The Bull Case For Enterprise Products Partners (EPD) Could Change Following Fresh Analyst Attention On Wartime Energy Flows

Enterprise Products Partners L.P. EPD | 37.57 | +0.37% |

- On March 25, 2026, Enterprise Products Partners L.P. presented at the World Chemical Forum, while Wells Fargo upgraded the partnership to Overweight and Truist Financial began coverage with a Hold rating, both emphasizing its role in global energy logistics.

- The upgraded view from Wells Fargo, linked to evolving energy flows amid the Iran war, highlights Enterprise’s position as a key U.S. midstream beneficiary with a balance sheet and distribution profile Truist sees as comparatively resilient.

- We’ll now assess how Wells Fargo’s upgrade, tied to shifting global energy demand patterns, may influence Enterprise Products Partners’ existing investment narrative.

AI is about to change healthcare. These 34 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

Enterprise Products Partners Investment Narrative Recap

To own Enterprise Products Partners, you need to believe in steady demand for U.S. midstream infrastructure and the partnership’s ability to keep its assets full and cash flows durable. The Wells Fargo upgrade and Truist initiation, tied to shifting global energy flows, mainly reinforce this view rather than change it, while the biggest near term swing factors still look like export demand trends and execution on asset reliability, including avoiding repeats of unplanned outages.

The recent distribution increase to US$0.55 per unit for Q4 2025 is particularly relevant here, as Truist’s comments on a well covered payout sit alongside ongoing buybacks and project build outs. Together with Wells Fargo’s focus on Enterprise’s role in global energy logistics, this raises the stakes on how effectively new Permian and export capacity translates into stable cash generation and unit holder returns.

Yet investors should also be aware of how Enterprise’s US$31.9 billion debt load could interact with shifting credit conditions and...

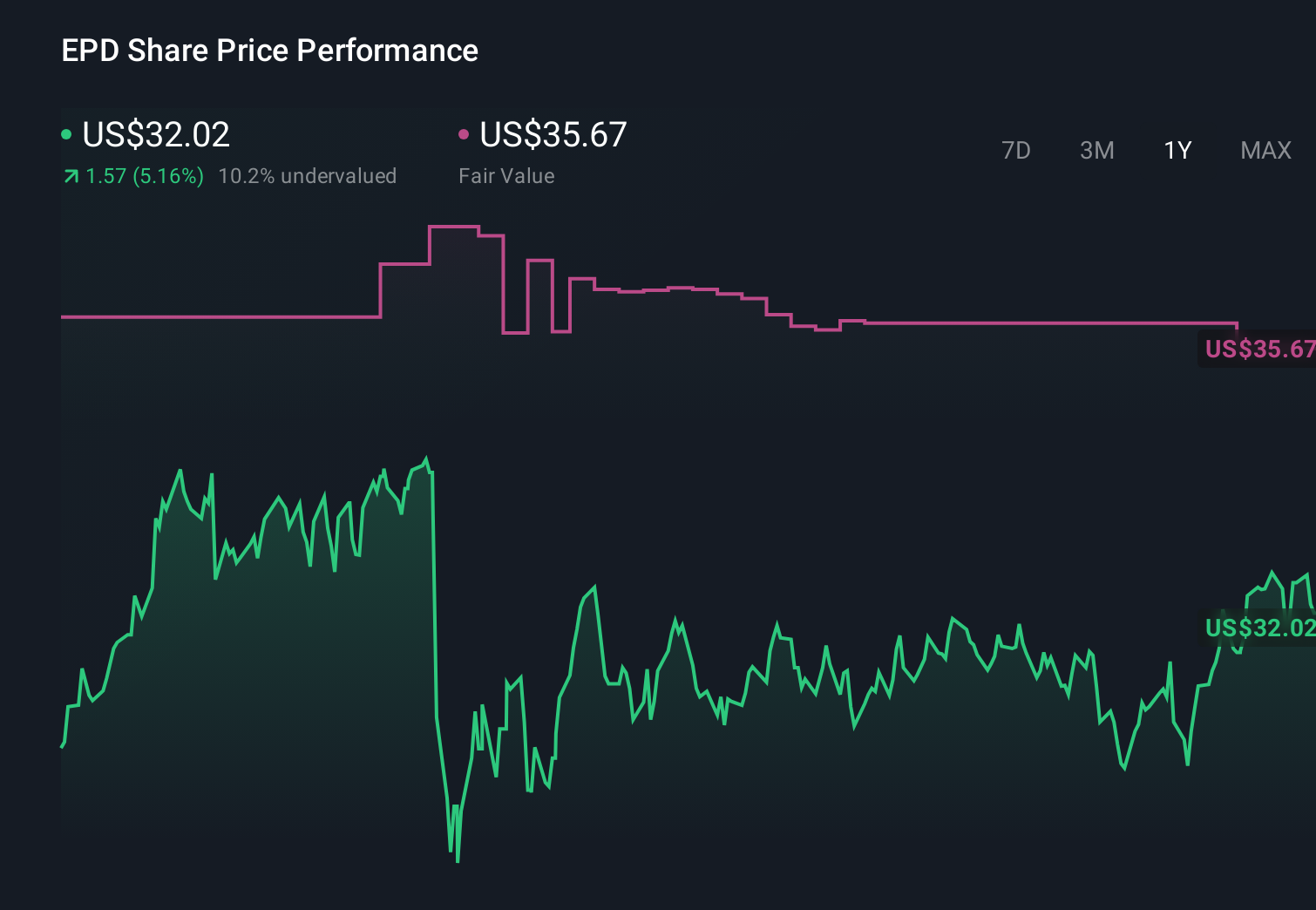

Enterprise Products Partners' narrative projects $58.4 billion revenue and $7.1 billion earnings by 2029. This requires 3.6% yearly revenue growth and a roughly $1.3 billion earnings increase from $5.8 billion today.

Uncover how Enterprise Products Partners' forecasts yield a $38.24 fair value, a 3% downside to its current price.

Exploring Other Perspectives

Eight members of the Simply Wall St Community currently value Enterprise Products Partners between US$34 and about US$89.54, with views spread across the entire range. Against this wide dispersion, the risk that high leverage meets changing interest or credit markets is a key factor that could shape how those expectations ultimately play out, so it is worth weighing several of these perspectives before forming your own view.

Explore 8 other fair value estimates on Enterprise Products Partners - why the stock might be worth 13% less than the current price!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Enterprise Products Partners research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Enterprise Products Partners research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Enterprise Products Partners' overall financial health at a glance.

Seeking Other Investments?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- Capitalize on the AI infrastructure supercycle with our selection of the 35 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

- Find 61 companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.