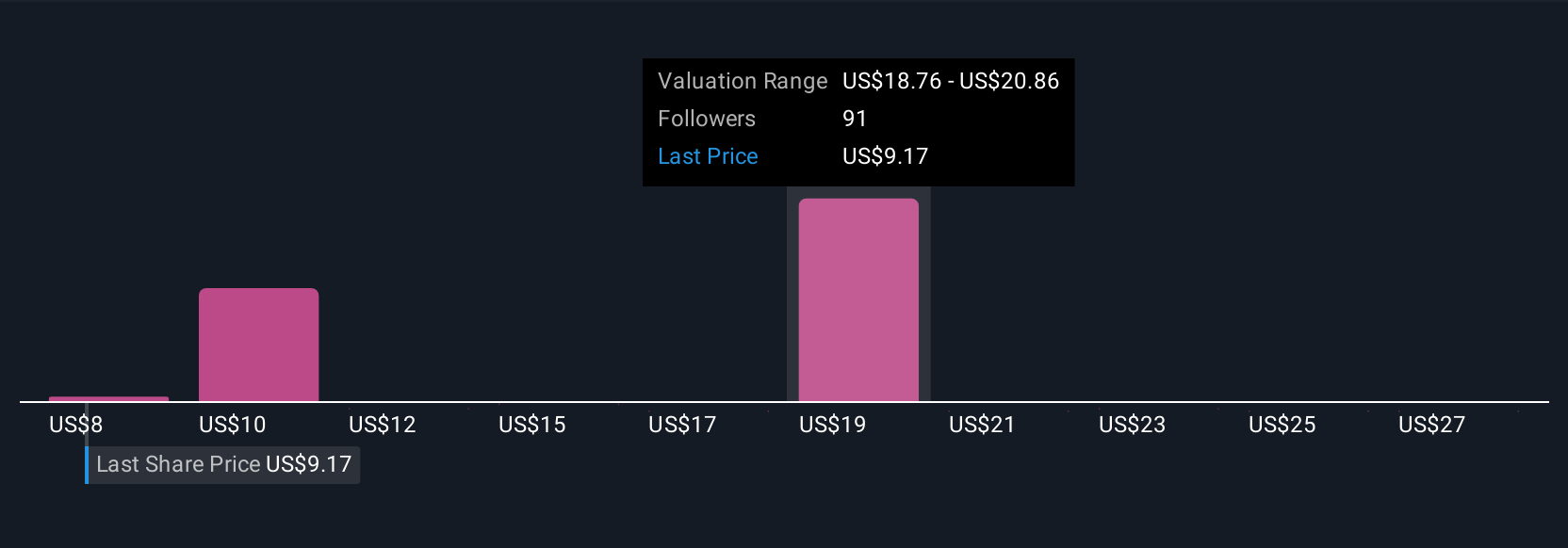

Uncover how CleanSpark's forecasts yield a $20.43 fair value, a 115% upside to its current price.

Exploring Other Perspectives

Fair value estimates from 18 Simply Wall St Community members range from US$8.26 to US$29.26 per share, showing wide disagreement. Revenue growth forecasts remain high, but ongoing reliance on Bitcoin fundamentals means your view could swing outcomes significantly.

Explore 18 other fair value estimates on CleanSpark - why the stock might be worth 13% less than the current price!

Build Your Own CleanSpark Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your CleanSpark research is our analysis highlighting 5 key rewards and 3 important warning signs that could impact your investment decision.

- Our free CleanSpark research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate CleanSpark's overall financial health at a glance.

Ready For A Different Approach?

Our top stock finds are flying under the radar-for now. Get in early:

- AI is about to change healthcare. These 27 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 20 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.