The Bull Case For Deere (DE) Could Change Following Margin Pressures In Precision Agriculture - Learn Why

Deere & Company DE | 0.00 |

- In recent days, Deere & Company has faced increased scrutiny ahead of its 21 May Q2 earnings release, as analysts highlight the possibility of lower quarterly earnings even if revenue rises.

- This focus has sharpened concerns around Deere’s Production & Precision Agriculture segment, where farmer cost pressures, tariffs, and a softer agricultural cycle are weighing on expected profitability.

- Now, we’ll examine how these margin concerns in precision agriculture influence Deere’s previously outlined investment narrative and assumptions.

Invest in the nuclear renaissance through our list of 87 elite nuclear energy infrastructure plays powering the global AI revolution.

Deere Investment Narrative Recap

To own Deere today, you need to believe its precision agriculture and automation strategy can sustain attractive margins even as farm incomes and equipment cycles fluctuate. The key near term catalyst is how the Q2 results and outlook frame profitability in Production & Precision Ag, where tariffs and farmer cost pressures are already in focus. The latest earnings worries reinforce, rather than change, the biggest risk right now: margin compression if Deere cannot offset rising costs and softer demand.

Among recent announcements, the upcoming 21 May Q2 earnings release stands out as the most relevant. Consensus expects lower earnings despite higher revenue, which puts a spotlight on how Deere’s precision agriculture investments, software offerings, and cost actions are affecting segment profitability. With shares having lagged the broader market recently, the way management talks about Production & Precision Ag margins and tariff costs in this report could strongly influence how investors view the current thesis.

Yet beneath Deere’s precision ag story, there is still the underappreciated risk that growing tariff costs could erode margins in ways investors should be aware of...

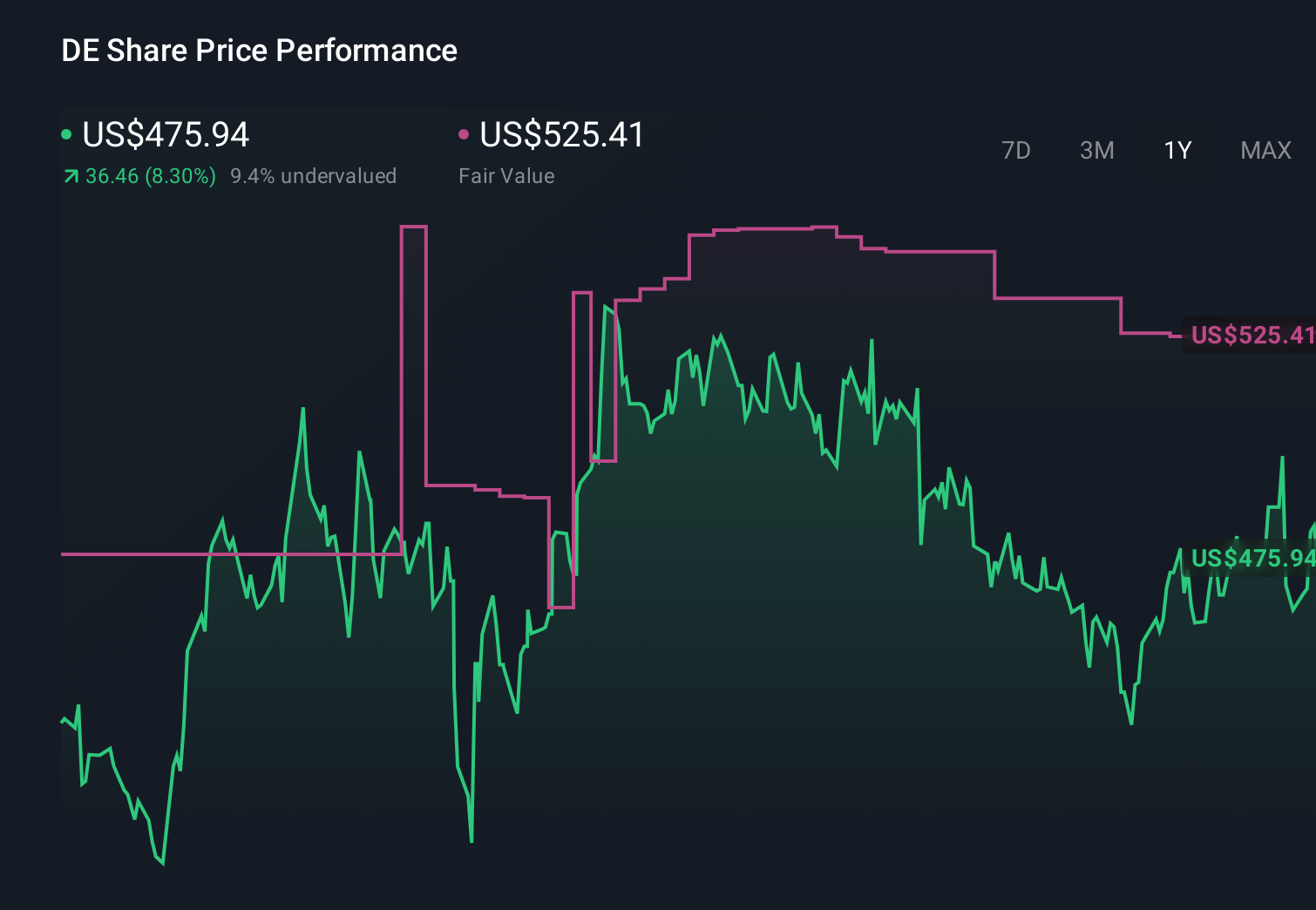

Deere's narrative projects $47.4 billion revenue and $8.4 billion earnings by 2029. This requires flat yearly revenue growth and a $3.6 billion earnings increase from $4.8 billion today.

Uncover how Deere's forecasts yield a $665.10 fair value, a 18% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were assuming Deere could almost double earnings to about US$10.3 billion by 2029, even as others warn that absorbing roughly US$1.2 billion in annual tariff costs could crimp margins, so you should expect that both the bullish and cautious narratives may shift as the latest precision ag margin and Q2 earnings news is absorbed.

Explore 4 other fair value estimates on Deere - why the stock might be worth just $655.00!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Deere research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Deere research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Deere's overall financial health at a glance.

Searching For A Fresh Perspective?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- AI is about to change healthcare. These 32 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Uncover the next big thing with 24 elite penny stocks that balance risk and reward.

- Find 49 companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.