The Bull Case For DoorDash (DASH) Could Change Following Autonomous EV Deal With ALSO – Learn Why

DoorDash, Inc. Class A DASH | 156.45 | +3.95% |

- In March 2026, ALSO, a Palo Alto–based small electric vehicle company, announced that DoorDash had invested in it and entered a multi-year commercial agreement to develop and roll out autonomous delivery at scale.

- This move deepens DoorDash’s push into automation and logistics innovation, potentially reshaping how it manages last-mile delivery and fulfillment efficiency.

- We’ll now examine how DoorDash’s autonomous delivery partnership with ALSO could influence the company’s broader investment narrative and long-term positioning.

We've uncovered the 12 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

DoorDash Investment Narrative Recap

To own DoorDash, you need to believe it can keep turning its large local commerce footprint into growing, profitable cash flows while managing rising complexity, labor pressures, and intense competition. The ALSO partnership reinforces the automation story but does not clearly change the near term catalyst, which still centers on sustaining profitable growth in new verticals, or the key risk that higher fulfillment and labor related costs could pressure margins if efficiency gains lag.

The recent Foot Locker partnership helps illustrate why automation matters for DoorDash. As DoorDash adds large non restaurant retailers, fulfillment density and order complexity increase, making lower cost, reliable last mile delivery more important to protecting margins and supporting earnings. The ALSO alliance fits into this context by adding another autonomous delivery option that could influence how efficiently DoorDash serves these expanding retail relationships over time.

Yet, beneath the promise of automation, investors should be aware that tighter labor rules and eco compliance costs could still materially pressure DoorDash’s margins over time...

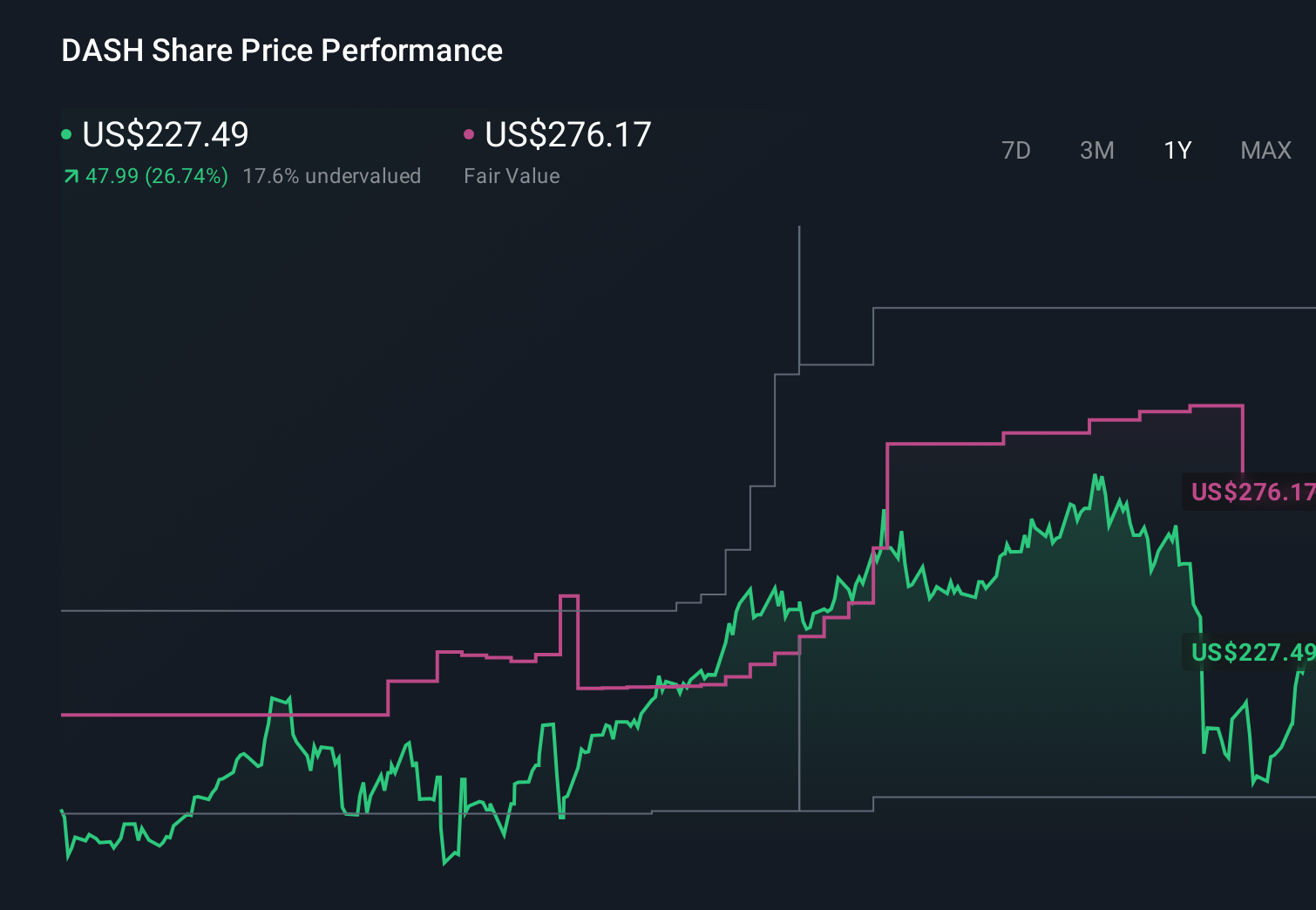

DoorDash's narrative projects $20.4 billion revenue and $3.2 billion earnings by 2028. This requires 19.6% yearly revenue growth and about a $2.4 billion earnings increase from $781.0 million today.

Uncover how DoorDash's forecasts yield a $258.00 fair value, a 72% upside to its current price.

Exploring Other Perspectives

Some of the lowest analysts were already assuming DoorDash would need to earn about US$2.3 billion on roughly US$23.7 billion of revenue, so this ALSO news could either ease or deepen those more pessimistic concerns about higher labor and eco costs depending on how the economics of autonomous delivery actually develop.

Explore 14 other fair value estimates on DoorDash - why the stock might be worth over 2x more than the current price!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your DoorDash research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free DoorDash research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate DoorDash's overall financial health at a glance.

Interested In Other Possibilities?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- This technology could replace computers: discover 24 stocks that are working to make quantum computing a reality.

- The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Capitalize on the AI infrastructure supercycle with our selection of the 36 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.