The Bull Case For Coty (COTY) Could Change Following Gucci Beauty License Return To Kering

Coty Inc. Class A COTY | 0.00 |

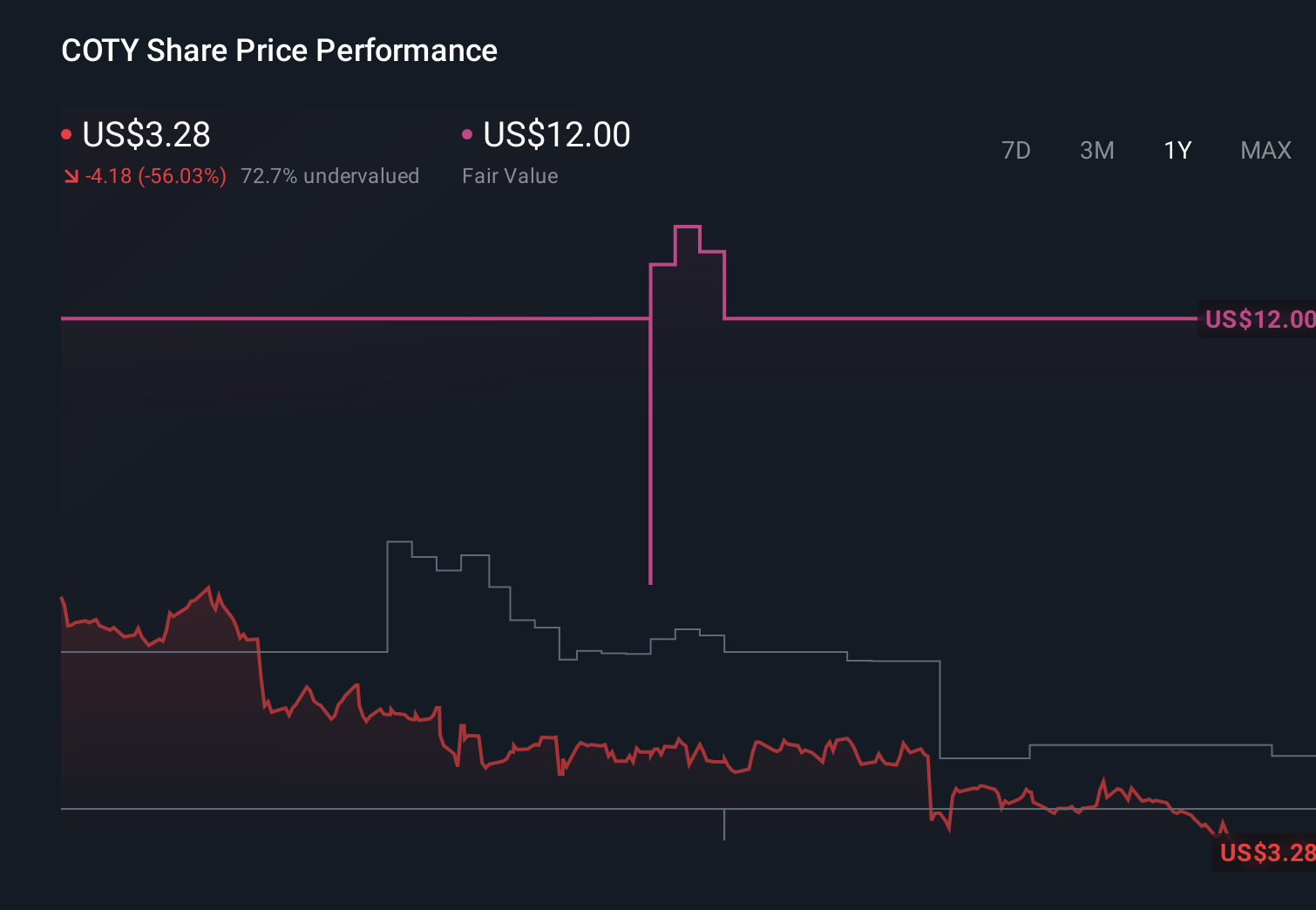

- Coty Inc. recently agreed to transition the Gucci Beauty license back to Kering for about US$400 million, while continuing to operate the brand until at least June 30, 2027 and resolving all related litigation between the two groups.

- The deal, alongside recent leadership and organizational changes under the Coty.Curated strategy, marks a meaningful reshaping of Coty’s prestige portfolio focus and operating structure.

- We’ll now examine how the Gucci Beauty license transition and related cash proceeds may influence Coty’s existing investment narrative.

Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

Coty Investment Narrative Recap

To own Coty today, you need to believe it can refocus on core prestige and mass fragrances, restore profitability, and use its balance sheet more effectively. The Gucci Beauty license transition provides US$400 million of proceeds that, if applied as announced to debt reduction and core brands, could modestly ease leverage concerns. The main near term catalyst remains execution on fragrance launches and portfolio focus, while high competition and ongoing losses still look like the key risk.

The most relevant update here is the July 2 Coty.Curated reorganization, which pulls prestige R&D, sustainability, and supply chain under one leader and gives Markus Strobel direct control of prestige commercial operations. Together with the Gucci license exit, this concentrates decision making around Coty’s remaining prestige portfolio and could influence how effectively it supports new launches and manages retailer destocking, a critical element of the existing catalyst path.

Yet even with these moves, investors should still be aware of how Coty’s elevated debt and refinancing needs could limit flexibility if...

Coty's narrative projects $5.9 billion revenue and $411.8 million earnings by 2029. This assumes fairly flat yearly revenue and an earnings increase of about $957.6 million from -$545.8 million today.

Uncover how Coty's forecasts yield a $3.17 fair value, a 42% upside to its current price.

Exploring Other Perspectives

Before this news, the most bearish analysts assumed roughly flat revenue near US$5.8 billion and earnings of about US$239 million by 2029, a far slower earnings recovery than consensus. If you lean toward that view, the Gucci exit and cash inflow might or might not soften concerns about high debt and margin pressure, which is exactly why it is worth comparing how your expectations line up against both narratives.

Explore 5 other fair value estimates on Coty - why the stock might be worth just $3.13!

Form Your Own Verdict

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Coty research is our analysis highlighting 3 key rewards that could impact your investment decision.

- Our free Coty research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Coty's overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- Find 45 companies with promising cash flow potential yet trading below their fair value.

- Uncover the next big thing with 20 elite penny stocks that balance risk and reward.

- The future of work is here. Discover the 29 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.